U.S. equities rose on Tuesday ahead of earnings reports by Microsoft and Alphabet after the close.

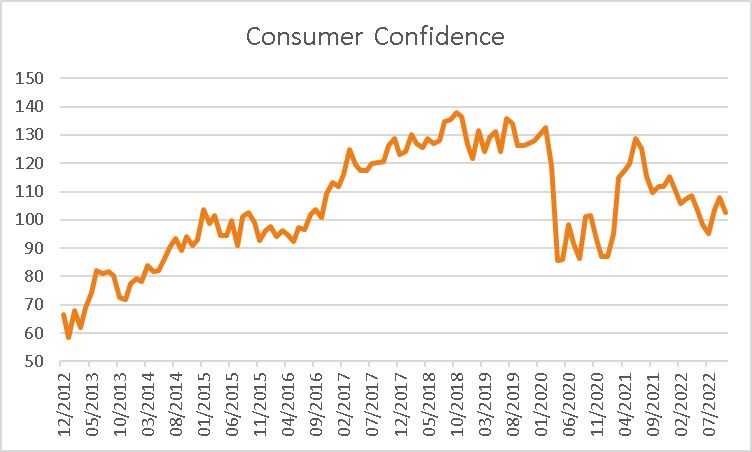

As of 3:48pm in New York, the S&P 500 rose +1.72% higher, with all sectors closing in the green except energy which fell -0.43%. Real estate, materials and consumer discretionary made the biggest gains, rising +3.43%, +2.33% and +2.26% respectively. The Dow increased by +1.10 %, the Nasdaq jumped +2.24%, the Russell 2000 rose +2.92%. The VIX index dipped -4.22% to 28.59 while the US 10-year note fell 14 basis points to 4.10%. More than 50% of companies have reported better than expected results this quarter, as Shawn Crux from TD Ameritrade explained, “The market was actually bracing itself for more pessimistic tones from companies as we got through earnings and it’s not coming out that way right now. It’s mixed too, but even being mixed is ahead of expectations.” The next few days will be of keen interest to investors from an earnings perspective, as Microsoft and Alphabet are set to report results after the closing bell today, followed by Meta sharing earnings on Thursday, along with Apple and Amazon set to report on Friday. Billionaire Elon Musk told his bankers that he wishes to close the Twitter deal on Friday, as reported by Bloomberg, pushing the company’s share price to a record high of $52.93. In economic data, the Conference Board’s measure of consumer confidence for October declined to 102.50 from 107.8 previously, more than the 106.5 forecast weighed by a weakening economic outlook.

In Europe, markets rallied on better-than-expected reporting from corporates. The STOXX 600 index closing +1.29% higher, energy being the only underperformer falling by -0.81%. The largest gains were seen in real estate, information technology and consumer discretionary which were up by +5.08%, +3.8% and +2.47% respectively. Out of the 65 companies on the index which have shared their earnings, 54% have beaten forecasts by analysts. The FTSE was up by +1.4%, the CAC rose by +1.94% and the Dax gained +0.94%. The newly elected PM Rishi Sunak took office and announced his cabinet, while the yield on the 10-year UK treasury note fell 11 points to 3.62%.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

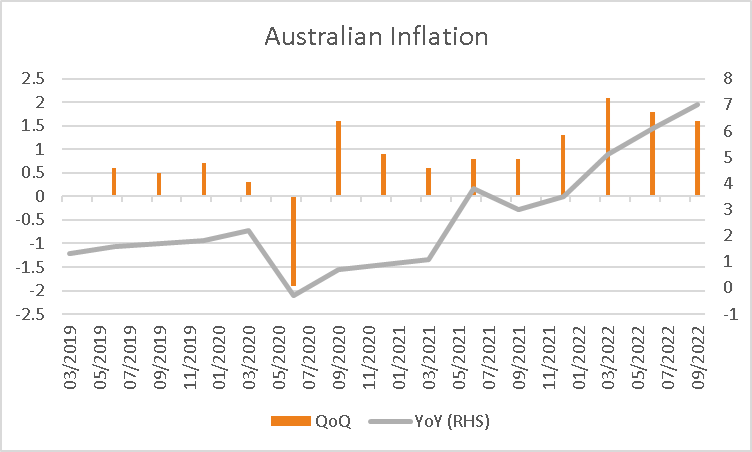

The ASX is set to open higher today, as ASX futures were up 53 points or 0.78% to 6,845. The ASX closed +0.28% higher on Tuesday, with real estate, communications and consumer discretionary boosting the index up by gaining +1.67%, +1.58% and +1.28% respectively. Shares in plumbing supplies Reliance group sunk -13.4% after announcing earnings before tax fell by 15% to $64.6 million. Ampol dropped -12.6% after the company announced a slowdown in profits for the third quarter, and CEO Matt Halliday warned of uncertainties affecting further trading conditions. The share price of Lithium explorer C29 was boosted 93% after it announced the company had signed an option agreement to acquire two lithium brine exploration licenses in South America. BHP Group and Rio Tinto both slipped -1.4%, Woodside Energy fell -0.9%. Pilbara Minerals declined -0.4%. Domino’s pizza’s share price fell -2.1% after broker Macquarie cut its valuation of the company, with declining sales due to households facing pressure in the rise of cost of living. Economic data showed that exports to China dropped 92%. In focus today is the release of Q3 inflation data expected to show prices rose +1.6% over the quarter and rose to +7% from +6.1% over the 12 months.

The federal budget was released on Tuesday, with the Albanese government warning of “hard days to come”, as it announced an agenda for tax increases and spending cuts which forecast debt and deficit to be worse than previously forecast. The cash rate, currently at 2.6%, is expected to reach 3.35%, will impact the cost of living as “Many indebted households will come under greater pressure.” Treasurer Jim Chalmers abandoned his pre-election pledge to reduce prices, stating “a lot has happened since that modelling was released”, with power prices expected to rise by 20% this year and 30% further by 2023-24.

In commodities, oil prices were mixed with the price of WTI rising +0.51% to $85.01 while Brent slipped -0.16% to $93.11. Spot gold edged up +0.26% to $1,654.17, spot silver gained +0.79% to $19.38. Meanwhile, SGX Iron ore closed +0.8% higher at $89.50, copper fell -0.69% to $341, nickel rose by +1.31% to $22,151. The price of bitcoin rose to 3.8% to $20,021.

Economic Calendar:

- Australian Business Confidence (OCT) 11:00

- Australian Inflation Rate YoY (Q3) 11:30

- Chinese FDI YoY (SEPT) 18:00

- US MBA Mortgage Applications 22:00

- US Retail Inventories Ex Autos MoM Adv (SEP) 23:30

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.