Equity markets slid on Friday after a rise in inflation expectations weighed on sentiment.

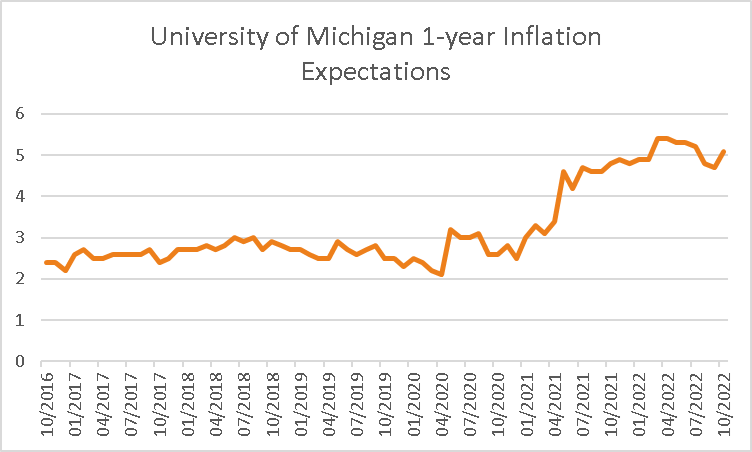

The S&P 500 closed -2.37% lower at the end of trading on Friday in broad-based selling with 94% of stocks closing lower. The biggest laggards were consumer discretionary, energy and materials which dropped by -3.88%, -3.71% and -3.41% respectively. The Dow declined by -1.34%, the Nasdaq dropped -3.08%, the Russell 2000 declined -2.66% and the VIX index rose by 0.25% to 32.02. The University of Michigan survey showed one-year ahead inflation expectations rose for the first time in several months to +5.1% from +4.7% previously with longer expectations also rising, which is worrisome for the Federal Reserve’s efforts to keep expectations anchored. Investors also continue to tread carefully amongst rising future supply chain hurdles which will hit corporate earnings, continued increases in interest rates to by banks to battle rampant global inflation, while geo-political uncertainty in Europe adds to market volatility. US Treasuries declined with the yield on the 2-year bond rising by 3.2 basis points to 4.49%, the 10-year bond yield was 4.02%, while the 30-year bond yield was 3.99%. Investors this week will be keen on earnings from Tesla Inc., Netflix and Johnson & Johnson, among others.

In Europe, markets closed higher before the weekend. The Euro STOXX 600 closed +0.63% higher on Friday, boosted by real estate which gained +3.72%, while utilities and healthcare were up +1.86% and +1.22% respectively. Energy and information technology were the only underperformers, both sliding -0.73%. The FTSE closed +0.7% higher, the CAC was up +0.9% while the DAX gained +0.67%. In the UK, ministers confirmed the sacking of Finance Minister Kwasi Kwarteng by the PM Liz Truss on Friday, after taking a U-turn on his mini budget. Mr. Kwarteng was replaced by Jeremy Hunt as the new Chancellor of the Exchequer, who won a vital endorsement from Band of England for his proposal to stabilize the country’s strained public finances. Mr. Hunt announced plans to abandon the premier’s dash-for-growth strategy. BOE Governor Andrew Bailey who had spoken to Mr. Hunt stated,” There is a very clear and immediate meeting of minds on the importance of sustainability”. Analysts at Goldman Sach’s had downgraded the country’s growth outlook after the sacking of Mr. Kwarteng, from -0.4% to minus 1%, while core inflation is seen at 3.1% at the end of 2023, versus 3.3% previously.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX is expected to open lower today, as ASX futures were down 102 points or 1.5 per cent to 6,660. The ASX 200 closed +1.75% higher on Friday following a strong rally on Wall Street despite U.S. inflation data moving higher. Energy, utilities and consumer staples soared by +3.75%, +3.62% and +2.04% respectively. Beach energy was up by +5.6% while Santos rose +4.4%. Qantas gained +3.2% after analysts gave an improved rating on the company following the release of half-year profit guidance from a day earlier. In banking, Westpac was up by +1.9%, National Australia Bank gained +1.6%, Commonwealth Bank was 0.8% higher while ANZ edged +0.4% higher. The yield on the Australian 10-year bond was little changed at 4.00% while the local currency weakened against the greenback by -1.6% to 0.6199. The Australian job markets report will be a focal point for investors this week, with a forecast of 20k jobs to be added in September and the unemployment rate decline to 3.3% compared to 3.5% in August.

In commodities, oil prices slumped with WTI and Brent Crude falling -3.91% and -3.11% to $85.61 and $91.63 respectively. In metals, Spot gold declined by -1.31%, spot silver fell -3.27% to $18.28, nickel fell -2.86% to $21,661, copper slid -0.49% to $342, Iron Ore rose +1.9% to $96.15, and the price of Bitcoin slipped -0.1% to $19,122.

Economic Calendar:

· 20th National Congress of the Chinese Communist Party 11:00

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.