Markets in the US rallied on Thursday despite inflation data hitting a 40-year high, hinting the year-long sell-off had potentially reached a bottom.

The S&P 500 reversed initial losses of as much as -2% before gaining +2.45% as of 3:43pm in New York, lead by energy, financials and materials which were up +3.87%, +3.81% and +2.86% respectively. The Dow gained +2.7%, the Nasdaq Composite was up +2.0941% while the Russell 2000 rose by +2.41% with the VIX Index down by -3.46% to 32.4. FWDBONDS chief economist, Chris Rupkey commented on the market’s performance stating, ”The Fed’s rate hikes may have won the battle with core commodities prices softening, but they are losing the war when it comes to rampant price hikes for the gigantic services ex-energy sector which cover 56.8 per cent of the economy. Today’s red hot inflation report brings the economy closer than ever to recession next year as the Fed loses patience and jacks up rates even higher than the markets thought”. On the rally despite hotter inflation data, Thomas Hayes of Great HilL Capital noted “There are no sellers left…no question that we’re at or near the bottom” hinting at capitulation by investors”.

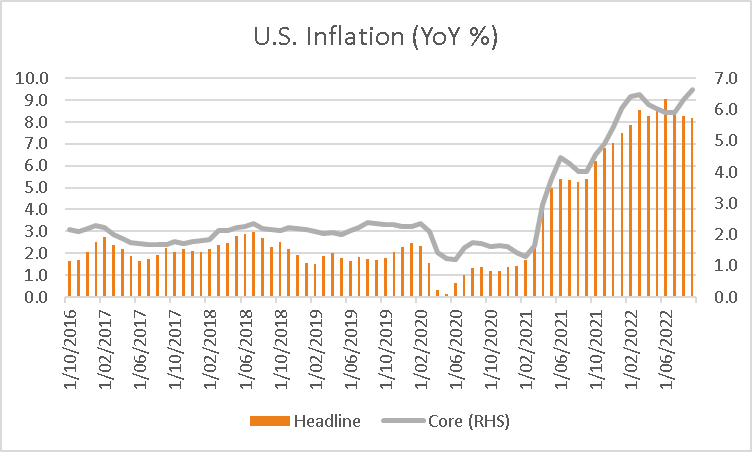

Economic data revealed the inflation rate of the US dropped slightly to 8.2% in September from 8.3% in August, while core inflation rose to 6.6% in September from 6.3% in the previous month above expectations of +6.5%. US Jobless claims also rose by 9k to 228k, also above forecasts. The markets are betting on the Fed to raise the interest rate by 75 basis points in the next two meetings while predicting the current hiking cycle will take interest rates past 4.85% from the current rate of 3.25%, before the tightening cycle ends. The yield on the 2-year US Treasury bond was +4.43%, while the yield on the 10-year and 30-year bonds was 3.93% and 4.22% respectively. In corporate news, Netflix saw a jump of +4.1% after announcing the launch of an ad-supported streaming service.

In Europe, the Euro STOXX 600 was up +0.69%, with energy, financials and industrials rising by +2.74%, 2.2% and +1.38% respectively, while the only sectors closing lower were consumer staples down by -1.24% and healthcare which slid -0.37%. The FTSE gained +1.56%, the CAC was up +1.04% and the Dax gained +1.51%. The UK markets are turbulent after the government unveiled plans to cut taxes, while the pound has dropped to $1.13. Susana Cruz, strategist at Liberum Capital Ltd. commented on the UK markets, “A U-turn would clearly lift investor sentiment and support not only government bonds but also the outlook of the UK economy as consumers would face lower mortgage payments, borrowing costs thus more disposable income.”

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX is set to open higher this morning, as ASX future were up 105 points or 1.58% to 6,739 . The ASX edged -0.07% lower on Thursday to close at 6642.6, weighed down by real estate, healthcare and energy receding by -1.87%, -1.04% and -0.94% respectively. Qantas’ share price jumped +8.7% it announced pre-tax profit of $1.2 billion, nearly double of analyst’s expectations. Kelsian soared +6.3%, Webjet slid -1.2% and Flight Center declined -1.1%. The banking sector rallied with Westpac gaining 3%, National Australia Bank firming +2.4%, Commonwealth Bank rising +1.9% and the Bank of Queensland gaining +0.3%. Netwealth’s funds dropped -0.6% despite a rise in the firm’s funds under administration rising by 4.4% in September. In mining, Sociedad Quimica y Minera de Chile (SQM) share price tumbled -11% after Morgan Stanley shared concerns of the company’s lithium exports declining 10%. Lithium prices in China sunk -21% MoM, adding to the vows of mining companies. Alkem receded -5.6%, Pilbara Minerals fell 4.5%, Lake Resources declined 3% and Core Lithium declined 2.6%. The yield on the 10-year Australian bond fell 3 basis points to +3.99%, while the local currency gained strength against the greenback, rising +0.30% to 0.6297.

In commodities, oil prices soared on the back of further output cuts from OPEC+ and uncertainty surrounding the US’ cap on the purchase of Russian oil. The price of WTI and Brent Crude oil jumped +2.44% and +2.56% to $89.38 and $94.83. In metals, spot gold was down -0.34% to $1,667.37, spot silver slide -0.66% to $18.9, copper rose by +1.24% to $347, nickel was up +1.04% to $22,142, while SGX Iron Ore slid –1.94% at US$91.98. The price of bitcoin rose by +0.5% to $19,183.

Economic Calendar:

- Business NZ PMI (MoM Sep) 08:30

- China Inflation Rate (YoY Sep) 14:00

- US Retail Sales (MoM Sep) 23:30

- US Michigan Consumer Sentiment (MoM Oct) 01:00

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.