Equity markets in the US fell on Monday, although pared larger losses as the IMF forecast a global recession is looming, highlighting higher borrowing costs, along with geo-political tensions weighing in on corporate earnings.

As of 3:46pm in New York, the S&P 500 was -0.41% lower, weighed down by energy, information technology and real estate which fell by –1.81 %, -1.10% and –0.83% respectively. The Dow slid -0.11%, the Nasdaq was down -0.85%, the Russell 2000 fell -0.31%, while the VIX index rose +2.55% to 32.16. Semiconductor stocks took a hit after the US announced a new round of restrictions on China’s access to American technology. Morgan Stanley strategists expect the bearish trend in markets to continue, stating “The bear market will not be over until the deteriorating fundamental picture is more fully discounted”.

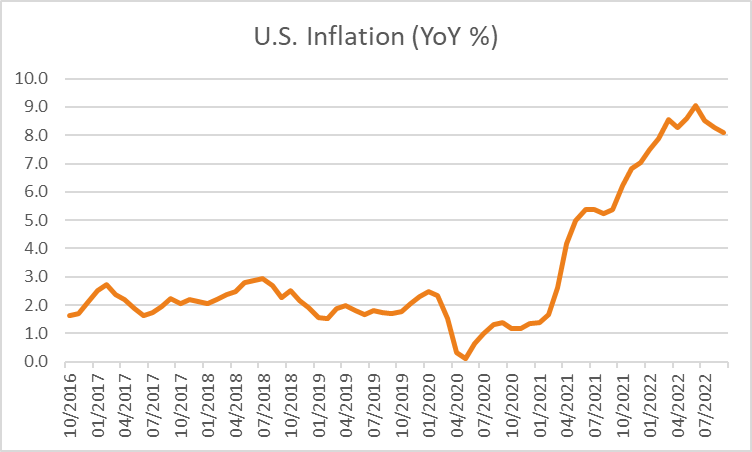

Data on the US inflation will be released on Thursday, with forecasts of the rate to be modestly lower in September, decreasing to 8.1% from 8.3% previously. Vice Chair Lael Brainard hinted at further hikes in the fed rate, stating cash rate hikes were still making their impact through the economy while Charles Evans of the Chicago Fed said inflation is much more persistent than thought but noted the central bank may be able lower inflation without pushing the economy into a recession.

European markets were mixed on Monday, as political uncertainty continues to overshadow the region. The Euro STOXX 600 Index slipped -0.4%, weighed down by information technology, real estate and energy which closed -1.75%, -1.34% and -1.23% lower. The CAC slipped -0.45%, while the DAX closed flat and the FTSE closed +0.05% higher, despite a turbulent UK bond market accelerating the sale of bonds, despite the Bank of England’s emergency stop measures.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX is expected to open higher today, with ASX futures up 16 points or 0.24% to 6,687. The ASX 200 closed -1.41% lower on Monday as all sectors underperformed. The index dropped 95 points to close at 6667.8, with the biggest laggards were the utilities, information technology and healthcare sectors which dropped by -3.19%, 2.59% and -2.11% respectively. Beach Energy edged -0.6% lower when the company announced two board members, Colin Beckett and Robert Jager would retire next month. Woodside energy fell by 0.7% after announcing a pre-emptive rights against Japan’s Tokyo Gas’ shock move to transfer interest in Woodside’s Pluto LNG project in Western Australia, while Santos lost -1%. Whitehaven was down -4.6%, New Hope fell -2.2%, Fortescue Metals rallied +1.8%, Rio Tinto was up 0.9%, BHP Group was flat. In banking, the top four banks declined with ANZ down -1.6%, Westpac -1.4%, National Australia Bank falling -1.7% and Commonwealth Bank was down by -1.5%. Payments company Tyro climbed +1.7% after announcing strong earnings for the first quarter and increasing its full-year guidance. Gold Road Resources slipped to -5.8%, after reporting its gold production for September. Dubber plunged 25.2% after the company restated its revenues, whilst its CFO resigned. Tabcorp rose +1.6% after announcing investment of $33 million in the online wagering platform Dabble Sports. In economic data, the Ai Group Services Index for September revealed a decline in business activity, The yield on the 10-year Australian bond was +2 basis points higher at 3.868%, while the local currency declined -1.15% to 0.6302.

In commodities, oil prices slumped with WTI and Brent crude declining -1.28% and -1.58% to $91.32 and $96.35 respectively following sharp gains on Friday. In metals, spot gold was down -1.48% to $1,670.16, spot silver slumped -2.35% to $19.06, copper strengthened +1.61% to $344, SGX Iron Ore rose +3.06% on Monday although is -0.98% lower this morning at US$96, and the price of bitcoin slipped by -0.9% to $19,294.

Economic Calendar:

- AUS Westpac Consumer Confidence Index (MoM Oct) 10:30

- UK Unemployment Rate (MoM Aug) 17:00

- ECB Lane Speech 23:45

- Fed Harker Speech 02:30

- Fed Mester Speech 03:00

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.