U.S. equities extended declines for a sixth straight session as concerns over tighter monetary policy weigh ahead of Friday’s PCE inflation data.

The S&P 500 declined by -0.21%, weighed down by consumer staples, utilities and real estate sectors receding -1.76%, -1.7% and -1.28% respectively. The energy sector was the best performing as oil prices rose, gaining +1.16%. The Dow fell -0.43% while the Nasdaq Composite rose +.25% along with the Russell 2000 +0.40% while the VIX Index continued to rise amidst growing fears of a recession, gaining +1.05% to 32.60. James Bullard, President of the Fed Reserve Bank of St. Louis hinted on the central bank’s agenda to raise the interest rate further, “We have increased the policy rate substantially this year and more increases are indicated”, with interest rates being moved to “the 4.5 per cent range”.

In relation, the Chicago Fed President Charles Evans stated that inflation would cool off in the next two years based on geo-political factors such as the Russia-Ukraine conflict and supply-side constraints to ease, “Supply-side repair could continue to move too slowly; events in Ukraine or further COVID-related shutdowns could put additional pressure on costs; and monetary policy may, on the one hand, not rein inflation in enough or, on the other hand, weigh too heavily on employment.”

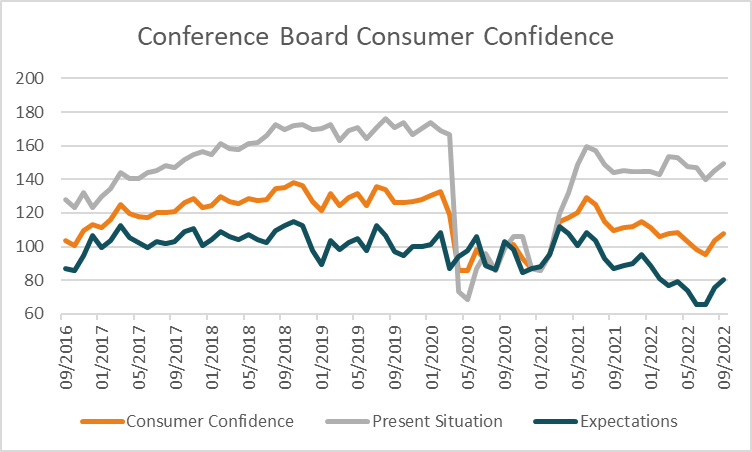

In economic data, the Conference Boards measure of consumer confidence report rose to 108 in September from 103.6 in August, above forecasts of 104.5 with confidence and expectations lifted by falling gasoline prices. The sale of new homes in August also rose by +28.8%, while orders for non-defense capital goods were up +1.3% since last month.

European markets receded based on escalating fears of a looming recession and the ECB raising interest rates again. The Stoxx 600 fell by -0.13%, with real estate down by -3.83%, utilities down by -3% and financials losing -1.08%. The energy sector gained +1.61% due to high oil prices, followed by healthcare which edged up +0.49%. Goldman Sachs commented on the region’s outlook, “We estimate that the interventions will raise the public deficit to 7.2% of GDP for 2022/23 and 5.3% of GDP in 2023/24, raising the debt ratio to 104.3% by 2024.” The FTSE fell by -0.5%, the CAC was down -0.3% while the DAX fell -0.7%. The UK pound continues to be the target of bearish forecasts, with Morgan Stanley forecasting the currency to reach parity with the USD by this year-end. ANZ chief economist Richard Yetsenga forecasts a ‘shallow recession’ in the Euro area, while the US dollar continues to gain momentum.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX is set to open lower, with ASX futures down -40 points or -0.62% to 6,466. The ASX closed +0.4% higher on Tuesday boosted by materials and energy which rose +2.57% and +1.72% respectively, offsetting the declines in real estate of -2.08%. Coal and lithium stocks were the biggest gainers on Tuesday after heavy falls on Monday, Whitehaven Coal rose by +6.8%, Pilbara Minerals and New Hope both gained +6.1%, Rio Tinto increased by +3%, and BHP Group climbed +2.8%. Lithium hopeful Atlantic Lithium’s debut on the ASX finished with the stock price declining -3% to 0.56c. MetalsGrove Mining doubled its value after identifying significant lithium deposits at the Coodina project. Santos gained 1% after selling 5% stake in the company’s PNG LNG project to Papua New Guinea based Kumul for $55 million. Star Entertainment continued to fall by -1% after the company revealed a remediation plan, as a part of a regulatory inquiry against the casino group. Synlait Milk fell by -4.4% despite a net profit of $8.5 million in 2022, more than triple the figure from last year. The yield on the Australian 10-year bond rose +3.7 basis points to 4.02%, with the local currency receding -0.37% to 0.6432 ahead of this morning’s release of August retail sales expected to show an increase of +0.40% over the month.

In commodities, rumors of sabotage on the Nord Stream pipeline made headlines, as Sweden launched a preliminary probe into the incident. A Swedish official commented, “We have established a report and the crime classification is gross sabotage”. Oil prices soared on Tuesday, based on Hurricane Ian’s potential impact on output from the US Gulf of Mexico, as well as supply cuts from OPEC+ which is set to meet on October 5th. WTI Crude and Brent Crude jumped +1.93% and +2.19% to $78.21 and $85.90 respectively. In precious metals, spot gold was up +0.29% to $1,627.2, spot silver rose by +0.12% to $18.38 while Bitcoin declined -0.7% to US$19,073. Iron ore futures in Singapore climbed +1.71% on Tuesday although are -0.28% lower this morning at US$96.95 and copper rose +0.29%.

Economic Calendar:

- Fed Daly Speech 10:35

- Australian Retail Sales (MoM Aug) 11:30

- German GfK Consumer Confidence (MoM Oct) 16:00

- ECB President Lagarde Speech 17:15

- US Retail Inventories Ex Autos (MoM Aug) 22:30

- Fed Bostic Speech 22:35

- Fed Bullard Speech 00:10

- Fed Powell Speech 00:15

- Fed Bowman Speech 01:00

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.