Equities extended weakness on Thursday as yields climbed while several other major central banks followed the Federal Reserve in raising interest rates.

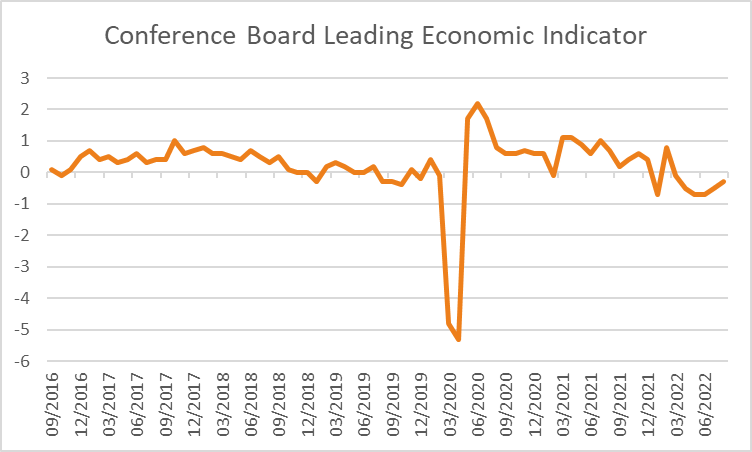

The S&P 500 closed -0.85% lower, with consumer discretionary falling -2.16%, financials down -1.66% and industrials down -1.49%. The Dow fell by -0.35% while the Nasdaq Composite declined -1.37% along with the Russell 2000 -2.26% however despite the decline in equities the VIX finished -2.29% lower at 27.35. The share price of large-cap technology stocks fell, with Tesla dropping -3.7%, Amazon falling by -1.5% and Apple declining -0.7%. Analysts at BNY Mellon Investor Solutions commented on expectations, “Our expectation is that it’s going to be a risk-off sentiment until we start to see signs that this restrictive policy is actually doing what the Fed says it’s going to do”. Evercore’s Chief Equity Strategist Julian Emanuel stated he expects a “full retest” of the June lows in the weeks ahead, revising his year-end forecast of the S&P 500 lower to 3,975 from 4,200. In economic data, Jobless claims in the US rose by 5000 to 213k, below forecasts of 218k while the Conference Board’s leading index for August improved less than expected to -0.3% compared to estimates of -0.1% and a prior reading of -0.5% suggesting the outlook for economic growth is deteriorating despite the labour market continuing to remain robust. The yield on the 2-year US treasury bond rose 5.5 basis points to 4.105, the 10-year bond yield rose 16 basis points to 3.692 while the 30-year bond yield was +13.3 basis points higher at 3.636%.

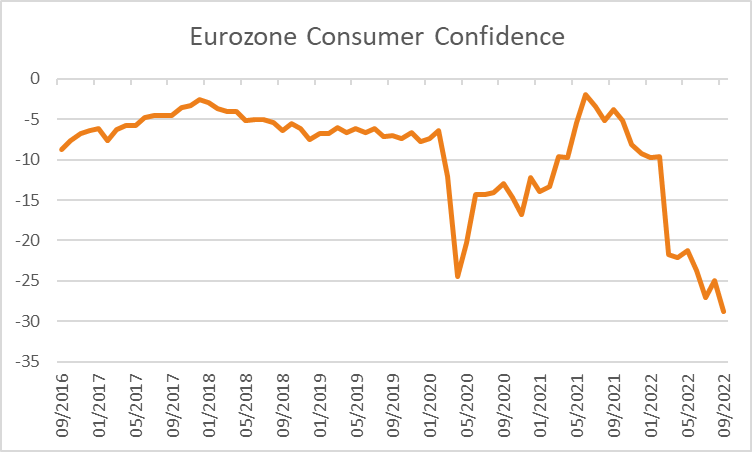

European markets dropped amid growing fears of a recession and ongoing energy crisis as winter approaches highlighted by consumer confidence for September declined more than expected to -28.8 compared to estimates of -25.8. The Euro SXXP 600 fell -1.62%, with energy the only sector rising by +0.17. The index’s biggest declines were seen in the interest rate-sensitive sector, namely real estate and information technology, sinking -4.34% and -4.1% respectively, while consumer discretionary declined by -2.58%. The Dax declined -1.84%, weighed down by the real estate sector which fell -4.29% technology falling -2.94%, and healthcare -2.68%. Traders are expecting a further hike in interest rates by the ECB to 3% by May. The FTSE dropped -1.08% after the Bank of England announced raising interest rates by 0.5% to 2.25%. The Swiss National Bank also opted to raise the interest rate by 0.75%, after the Fed’s raised the cash rate on Wednesday. Oanda’s Edward Moya commented, “Most of these rate hikes around the world are not done yet which means the race to restrictive territory won’t be over until closer to the end of the year”.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX was closed on Thursday and is set to open lower today as ASX futures were down 14 points or 0.2% to 6,631 following a -0.67% decline on Wednesday. The local currency edged 0.2% higher to 0.6644 an in focus today is the release of manufacturing and services PMI for September at 09:00 AEDT.

In commodities, the oil prices rose with WTI crude and Brent crude both increasing by +0.54% and +0.50% to $83.39 and $90.28 a barrel respectively. Precious metal prices were mixed, with spot gold falling -0.04% to $1,673, spot silver gaining +0.46% along with bitcoin which gained +1.82% to $19,270. Copper prices finished -0.23% lower extending a run of losses to four consecutive sessions, while iron ore futures in Singapore are +0.75% higher at US$99 this morning having gained +2.72% on Thursday.

Economic Calendar:

- Australian PMI (MoM Sep) 09:00

- Eurozone PMI (MoM Sep) 18:00

- S. PMI (MoM Sep) 23:45

- Fed Chair Powell Speech 04:00

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.