U.S. equities gained on Wednesday in a slow session with traders likely hesitant to make big bets ahead of Jerome Powell’s speech on Friday at the Federal Reserve’s Jackson Hole Symposium.

According to BMO Capital Markets’ Ian Lyngen ““It’s safe to assume one of Powell’s objectives will be to communicate that there remains work to be done to combat inflation and the hiking cycle isn’t nearing its end. At least not yet”. There has been no shortage of Federal Reserve policy makers leading up to the event reiterating that rates need to tighten to bring inflation back under control with Minneapolis Fed President Neel Kashkari late on Tuesday saying it is “very clear” officials need to tighten noting “By many, many measures we are at maximum employment and we are at very high inflation. So this is a completely unbalanced situation, which means to me it’s very clear: We need to tighten monetary policy to bring things into balance”.

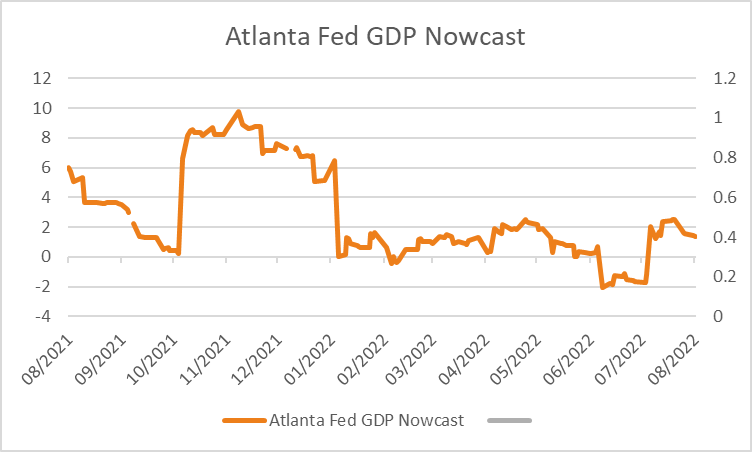

The S&P500 rose +0.29% with all sectors positive with financials +0.52% and energy +1.20% the biggest contributor to the index’s gains with 71% of stocks trading higher. The Dow Jones also rose +0.18%, as did the Nasdaq Composite +0.41% and Russell 2000 +0.84% with the VIX retreating -5.35% to 22.82. Meanwhile, Treasury yields rose ahead of the symposium with the 2-year rate up +6.9 basis points along with the 10 and 30-year rates by +6.3 and +6.2 basis points respectively after a week 5-year Treasury auction. Elsewhere in economic data, durable goods orders for July were unchanged following a +2.2% gain in June, missing estimates of +0.6% while a core measure that excludes transport rose +0.3% compared to +0.2% forecast. In focus tonight is the second reading of Q2 GDP expected to show the economy contracted at a -0.8% annualised pace, a second consecutive quarterly decline meeting the technical definition of a recession, while the Atlanta Fed’s GDP now forecast is predicting a +1.38% gain for the economy in Q3.

European equities were mixed after weaker PMI reports on Tuesday signalling the growing probability of a recession, particularly in the U.K and highlighted by the Euro’s recent move below parity with the U.S. dollar. The Euro Stoxx 600 edged +0.16% higher along with the DAX +0.20% and CAC +0.39% while the FTSE100 slipped -0.22%. According to analysts at Swissquote “The softer euro could’ve normally given a boost to European stocks, but understandably, no one wants to stomach the risks of the deepening energy crisis”. In focus tonight is the final reading of German GDP For Q2 expected to show economic growth was unchanged over the quarter and rose +1.4% over the year, followed by the German Ifo business climate survey for August expected to weaken modestly. Finally, the latest policy minutes from the ECB will be released at 21:30 AEDT.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX looks set to open higher this morning with ASX200 futures up +29 points or +0.42% to 6,932. The index rose +0.52% on Wednesday lifted by materials +1.09% and energy +2.84% while consume staples lagged -1.31%. Shares in WiseTech Global jumped +12.8% following the release of full-year results that saw net profit climb by +80% to $194.6m with CEO Richard White noting “In an environment of persistent supply chain constraints, inflationary pressures and COVID-related business disruption, to have delivered these outcomes is a real testament to the strength of our business”. Shares in Iluka climbed +9.8% after doubling its interim dividend to $0.25 reflecting higher commodity prices boosting revenue from material sands in the half year ending June 30 by +30%. Meanwhile the Australian dollar is -0.29% weaker at 0.6911 while the 10-year government bond yield climbed +5 basis points to 3.629%.

Oil prices extended a recent bounce with both WTI and Brent crude rising +1.69% and +1.47% overnight to US$95.32 and US$101.69 a barrel. Iron ore futures in Singapore gained +0.44% on Wednesday and are a further +0.93% higher this morning at US$104.65 while copper fell -1.39%. Gold rose +0.23% to US$1,752 an oz with silver unchanged and Bitcoin rising +1.11% to US$21,716.

Economic data:

- NZ Retail Sales (QoQ Q2) 08:45

- German GDP Final (QoQ Q2) 16:00

- German Ifo Business Survey (MoM Aug) 18:00

- ECB Policy Minutes 21:30

- U.S. GDP 2nd Estimate (QoQ Q2) 22:30

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.