U.S. equities rallied on Friday, supported by a decline in Treasury yields and better-than-expected consumer sentiment data.

The S&P500 climbed +1.73% on Friday in broad-based breath with 94% of stocks finishing higher and all sectors positive paced by consumer discretionary +2.30% and technology +2.07%. The Dow Jones also gained +1.27%, as did the Nasdaq Composite +2.09% and Russell 2000 +2.09% with the VIX retreating -3.32% to 19.53. The S&P500 has now gained +17.7% since the June lows driven by better-than-expected earnings as well as signs price pressures have peaked, providing the Federal Reserve with room to ease off aggressive rate increases in the coming months as economic data weakens. Ahead for the week, investors will be focused on the release of retail sales for July on Wednesday expected to be little changed over the month as well as the release of the latest Federal Reserve policy minutes followed by initial jobless claims on Thursday and the Conference Board’s leading index for July as well as several speeches by members of the Federal Reserve.

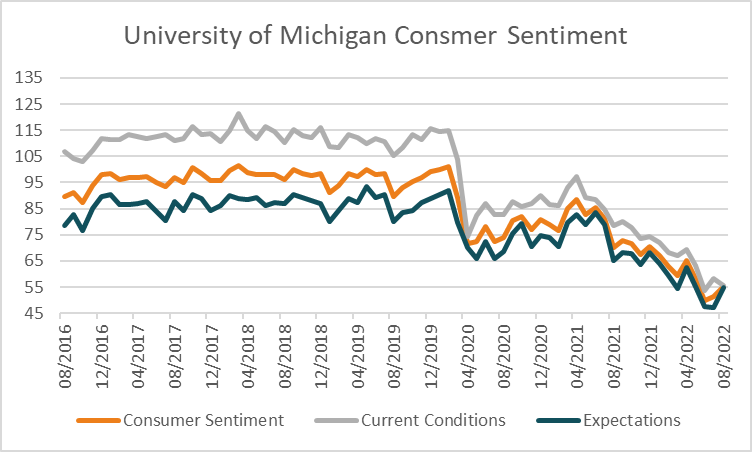

The University of Michigan consumer sentiment survey for August increased to 55.1, an improvement from 51.5 previously and above estimates of 52.5 having reached a record low of 50 in June. The survey showed the median expected year-ahead inflation rate eased to 5.0% from 5.2% on lower gasoline prices while longer-term expectations of inflation over 5-10 years remained anchored edging modestly higher to 3.0% from 2.9% previously. Elsewhere, President of the San Francisco Federal Reserve Mary Daly said a slowdown in price pressures may mean it is appropriate to slow the pace of rate increases to 0.5% in September but noted the fight against inflation is far from over.

European equities also finished higher on Friday with the Euro Stoxx 600 up +0.16% along with the DAX +0.74%, CAC +0.14%, and FTSE100 +0.47% with major benchmarks higher. Ahead for the week, investors will be focused on the release of Eurozone ZEW economic sentiment for August expected to modestly improve but remain deep in negative territory on Tuesday as well as Eurozone GDP on Wednesday forecast to show the economy expanded +0.7% over the quarter from +0.5% previously. Data on Friday showed Eurozone industrial production for the 12 months to June was higher than expected, growing +2.4% from +1.6% previously compared to estimates of +0.8%. The Euro weakened -0.59% on Friday to 1.0259 along with the Pound -0.55% to 1.2138.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX is expected to open +39 points or +0.56% higher this morning with ASX200 futures finishing at 6,973 on Friday. The index declined -0.54% on Friday weighed by materials -0.74% and health care -1.38% while energy outperformed +2.31%. Coal miner Stanmore Resources was a notable performer surging nearly +11% after posting record half-year profits and announcing it had acquired the remaining 20% stake in South Walker Creek and Poitrel coal miners from BHP Mitsui for US$380m. Ahead for the week, Tuesday will bring the release of the RBA’s latest policy minutes followed by the Westpac leading index for July and wage growth data for Q2 on Wednesday. Thursday will be the main focus with the release of employment data for July expected to show +26.5k jobs were added with the unemployment rate remaining stable at +3.5%.

Oil prices finished lower on Friday with both WTI and Brent crude down -2.38% and -1.46% respectively to US$92.09 and US$98.15. According to TD Securities, “oil markets are nearing a critical pivot point. The Iranian nuclear deal has long been a wildcard for oil markets, but negotiations could finally be nearing a conclusion, with Washington and Tehran now reviewing a final draft for a potential deal”. Iron ore futures weakened -1.70% on Friday and are a further -0.56% weaker this morning at US$109.75 with weaker demand from China offsetting an increase in production and mill margins. Gold rose +0.71% on Friday to US$1,802.40 an oz, with silver also rising +2.52% to US$20.82 with Bitcoin little changed on Friday and edging +0.35% higher over the weekend to US$24,320.

Economic data:

- Chinese Fixed Asset Investment, Industrial Production and Retail Sales (YoY Jul) 12:00

- U.S. NAHB Housing Market Index (MoM Aug) 00:00

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.