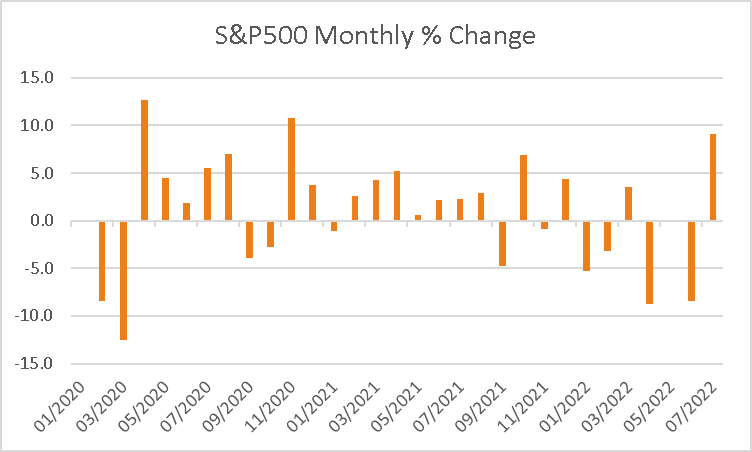

U.S. equities finished higher on Friday, posting their best monthly gain since November 2020 boosted by gains in mega-cap stocks.

The S&P500 rose +1.42% boosted by consumer discretionary +4.27% and technology +1.55% with energy also a notable performer up +4.51% on higher oil prices. The Dow Jones also gained +0.97%, as did the Nasdaq Composite +1.88% and Russell 2000 +0.42% with the VIX -4.7% lower at 30.57. Both Amazon and Apple posted strong gains after posting rising revenue, countering fears of a profit slowdown at a time when the industry is slowing hiring, with Amazon shares rising +10.11% and Apple +3.04% higher.

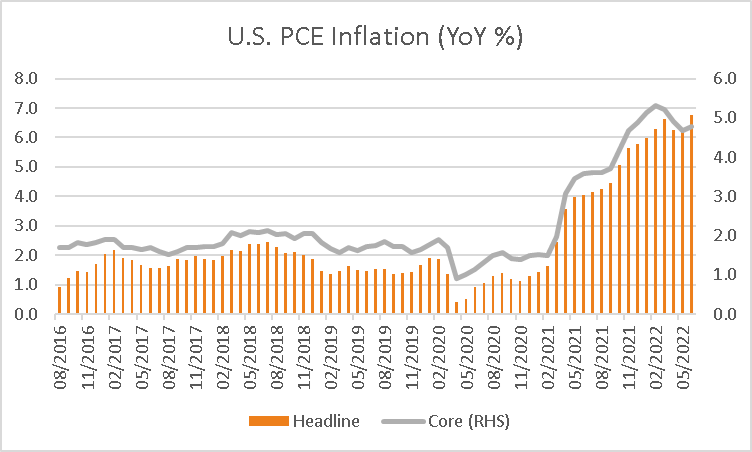

In economic data, U.S. PCE inflation rose with headline prices up +6.8% over 12 months as forecast from +6.3% previously, while core inflation rose +4.8% modestly higher than the +4.7% forecast. Slightly higher than forecast gains over the month of +1% and +0.6% previously highlighted inflation pressure remains, and despite recent comments from Jerome Powell that the rates have reached their “neutral level”, the central bank is likely to continue raising rates until inflation moves back towards target, although will be data dependant rather than on autopilot. Nominal spending rose +1.1% in June, slightly above consensus at +1% although only gaining +0.1% on an inflation-adjusted basis, with consumers dipping into savings and demanding higher wages. Bloomberg economists noted “the downward trajectory of inflation-adjusted services spending toward the end of the second quarter means less momentum for consumption and the overall economy entering the second half of the year. Despite relatively positive headlines, details of the June spending report look weaker than the headline and raise the chance of a third consecutive drop in real GDP this quarter”. Elsewhere, the University of Michigan’s final consumer sentiment reading for July was modestly higher than forecast at 51.5 compared to 51.1 estimated and a prior reading of 50 in June.

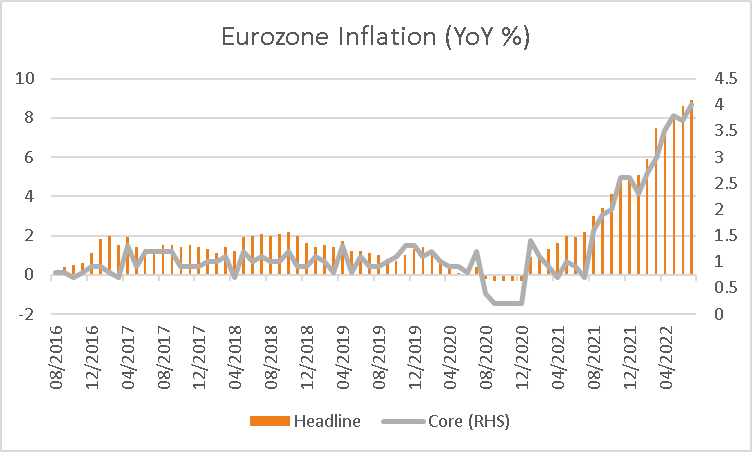

European equities also posted their best month since November 2020 as investors turned optimistic about corporate earnings and the potential for the Federal Reserve to slow rate hikes amid recession fears. The Euro Stoxx 600 gained +1.43% on Friday along with the DAX +1.52%, CAC +1.72% and FTSE100 +1.06% with benchmarks across the region higher. Higher than forecast inflation data on Friday for the Eurozone meanwhile is likely to keep the ECB on a hawkish trajectory this year even in the face of a likely recession according to HSBC Asset Management strategist Hussain Mehdi. Core prices for the 12 months to July rose +4%, higher than the +3.8% forecast while headline prices gained +8.9% compared to +8.6% estimated. Elsewhere, the second estimate of Q2 GDP for the Eurozone showed the economy expanded +0.7% over the quarter, higher than the +0.2% estimated and rose +4% over the year compared to +3.4% forecast.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

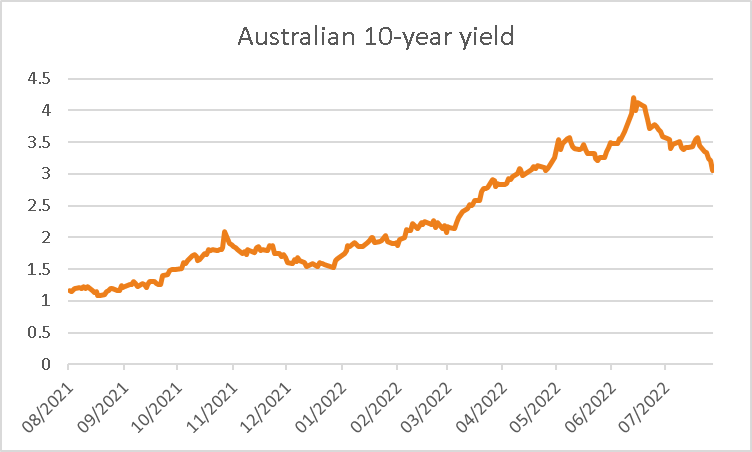

The ASX looks set to follow global markets higher this morning with ASX200 futures up +46 points or +0.67% to 6,906. The index rose +0.80% on Friday boosted by gains in materials +0.98% and real estate +2.96% while health care was the only sector, down -0.06%. In focus this week is a rate decision by the RBA on Tuesday where the central bank is expected to raise rates by +0.5% taking the cash rate to +1.85%. Following weaker than expected inflation data last week traders have pared back their hawkish views for the cash rate, now expected to peak at a lower +3.2% by April 2023 with expectations of a rate cut by the end of 2023 growing. The Australian dollar was little changed at 0.6985 on Friday while the 10-year government bond yield weakened -15 basis points to 3.056% having recently traded over +4% in late June.

Oil prices were higher on Friday with both WTI and Brent crude up +2.28% and +2.10% to US$98.62 and US$103.97 respectively. Base metals were higher over the week with aluminium up +0.53% along with copper +6.24%, lead +0.84%, nickel +6.77%, tin +0.40% and zinc +10.56%. Iron ore futures in Singapore fell -3.12% on Friday although are +0.92% higher this morning at US$116.05. Gold was +0.58% higher on Friday at US$1,765 an oz along with silver +1.73% to US$20.36 while Bitcoin was -0.34% lower on Friday and is a further -0.57% lower over the weekend at US$23,820.

Economic data:

- Australian Manufacturing PMI Final (MoM Jul) 09:00

- German Retail Sales (YoY Jun) 16:00

- Eurozone Manufacturing PMI Final (MoM Jul) 18:00

- Eurozone Unemployment Rate (MoM Jun) 19:00

- U.S. ISM Manufacturing PMI (MoM Jul) 00:00

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.