U.S. equities weakened on Thursday as data showed inflation continue to rise ahead of key unemployment data on Friday, while Treasury yields were lower, driven by declines in longer-dated rates flattening the yield curve.

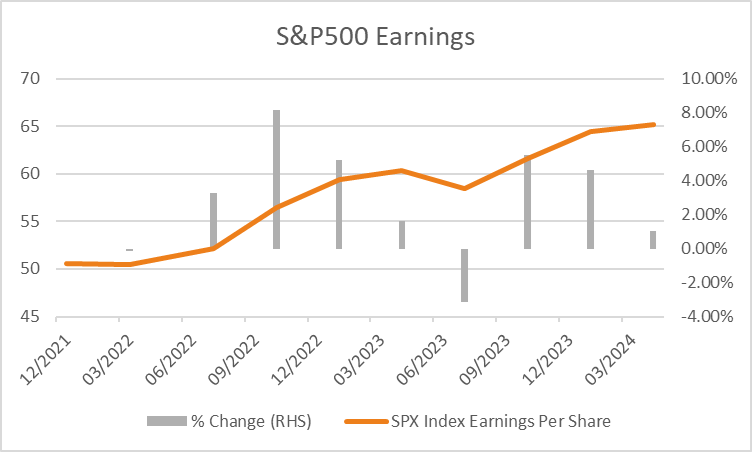

The S&P500 weakened -1.57% taking its quarterly loss to -4.95% with declines on Thursday driven by technology -1.59%, financials -2.32% and consumer discretionary -1.95% with 86% of stocks trading lower. The Dow Jones also retreated -1.56%, as did the Nasdaq Composite -1.54% and Russell 2000 -1.0% with the VIX climbing +6.36% to 20.56. Other than key economic data this week, investors will be focused on the release of Q1 2022 earnings over the coming weeks with the average analyst estimate for S&P500 earnings to grow by +3.28% to 52.17 from 50.51 in Q4 2021.

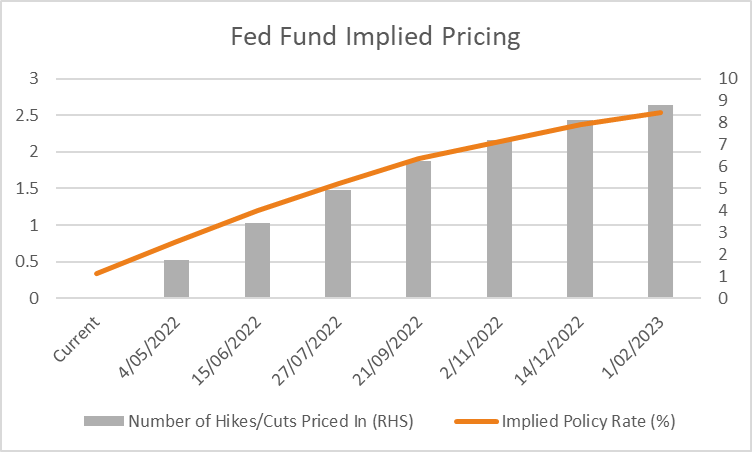

Inflation continued to rise for the year to February data showed on Thursday, with core prices rising +5.4% over the year from +5.2% previously, modestly below estimates of +5.5%. Meanwhile, headline prices rose +6.4% in line with estimates from a revised higher +6% in January. Personal income rose +0.5% over the month in line with estimates and up from +0.1% previously, while spending was weaker than expected at +0.2% versus forecasts of +0.5% from a revised +2.7% in January. Elsewhere, initial jobless claims were in line with estimates of +197k with a reading of +202k from +188k previously. The 2-year yield rose +0.8 basis points to 2.314% while the 10 and 30-year rates declined -2.2 and -3.4 basis points respectively, flattening the yield curve as the market continues to signal concerns about the outlook for economic growth. Fed Fund futures pricing continues to price in the likelihood of a 50-basis point rate hike at the Fed’s May meeting, currently implying a hike of +0.44% with a total of 8 hikes expected before the end of 2022.

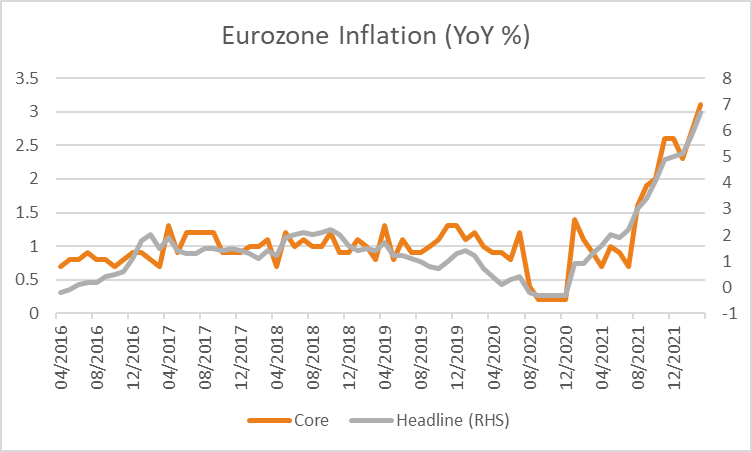

European equities were broadly lower with the Euro Stoxx 600 down -0.94%, as was the DAX -1.31%, CAC -1.21% and FTSE100 -0.83% with major benchmarks across the region all lower. Talks between Russia and Ukraine are set to resume on Friday, seeking to build on earlier talks this week that failed to yield significant progress while Russian President Vladimir Putin said Russia will continue supplying gas to Europe amid earlier fears it would restrict energy, although demands customers pay in rubles. In economic data, German unemployment remained stable at 5% as forecast with unemployment declining by -18k in line with estimates of a -20k decline. Eurozone unemployment declined to 6.8% from 6.9% previously, missing estimates for a larger decline to 6.7%. 10-year government bond yields were broadly lower across Europe, ranging from -5.6 basis points in the U.K. to -11.4 in Sweden, with the Euro weakening -0.78% to 1.1072 while the Pound edged +0.10% higher to 1.3147. The focus on Friday will be Eurozone inflation data for the year to March, expected to show core prices rising to +3.1 from +2.7% previously and headline prices climbing +6.6% from +5.9% previously.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX looks set for a weaker open this morning with ASX200 futures down -42 points or -0.56% to 7,437. The index reversed initial gains on Thursday, falling in the final hours of trading to decline -0.20% into the close weighed by financials -0.99% and consumer discretionary -1.30% while materials +1.46% outperformed as the prospect of further sanctions on Russia pushed commodity prices higher. Oil producers were weaker after news the U.S. was considering releasing as much as 180m barrels of oil from its strategic reserves with WPL -1.35% lower, as was STO -1.65% and BPT -2.20%. The Australian dollar is -0.25% weaker at 0.7490 this morning ahead of manufacturing PMI for March at 09:00 AEDT expected to rise modestly to 57.3 from 57 previously, firmly within expansionary territory.

Oil prices slumped on news that the U.S. may release strategic oil reserves with both WTI and Brent crude down -6.07% and -5.24% to US$101.26 and US$105.60. While the move is seen as likely cooling prices in the short-term, those barrels will need to be replaced likely driving prices higher in the future. Iron ore futures in Singapore weakened -0.24% on Thursday although are trading +1.07% higher this morning at US$161.35. Gold rose +0.22% to US$1,937 while silver declined -0.29% to US$24.80 along with Bitcoin -3.27% to US$45,733.

Economic data:

- Australian Manufacturing PMI (MoM Mar) 09:00

- Eurozone Manufacturing PMI (MoM Mar) 19:00

- Eurozone Inflation (YoY Mar) 20:00

- U.S. Non-farm Payrolls (MoM Mar) 23:30

- U.S. ISM Manufacturing PMI (MoM Mar) 01:00

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.