U.S. equities retreated on Thursday as hopes of a de-escalation of the war in Ukraine faded, while oil gained after U.S. stockpiles declined more than forecast.

The S&P500 declined -by 0.63% weighed by declines in technology -by 1.54% and consumer discretionary -by 1.69% with 67% of stocks lower with energy +1.10% and utilities +0.75% the top-performing sectors. The Dow Jones also declined -by 0.19%, as did the Nasdaq Composite -1.21% and Russell 2000 -by 1.97% with the VIX climbing +2.22% to 19.32. Lithium miners were notable performers, rising after President Joe Biden’s plans to invoke Cold War measures to encourage domestic production of critical materials for electric vehicles that would see companies gain access to US$750m to fund production at current operations, productivity, safety upgrades and feasibility studies.

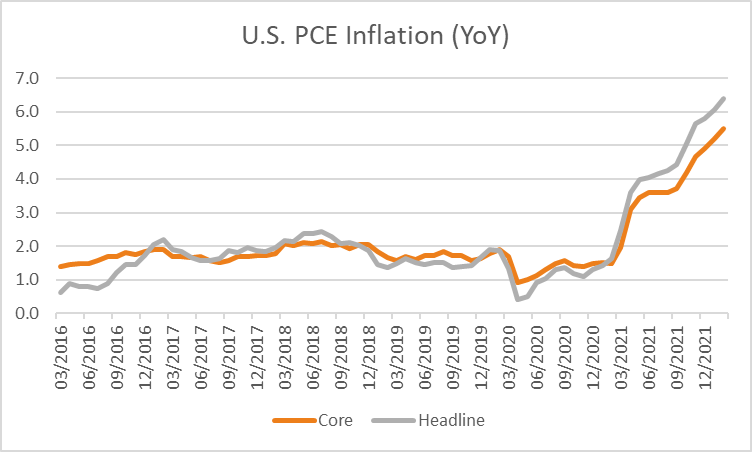

In economic data, the final reading of fourth-quarter 2021 GDP was lower than forecast at a +6.9% annualised rate versus estimates of +7.1% although up from +2.3% in the third quarter. ADP private employment for March rose +455k in line with forecasts of +450k from a slightly revised higher +486k in February. The data comes ahead of non-farm payroll data on Friday which is expected to show +490k jobs were added in March and the unemployment rate edged lower to +3.7% from +3.8% previously. In focus, tonight is PCE inflation data which is forecast to show core prices rose +5.5% over the year to February from +5.2% previously, and headline prices rise +6.4% from +6.1% previously.

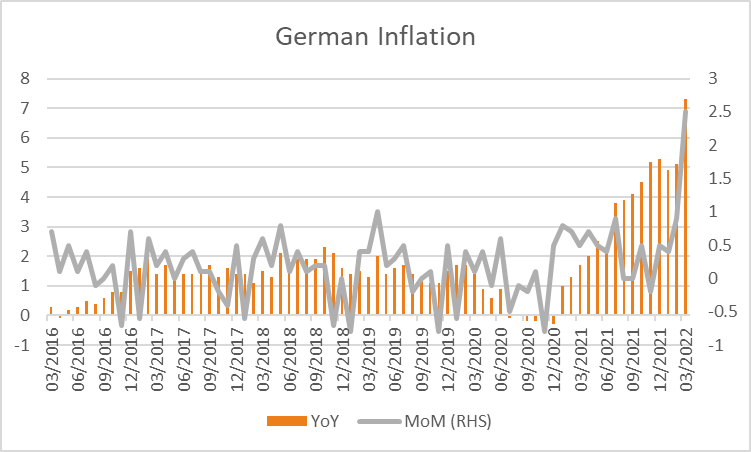

European equities were generally lower with the Euro Stoxx 600 declining -0.41% as did the DAX -1.45%, CAC -0.74% and most benchmarks across the region negative, except the FTSE100 which gained +0.55%. Weighing on sentiment was higher than forecast German inflation as well as fading sentiment of a de-escalation of the war in Ukraine with Russian forces regrouping to focus on taking the Donbas region. German inflation rose +7.3% for the year to March from +5.1% in February, higher than the +6.3% forecast, gaining +2.5% over the month versus expectations of a +1.6% gain. Eurozone consumer confidence for March weakened to -18.7 in line with estimates and down from -8.8 previously with economic sentiment also weaker at 108.5 from 113.9 previously as was industrial sentiment at 10.4 from 14.1 prior. In focus on Friday is inflation for the Eurozone, forecast to show core prices rose +3.1% for the year to March from +2.7% previously and headline prices rising to record levels at +6.7% from +5.8% in February.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX200 looks set to edge higher this morning with ASX200 futures +10 points or +0.13% higher at 7,494. The index gained +0.67% on Thursday boosted by financials +0.88% and technology +3.84% which more than offset a -0.29% fall in materials. Companies with exposure to fuel benefited from the announced tax cut on fuel with Eagers Automotive rising +2.9%, as did GUD Holdings +2.2% and Bapcor +1.4%. Announced cash handouts benefited retailers with Kogan rising +5%, as did Harvey Norman +1.8% and Wesfarmers +1%. VGI Partners, the listed hedge fund was a notable performer surging +25% after announcing it had secured a deal to merge with rival Regal Funds Management. The Australian dollar is +0.08% higher this morning at 0.7515 while the 10-year yield declined -10.5 basis points on Thursday to 2.793%.

Oil prices climbed with both WTI and Brent crude +3.10% and +2.24% higher at US$107.47 and US$112.70 a barrel. The gains follow tighter than expected U.S. stockpiles with declined -3.449m barrels for the week ending 25th March compared with estimates of a -1.022m barrel draw offsetting a surprise gain of +785k barrels of gasoline against estimates of a -1.744m barrel decline. Iron ore futures in Singapore rose +3.49% on Wednesday and are a further +1.23% higher this morning at US$162. Gold rose +0.76% to US$1,934 as did silver +0.41% to US$24.87 while Bitcoin weakened -0.80% to US$47,106.

Economic data:

- Australian Building Permits (MoM Feb) 11:30

- Chinese PMI (MoM Mar) 12:30

- U.K. GDP (YoY Q4) 17:00

- German Unemployment (MoM Mar) 18:55

- Eurozone Unemployment (MoM Feb) 20:00

- U.S. Core PCE (YoY Feb) 23:30

- Fed Williams Speech 00:00

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.