U.S. equities extended gains on Tuesday while yields mostly declined with the closely watched 2-10 year spread briefly inverting while sentiment was lifted on hopes of a de-escalation of tensions in Ukraine.

The S&P500 advanced +1.23% in broad-based buying with 87% of stocks rising boosted by technology +2.06% and consumer discretionary +1.54% while energy -0.44% was the only negative sector. The Nasdaq Composite also gained +1.84%, as did the Dow Jones +0.97% and Russell 2000 +2.65% with the VIX retreating -3.46% to 18.95. While talks between Ukraine and Russia failed to yield a breakthrough, sentiment was lifted following small positive indications with Russia announcing a de-escalation of tensions as its advance of the capital Kyiv stalled.

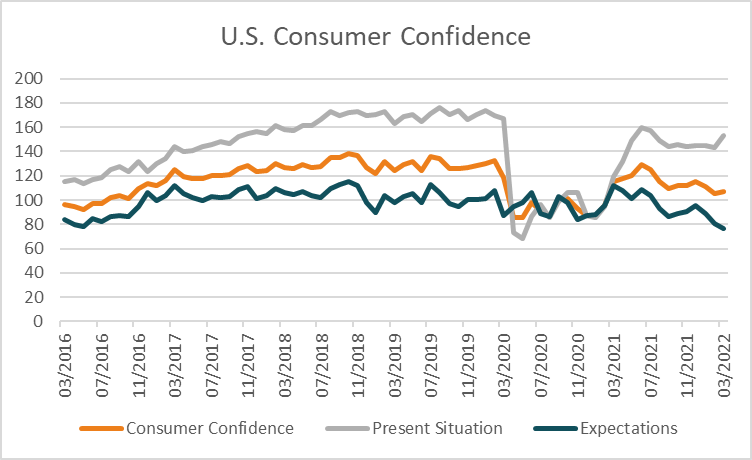

The 2-year yield traded -0.4 basis points lower at 2.361% with both the 10 and 30-year rates down -7.3 and -4.5 basis points respectively. The closely watched 2-10 yield spread briefly inverted before edging back to +0.0026%. Historically this has been a strong indication that market is worried about a recession in the near future, although a case could be made that longer-dated yields would be higher and the curve not inverted if it wasn’t for the Fed’s large QE program in the wake of the pandemic. Still, it suggests that the market is worried the Fed will hike too aggressively, slowing economic growth and raising the risk of pushing the economy into a recession. While the market has factored in several more rate hikes this year, the focus is likely to increasing move towards the winddown of the Fed’s balance sheet and the impact it is likely to have. In economic data, the Conference Broad’s consumer confidence measure for March improved from a revised lower 105.7 in February to 107.2 in line with estimates of 107.

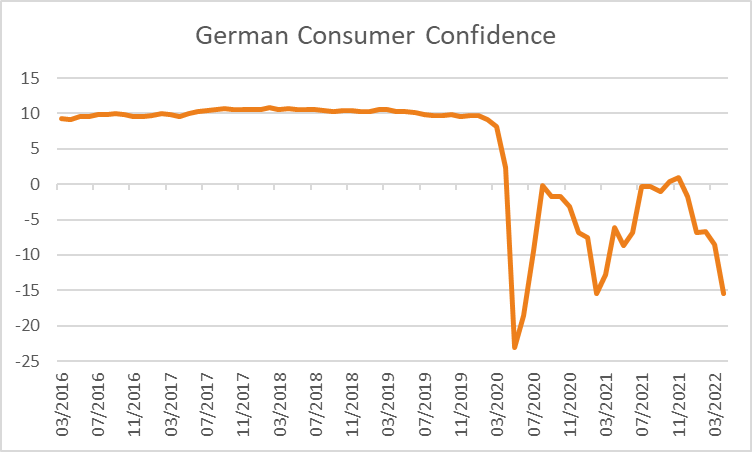

European equities were broadly higher following positive indications from talks over Ukraine. The Euro Stoxx 600 advanced +1.74%, as did the DAX +2.80%, CAC +3.08% and FTSE100 +0.86% with benchmarks across the region broadly higher. In economic data, the German GfK consumer confidence measure for April rose weakened further to -15.5 from -8.1 previously and more than the -14 forecast. 10-year bond yields across Europe were higher across the broad, ranging from +9 basis points in Switzerland to +0.9 in Italy, with the Euro strengthening +0.93% to 1.1087 and the Pound edged +0.08% higher to 1.3098.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX looks set to rise this morning with ASX200 futures up +56 points or +0.75% to 7,503 following the release of the Federal Budget on Tuesday night focusing on relieving the cost of living. The index rose +0.70% on Tuesday lifted by financials +0.57% and health care +1.80% while materials -0.18% and energy -0.55% lagged. Telix Pharmaceuticals was the top performer, rising +9.9% after the U.S. Food and Drug Administration granted organ drug designation relating to hematopoietic stem cell transplant. In economic data, retail sales were stronger than forecast for February rising +1.8% from a revised +1.6% in January and surpassing estimates of a +1% gain. The Australian dollar is +0.31% higher at 0.7512 and the yield on 10-year government bonds was little changed at 2.898%. The yield curve in Australia remains a long was from inverting with the 2-10 spread at 0..9475% although continues to flatten as the market prices in rate hikes by the RBA throughout this year.

Oil prices weakened overnight with both WTI and Brent crude -0.85% and -1.26% lower at US$105.06 and US$111.06 a barrel respectively. Iron ore futures in Singapore were -0.19% lower on Tuesday and are a further -0.21% lower at US$154.30 this morning. Gold edged -0.18% lower to US$1,919.25 as did silver -0.38% to US$24.78 and Bitcoin -0.65% to US$47,656.

Economic data:

- Australian Business Confidence (MoM Mar) 11:00

- Eurozone Consumer Confidence (MoM Mar) 20:00

- German Inflation (YoY Mar) 23:00

- U.S. ADP Employment (MoM Mar) 23:15

- U.S. GDP (QoQ Q4) 23:30

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.