Equities extended a rally on Tuesday while Treasury yields continued to climb as investors took comfort following recent comments by Fed Chair Jerome Powell that the Fed would act to tame inflation and remain behind the curve.

The S&P500 climbed +1.13% on Tuesday in broad-based buying with 72% of stocks higher as technology +1.42%, consumer discretionary +2.45% and communications +2.01% contributed the most to gains. The Dow Jones also rose +0.74%, as did the Nasdaq Composite +1.95% and Russell 2000 +1.08% with the VIX closing -2.89% lower at 22.85 having peaked at 36.45 recently.

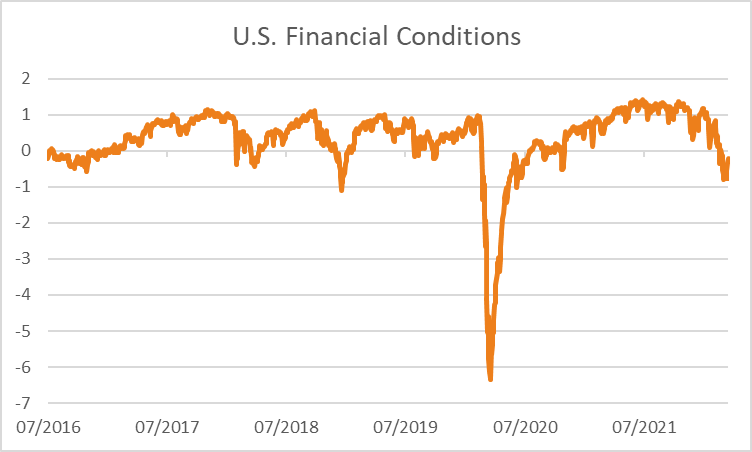

The 2-year Treasury yield rose +5.1% basis points to +2.166%, as did both the 10 and 30-year rates by +9.5 and +9.5 basis points respectively. Breakeven inflation rates were little changed pushing real yields higher across 5 and 10-years by +9 and +8.2 basis points to -1.20% and -0.552% respectively. While the Fed has only raised rates by +0.25% so far, traders are pricing in a further +7.5 hikes by the end of the year suggesting the Fed Funds rate will finish at +2.24% in 2022. Recently forward guidance by the Federal Reserve has already done a significant amount of work for the Fed, as financial conditions highlighted by the Bloomberg U.S. financial conditions index below show have already tightened from historic lows.

Speaking to Bloomberg on Tuesday, St. Louis Fed President James Bullard argued that “faster is better” when it comes to raising rates to put downward pressure on inflation, noting “history tells us that the faster we move to the situation, the better chance we will have of moving inflation back to target and getting a boom in the U.S. economy”. Bullard referred to the 1994 tightening cycle as the best analogy for engineering a soft landing where Alan Greenspan raised rates from 3% to 6%, containing inflation with the economy expanding over the next 10-years.

European equities also rose on Tuesday with the Euro Stoxx 600 rising +0.85%, as did the DAX +1.02%, CAC +1.17 and FTSE1100 +0.46% with major benchmarks broadly higher. While equities have erased declines following the invasion of Ukraine amid optimism over peace talks as well as cheap valuations, the outlook remains complex in the near term given higher energy costs, rising inflation, falling consumer sentiment and supply chain disruptions. 10-year government bond yields also rose across Europe ranging from +1.1 basis points in Spain to +9.5 in Sweden with the Euro edging +0.10% higher to 1.1027 as did the Pound, up +0.68% to 1.3258.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

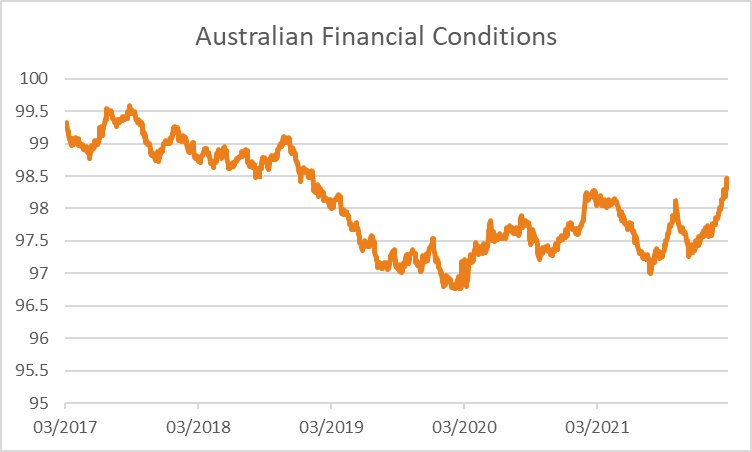

The ASX looks set to open higher with ASX200 futures up +31 points or +0.42% to 7,343. The index climbed +0.86% on Tuesday lifted by gains in materials +3.34% and financials +0.56% while breadth was mixed with only 54% of stocks rising. BHP was a major contributor rising +5.1% following higher commodity prices as well as Beijing announcing $532 billion in tax cuts. New Hope rallied +8.5% after reporting net profit for the six months to January 31st of $330.4 million compared to a $55.4 million loss previously while declaring a $0.17 dividend up from $0.13 previously as well as a special dividend of $0.13 per share. The Australian dollar is +0.91% higher at 0.7467 and the 10-year government bond yield climbed +14 basis points on Tuesday to 2.723%. Australian financial conditions also continue to tighten as shown by the Goldman Sachs Australian financial conditions index with further expectations the RBA will need to raise rates sooner than expected.

Oil edged pared initial gains to edge lower as Germany and Hungary put brakes on a potential embargo of Russian oil. Both WTI and Brent crude edged -0.32% and -0.30% lower to US$111.76 and US$115.27 respectively. Iron ore futures in Singapore declined -3.04% on Tuesday and are a further -0.30% weaker this morning at US$145.20. Gold traded -0.77% lower to US$1,920 as did silver -1.76% to US$24.76 while Bitcoin gained +3.26% to US$42,477.

Economic data:

- U.K. Inflation (YoY Feb) 18:00

- Fed Chair Powell Speech 23:00

- Eurozone Consumer Confidence (MoM Mar) 02:00

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.