U.S. equities extended gains for a fourth consecutive session on Friday, posting their best week since November 2020.

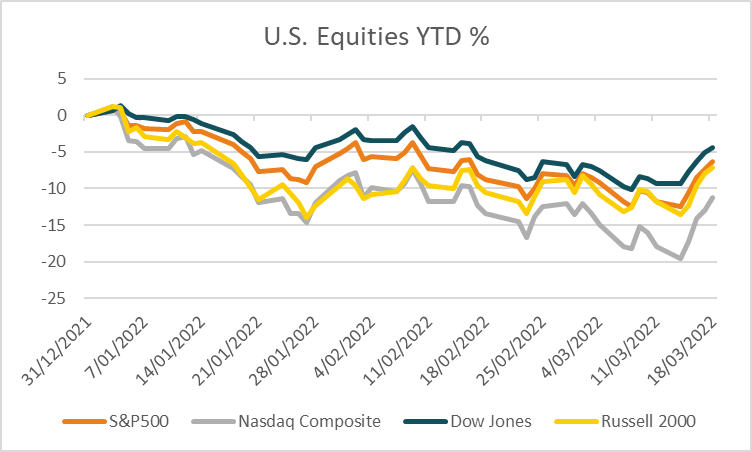

Following signs that selling pressure had become exhausted, U.S. equities have rallied strongly with the S&P500 rising +1.17% on Friday taking its weekly gain to +6.16%. The Dow Jones also closed +5.50% higher for the week, as did the Nasdaq Composite +8.18% and Russell 2000 +5.38% with the VIX retreating -22.37% to 23.87. From a technical perspective, with the S&P500 breaking upwards through initial resistance levels around 4,400 which also coincide with a higher high, an early indication of an uptrend forming, analysts are now looking for further gains towards 4,600. However, it is too soon to say whether the current bounce is a relief rally following heavy selling at the start of the year or a change in the trend direction. With key risks still on investors’ minds including inflation and war, markets are likely to remain headline-driven in the near term.

In economic data, the Conference Board’s leading index for February rose +0.3% as forecast from -0.5% previously. Several Federal Reserve members spoke on Friday with St. Louis President James Bullard saying he favours raising rates above 3% by the end of the year and urging a faster pace of tightening and balance sheet wind down. Governor Christopher Waller said Ukraine was the reason he didn’t push for a +0.5% increase at this week’s meeting but will not rule out such a move in coming meetings. Ahead for the week, investors will focus on a speech by Fed Chair Jerome Powell overnight and again on Wednesday. Durable goods orders for February will be released on Thursday night, expected to show a decline of -0.5% for the month, followed by the Markit Manufacturing PMI for March expected to show a decline while Friday will see the final reading of consumer sentiment for March.

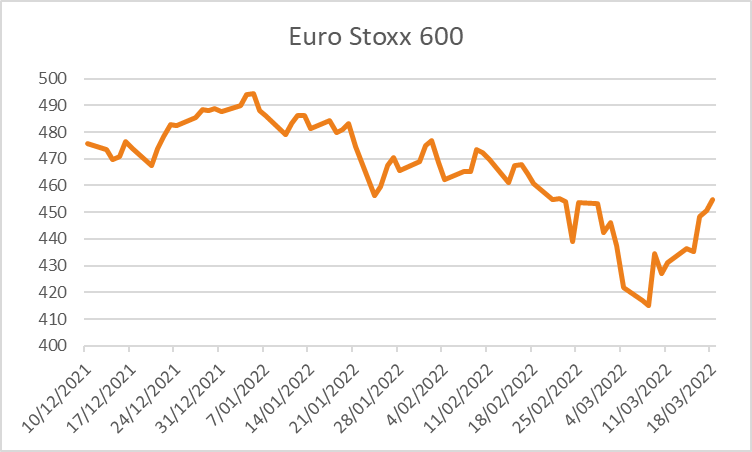

European stocks have now recouped their losses from the start of Russia’s invasion of Ukraine, posting their best week since November 2020. Reports that Russia had paid U.S. dollar to settle coupon payments due Wednesday on two Eurobonds also boosted sentiment, suggesting Russia will avoid defaulting on debt for now. The Euro Stoxx 600 rose +0.91% on Friday taking gains to +5.43% for the week with the DAX also rising +5.76% for the week, as did the CAC +5.75% and FTSE100 +3.48% with benchmarks broadly higher for the week. Ahead for the week investors will focus on consumer confidence for March on Wednesday night, followed by German and Eurozone PMI for March on Thursday and rounded off by the German Ifo Business Climate survey for March on Friday.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX looks set to open higher this morning with ASX200 futures +59 points or +0.81% higher at 7,323 at the close of trade last week. The index rose +0.60% on Friday extending a weekly gain to +3.27%, the third consecutive higher weekly close. Ahead in economic data for the week, RBA Governor Philip Lowe is due to speak on Tuesday followed by manufacturing and services PMI data for March on Thursday. The Australian dollar climbed +0.53% on Friday to 0.7415 with the yield on 10-year government bonds rising +6.9 basis points to +2.578%.

Oil prices rose on Friday with both WTI and Brent crude rising +1.67% and +1.21% although finished the week lower following heavy losses earlier in the week. Base metals were mixed with aluminium declining -2.93%, as did lead -3.14%, tin -4.07% and nickel slumped -23.22% hitting limit down on every session following the resumption of trading. Meanwhile, copper rose +1.45% along with iron ore futures in Singapore +1.45% although futures are down -0.78% in early trade this morning at US$152.30. Gold finished -1.09% lower at US$1,921 on Friday, along with silver -1.63% to US$24.96 while Bitcoin rose +2.53% and is little changed over the weekend at US$41,649.

Economic data:

- ECB President Lagarde Speech 18:30

- Fed Bostic Speech 23:00

- Fed Chair Powell Speech 03:00

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.