U.S. equities declined on Monday with Treasury yields climbing ahead of the Federal Reserves policy meeting overnight Wednesday, while commodities fell on restrictions in China to address rising Covid cases.

The S&P500 declined -0.74% paring initial gains of 1% as declines in technology -1.90% and consumer discretionary -1.75% weighed while financials +1.23% outperformed on rising yields. The Dow Jones was unchanged, while the Nasdaq Composite declined -2.04% as did the Russell 2000 -1.92% with the VIX rising +3.32% to 31.77. Initial gains were driven by hopes of a new round of talks between Russia and Ukraine before fading late in the session as investors await updated economic projections from the Federal Reserve overnight on Wednesday.

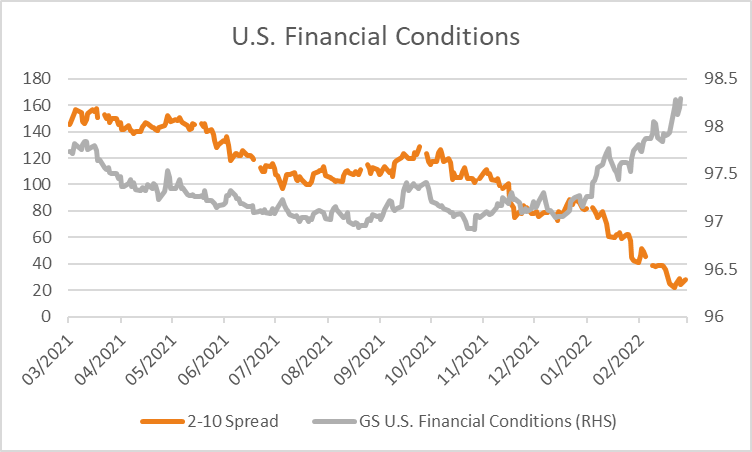

Traders are now pricing in seven rates hikes in 2022 as the central bank seeks to cool inflation that is at 40-year highs. The yield on 2-year Treasuries climbed +11.1 basis points to 1.859%, with the yield on both the 10 and 30-year rates rising +14.8 and +12.5 basis points respectively. The spread between the 2 and 10-year rates currently sits at 0.285% having reached as high as +1.57% in March 2021 with the flattening of the curve generally a sign the market is worried about the outlook for economic growth. Still, the curve has not yet inverted which typically signals the market expects a recession in the coming months. U.S. financial conditions continue to tighten as well, driven by rising yields, higher energy prices and weaker equities. Tonight will bring further insight into the outlook for inflation with U.S. producer prices for February expected to show a +0.9% increase over the month down slightly from +1% previously.

European equities rose on Monday on hopes of talks between Russia and Ukraine that could lead to an end to the multi-week war. The Euro Stoxx 600 rose +1.20%, as did the DAX +2.21%, CAC +1.75% and FTSE100 +0.53%. 10-year government bond yields in Europe also climbed ranging from +8.1 basis points in Switzerland to +11.9 basis points in Germany with the Euro rising +0.30% to 1.0945 while the Pound weakened -0.27% to 1.3002. Ahead in economic data U.K. employment for the 3-months to January is expected to show the unemployment rate edged lower to 4.0% from 4.1% previously with the number of employed increased by +30k. We’ll also see economic sentiment for both the Eurozone and Germany with the release of the ZEW economic sentiment surveys for March which is expected to show declines.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX looks set to open lower this morning with ASX200 futures down -61 points or -0.85% to 7,087. The index rose +1.21% on Monday boosted by financials +2.46% and health care +2.16% accounting for the majority of gains. A +5.5-basis point rise in 10-year government bond yields lifted major banks with CBA advancing +2.6%, as did NAB +1.5%, ANZ +2.8% and WBC +2.5%. A notable performer was Elders which climbed +11% after it expanded market share across most of its businesses, underpinned by cattle and sheep prices as well as growing demand for fertilizers and farm chemicals.

Oil prices declined overnight with other commodities following restrictions in China to deal with an outbreak of Covid cases clouds the nation’s economic outlook. China has placed over 17 million people in Shenzhen under a lockdown and forbade people from the Jilin province. Both WTI and Brent crude declined -6.74% and -5.98% respectively to US$101.94 and US$105.93 down from highs of US$130 last Monday. Iron ore futures in Singapore declined -6.58% on Monday and are a further -1.18% weaker this morning at US$145.50. Gold declined -1.83% to US$1,952 weighed by a rise in real yields, silver also declined -3.25% to US$25.03 while Bitcoin edged +0.34% higher to US$38,819.

Economic data:

- RBA Minutes 11:30

- Chinese Fixed Asset Investment, Industrial Production, Retail Sales (YoY Feb) 13:00

- U.K. Unemployment (3m Dec) 18:00

- Eurozone Economic Sentiment (MoM Mar) 21:00

- U.S. PPI (MoM Feb) 23:30

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.