Global equities declined on Friday with Treasury yields lower as investors bought havens with tensions over Ukraine continuing to weigh on sentiment.

The S&P500 declined -0.72% on Friday, taking a weekly loss to -1.58% with 66% of stocks lower on Friday as technology -1.10% and health care -0.82% weighed with consumer staples +0.11% the only positive sector. The Nasdaq Composite also declined -1.23%, as did the Dow Jones -0.68% and Russell 2000 -0.92% while the VIX was -1.28% lower at 27.75. The U.S. said Russia has massed as many as 190,000 personnel in and around Ukraine, while Russia continues to deny any plans to invade. U.S. foreign secretary Antony Blinken is due to meet Russian foreign minister Sergei Lavrov this week in Europe to discuss the situation amid reports of ceasefire violations between pro-Russian separatists and the Ukrainian military. U.S. markets are closed on Monday for a public holiday.

Chicago Fed President Charles Evans, one of the most dovish officials, called for a “substantial” policy shift on Friday while playing down the need for aggressive tightening. The comments did little to move Treasury yields with the market already pricing in nearly six rate hikes by the end of the year, with the first expected next month. Yields instead declined as investors sought safety amid geopolitical tensions. The 2-year yield was little changed at 1.469% with the 10-year down -3.2 basis points and the 30-year down -5.2 basis points and the U.S. dollar index rising +0.25% benefiting from its status as a haven. In economic data, the conference board’s leading index for January missed estimates of a +0.2% gain, declining -0.3% from a revised lower 0.7% previously.

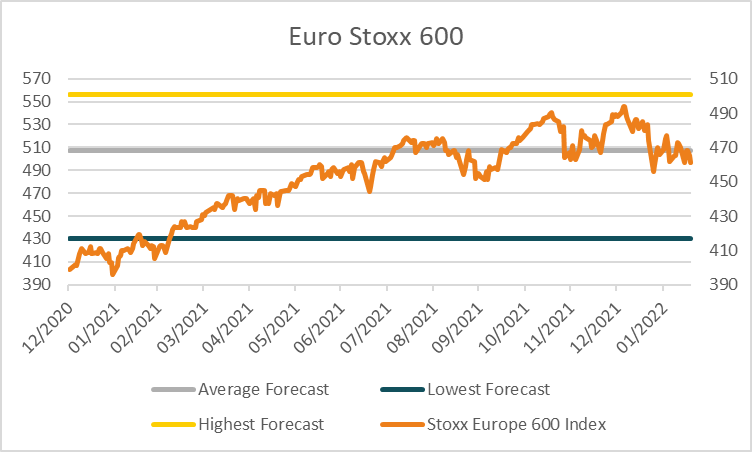

European equities also finish the week lower with the Euro Stoxx 600 declining -0.81% taking a weekly decline to -1.87%. The DAX also declined -1.47% on Friday, as did the CAC -0.25% and FTSE100 -0.32% with major benchmarks lower across the region. In economic data, the flash reading of Eurozone consumer confidence for February declined to -8.5 missing estimates of a slight increase to -8 from -8.5 previously. A monthly report by Bloomberg on Friday showed equity strategists expect European stocks to gain more than +8% by the end of the year, even as monetary policy begins to tighten amid higher inflation.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

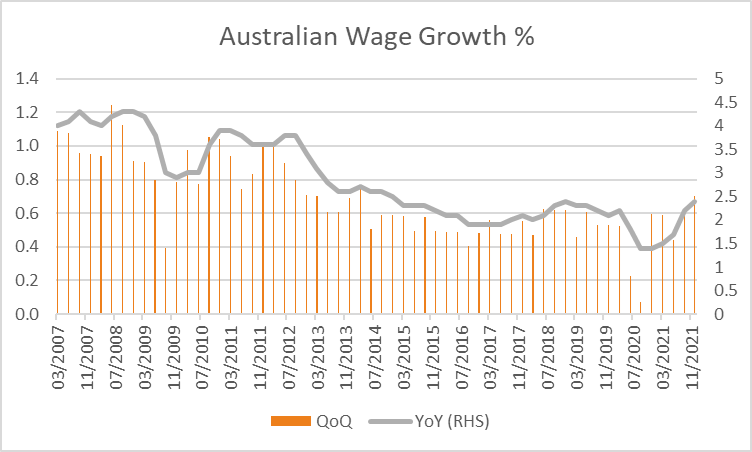

The ASX looks set to open lower with ASX200 futures down -51 points or -0.71% from Friday at 7,094. The benchmark index declined –1.02% on Friday to finish little changed for the week with health care -3.07% and financials -0.93% weighing on Friday with all sectors negative and only 29% of stocks higher. In economic data for this week, Monday will see the release of flash PMI data for both manufacturing and services for February, followed by the wage price index for the year to December 31st 2021 expected to show a rise of +2.4% from +2.2% previously. Gains are seen as adding weight to a higher path of interest rates in Australia and has been a key focus by the RBA suggesting wage growth needs to pick up for inflation to be sustained within its target range of 2-3%. The Australian dollar finished -0.14% weaker on Friday at 0.7177 while the 10-year yield on government bonds rose +4 basis points to 2.248%.

Oil prices were mixed on Friday as investors weigh ongoing Iranian nuclear talks as well as tensions over Ukraine. WTI crude traded -0.75% lower at US$91.07 while Brent crude rose +0.61% to US$93.54 a barrel. Base metals were higher for the week with aluminium rising +4.02%, as did copper +0.97%, lead +3.05%, nickel +4.74% and tin +1.36% while zinc declined -1.41%. Iron ore futures in Singapore finished the week -5.92% over concerns of further action by Chinese officials to stabilise the market. Gold was unchanged at US$1,898 on Friday with silver rising +0.37% to US$23.92 while Bitcoin declined -1.74% on Friday and is down a further -4.17% over the weekend to US$38,323.

Economic data:

- Australian PMI (MoM Feb) 09:00

- German PMI (MoM Feb) 19:30

- Eurozone PMI (MoM Feb) 20:00

- Fed Bowman Speech 03:15

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.