U.S. equities pared declines on Wednesday following higher than forecast retail sales figures for January, while shorter-dated Treasury yields declined following the release of the Federal Reserve policy minutes.

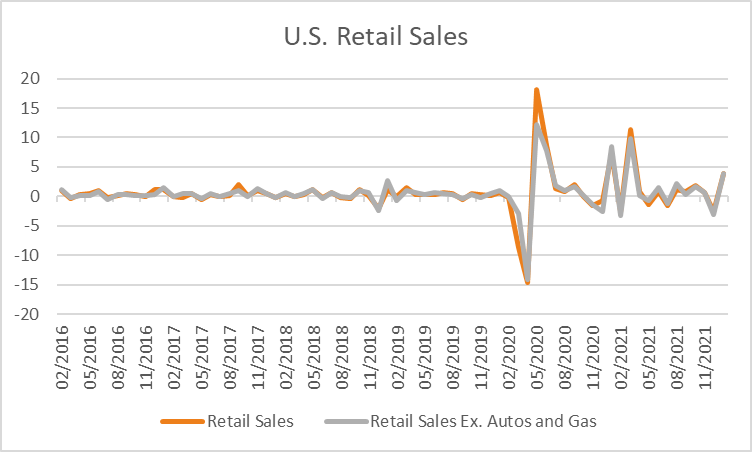

Retail sales in January rose by the most in 10-months, rising +3.8% versus +2.0% forecast by analysts and up from a revised lower +2.5% in December. A measure that excludes both gas and autos also rose +3.8% for the month from a revised -3.2% in December. Expectations are for spending to revert to more normal lower levels with disposable income back to its pre-recession trend with most pandemic-era stimulus payments having ended. Elsewhere, industrial production rose +1.4% in January against estimates of a +0.4% gain, and business inventories for December rose +2.1% from +1.5% as expected. The S&P500 pared modest declines to trade +0.19% higher as of 07:27 am AEDT lifted by industrials +0.65% and consumer discretionary +0.40%. The Dow Jones edged -0.06% lower, while the Nasdaq Composite was +0.5% higher with the Russell 2000 rising +0.33% and the VIX declining -6.13% to 24.11.

The minutes from the latest Federal Reserve meeting were seen as slightly more dovish than expected with no talk of a 50-basis point rate hike and offering little besides the hawkish pivot already seen from the meeting statement and press conference. The minutes reaffirmed that inflation was running too high, warranting an increase in rates soon and potentially justifying a faster pace of tightening. The yield on 2-year Treasuries declined -5.5 basis points to 1.525%, with the 10-year edging -0.3 basis points lower while the 30-year was little changed at 2.358%.

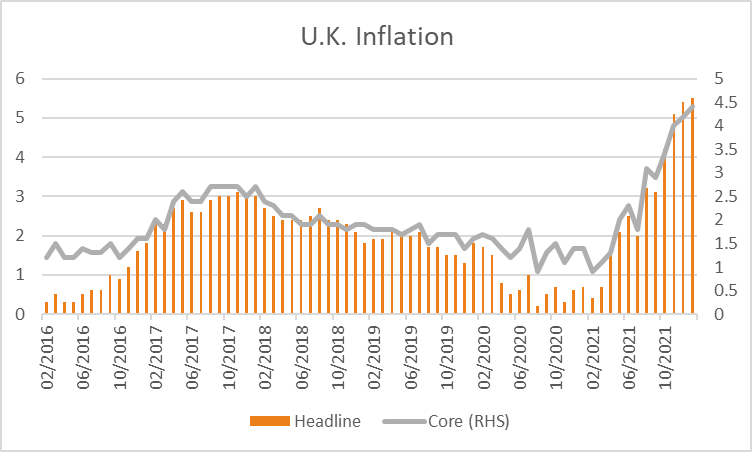

European equities were mixed following higher than expected inflation in the U.K. with the Euro Stoxx 600 edging +0.04% higher as energy +1.76% and materials +0.76% offset a -0.58% decline in financials. The DAX weakened -0.28%, as did the CAC -0.21% and FTSE100 -0.07% with Spain’s IBEX rising +0.22%. U.K. core inflation rose +4.4% for the year to January, modestly higher than estimates of +4.3% while headline inflation rose +5.5% also modestly higher than estimates to remain unchanged at +5.4% with inflation reaching a 30-year high. The gains in inflation spurred further bets of a 50-basis point rate hike by the Bank of England when it meets next month. Elsewhere, Eurozone industrial production for the year to December rose +1.6% versus estimates of a -0.5% decline. 10-year bond yields were lower across the region, ranging from -5.9 basis points in Sweden to -2.9 in France.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX looks set for a flat open this morning with futures up just +6 points or +0.08% to 7,209. The index gained +1.08% on Wednesday in broad-based buying with 84% of stocks higher lifted by health care +6.22% and real estate +3.09%. CSL rose +8.5% after upgrading guidance and reporting better than expected sales. Treasury Wine Estates also gained +11.7% after its first half results showed it was executing moving earnings away from China in a push to reinvigorate growth after a difficult two years following tariffs imposed by China. Elsewhere Liontown Resources climbed +18% after reporting a deal with Tesla Inc. to supply more than 100,000 tonnes of lithium spodumene concentrate annually over the next five years. The Australian dollar is +0.70% higher at 0.7202 ahead of this mornings employment data for January which is expected to show no jobs were added in the month and the unemployment rate to remain stable at +4.2%.

Oil prices made a modest rebound following Tuesday’s declines amid easing geopolitical tensions with both WTI and Brent crude up +0.70% and +0.60% at US$92.76 and US$93.91 a barrel. Iron ore futures in Singapore gained +3.18% on Wednesday following Tuesday’s slump although have given back most of those gains this morning trading -2.95% lower at US$136.10 amid Chinese officials taking steps to ensure a more stable iron ore market. Gold rose +0.95% to US$1,871 with silver rising +1.11% to US$23.62 and Bitcoin gained +0.74% to US$44,322.

Economic data:

- Australian Employment (MoM Jan) 11:30

- ECB Economic Bulletin 20:00

- U.S. Initial Jobless Claims (Feb 12th) 00:30

- Fed Bullard Speech 03:00

- Fed Mester Speech 09:00

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.