US equities extended gains on Wednesday, as weaker UK inflation data added to easing concerns of inflationary and aggressive central banks.

United States

The S&P 500 rose 0.24% along with the Dow Jones 0.31%, Nasdaq Composite 0.03%, and Russell 2000 0.45% while the VIX was 3.46% higher at 13.76. Meanwhile, US equity futures are lower after the close following earnings from Tesla and Netflix which disappointed. As of 8:25 AEDT, S&P500 e-mini futures are down -0.16% with Nasdaq 100 futures -0.43% weaker.

Tesla’s second-quarter earnings beat analyst estimates, however, the stock was -3.6% lower in after-hours trading as shrinking margins weighed on sentiment, declining to 18.2% from 25% a year earlier. Netflix’s share price declined as much as -6% in after-hours as revenue figures fell short of expectations. In terms of guidance, third-quarter revenue is now expected at US$8.52 billion, below estimates of analysts at US$8.67 billion. Carvana’s stock price rallied during a six-minute frenzy on Wall Street akin to previous meme stock hype, after announcing a debt restructuring plan to end concerns of the company’s liquidity. The stock price rocketed more than 40% to land at $55.80, from $39.80 a day earlier.

Europe

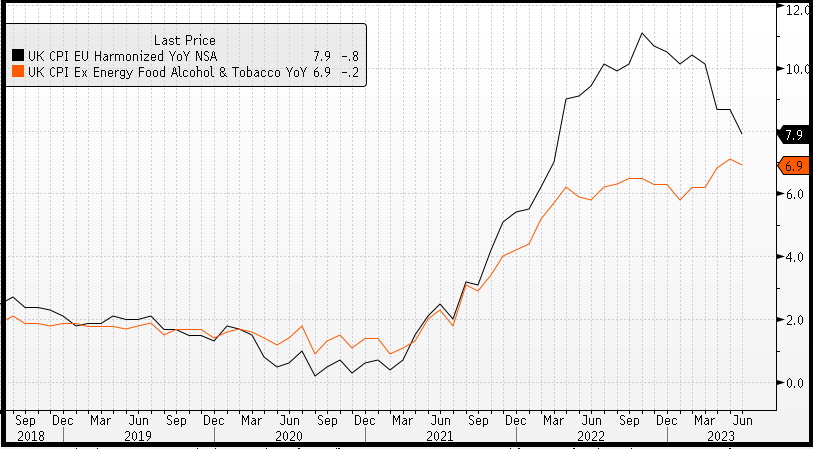

European equities rose after UK inflation rose less than forecast after an extended period of upside surprises. Over the 12 months, headline prices rose 7.9% below estimates of 8.2% with core inflation up 6.9% also below estimates of 7.1%. The Euro Stoxx 600 gained 0.26% along with the CAC 0.11 and FTSE100 1.80% which benefited from a -0.74% fall in the Pound given FTSE100 companies have significant exposure to overseas earnings, while the domestically focused FTSE 250 jumped 3.78%. Traders pared bets on peak Bank of England rates now sitting at 5.8% down from 6% before the data.

UK Inflation (YoY %)

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

Australia

The ASX is expected to open flat this morning with ASX200 futures up just 2 points or 0.03% to 7,286. The index rose 0.55% on Wednesday, with a 1.49% gain in financials more than offsetting a -0.56% fall in materials with most sectors positive for the session, led by energy which rose 1.7% following higher oil prices.

In focus today is the release of the latest employment data for June, expected to show 15k jobs were added over the month and the unemployment rate remaining stable at 3.6%. The data will be one of the final pieces of key information ahead of the RBA rate decision on August 1st, with official Q2 inflation data released next week.

Commodities

Oil prices dropped despite inventory reports showing US stockpiles declined by 708k barrels against expectations of a 2.4 million barrel draw. WTI and Brent crude down -0.53% and -0.09% to $75.35 and $79.56 respectively. In precious metals, spot gold declined by -0.11% to $1,976, while spot silver advanced 0.36% to $25.14. In industrial metals, copper fell -0.43% to $380 and SGX Iron Ore fell -1.14% to $110.34. The price of bitcoin advanced 0.5% to $30,088.

Economic Calendar

20th July 2023

Australian Unemployment Rate (MoM Jun) 11:30

US Jobless Claims (15th July) 22:30

US Philadelphia Fed Manufacturing Index (MoM Jul) 22:30

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.