U.S. equities rose with Treasury yields and the U.S. dollar on Friday after a stronger than anticipated non-farm payrolls report for January.

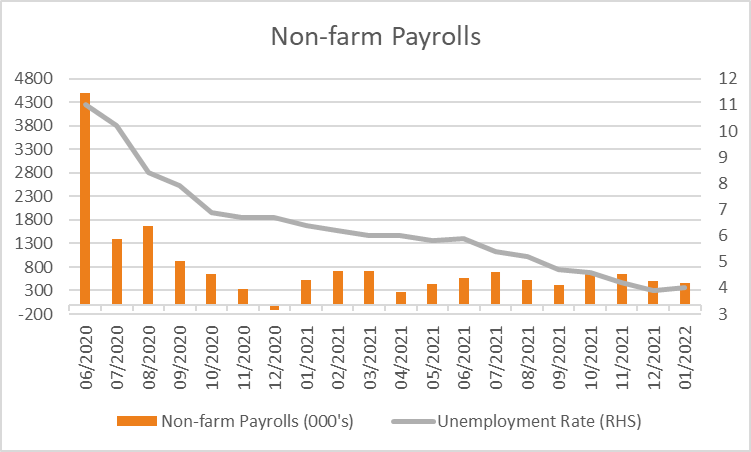

The non-farm payrolls report for January showed +467k jobs were added over the month, higher than the +150k expected with the two prior readings also revised higher. The unemployment rate increased slightly from +3.9% to +4.0% as the participation rate rose from 61.9% to 62.2% as more people look to return to the workforce. Average hourly earnings rose +0.7% for the month, higher than the estimated +0.5% rising +5.7% over the year vs +5.2% expected. Overall, this was a strong job report that places further pressure on the Federal Reserve tightening policy, with more analysts and economists calling for a 50-basis point rate hike in March although this has so far been downplayed by officials.

The S&P500 rose +0.52% boosted by a +3.74% gain in consumer discretionary relating to a +13.54% gain in Amazon.com Inc shares which surged following better than expected earnings reported on Thursday after the close of trading. The Nasdaq Composite also gained +1.58% while the Dow Jones edged -0.06% lower, the Russell 2000 gained +0.57% and the VIX weakened -4.64% to 23.22. Treasury yields jumped across the curve following the jobs report with the 2-year yield rising +11.6 basis points to 1.313%, the 10-year rose +7.9 basis points as did the 30-year up +5.9 basis points. The 1-year breakeven inflation rate jumped +10.4 basis points to 3.736% while longer measures were little changed, lifting real yields higher and strengthening the U.S. dollar +0.11% to 95.48.

European equities retreated on Friday with a drop wiping out a weekly gain as growing expectations of rate hikes and more hawkish rhetoric from central banks weighed on sentiment. The Euro Stoxx 600 fell -1.38% on Friday with 82% of stocks trading lower and all sectors but energy +2.81% negative for the session. The DAX also declined -1.75%, as did the CAC -0.77% and FTSE100 -0.17% with major European benchmarks lower. In economic data, Eurozone retail sales for the year to December were lower than expected, rising +2% vs estimates for a +5.1% gain, while the November reading was revised higher to +8.2%.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX looks set for a weaker open this morning with ASX200 futures down -41 points or -0.58% at 6,993 from Friday. The index rose +0.60% on Friday pushing gains for the week to +1.89% with Westpac leading market gains rising +4.3% after reporting higher than expected earnings for the December quarter. Continued strength in oil prices supported energy shares with WPL rising +5.8%, as did STO +6%, ORG +6.7% and BPT +4.9%. The Australian dollar weakened -0.97% on Friday to 0.7072 while the yield on 10-year government bonds rose +9.3 basis points to 1.96%. Ahead for the week retail sales for December are released at 11:30 am AEDT this morning, followed by the Westpac consumer confidence index for February on Wednesday and a speech by RBA Governor Lowe on Friday.

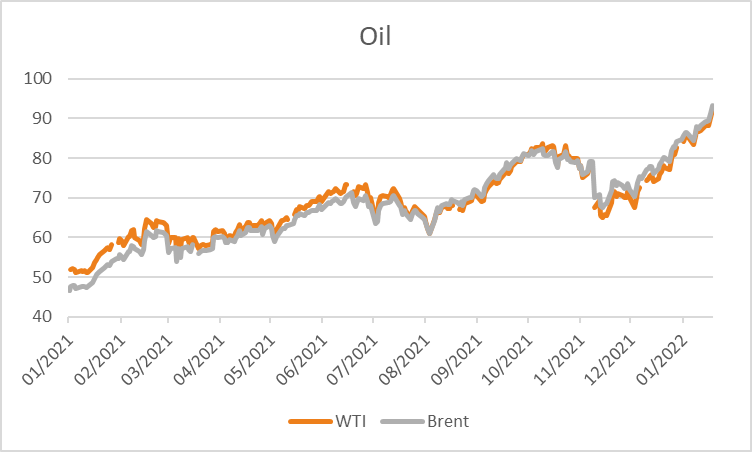

Oil prices rose on Friday as expectations of higher demand, declining spare capacity and the inability to meet production increases so far by OPEC+ support prices. Both WTI and Brent crude rose +2.26% and +2.37% on Friday to US$92.31 and US$93.27 a barrel. Base metals were mixed for the week with copper gaining +3.51%, as did nickel +2.95%, aluminium +2.15% and tin +3.21% while lead declined -3.42%. Iron ore futures in Singapore rose +0.46% on Friday and are little changed this morning at US$144.95. Gold rose +0.19% on Friday to US$1,808 despite the rise in real yields and the U.S. dollar, silver also gained +0.42% to US$22.52 and Bitcoin surged +9.96% and is a further +2.52% higher over the weekend at US$41,740.

Economic data:

- Australian Retail Sales (MoM Dec) 11:30

- Chinese Composite PMI (MoM Jan) 12:45

- ECB President Lagarde Speech 02:45

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.