U.S. equities declined on Wednesday and Treasury yields rose after geopolitical tensions continued to weigh on sentiment with President Biden expanding sanctions against Russia.

President Biden expanded sanctions on Wednesday against the builder of the Nord Stream 2 gas pipeline from Russia to Germany, as well as its corporate leadership. Elsewhere, reports of cyberattacks on several Ukrainian government and bank websites also weighed on sentiment. As of 07:29 am AEDT the S&P500 was -1.62% lower in broad-based selling with 83% of stocks trading lower, led by declines in technology -2.04%, consumer discretionary -2.86% and financials -1.47% while energy outperformed +1.05% despite oil prices edging lower. The Dow Jones also weakened -1.08%, as did the Nasdaq Composite -2.03% and Russell 2000 -1.34% with the VIX rising +6.18% to 30.59 bringing the VIX curve into backwardation. Typically, when the VIX curve moves to backwardation (reading above 1) it signals a heightened level of short-term fear in the markets, and while by no means a perfect indicator, when this reverses back in contango (reading below 1) has coincided with key lows.

Inflation remains a key concern for investors, with the Ukrainian situation expected to worsen the outlook given recent increases in both oil and natural gas prices. Treasury yields rose across the curve on Wednesday, with the 2-year yield up +2 basis points to 1.596%, as were both the 10 and 30-year yields up +3.5 and +3.1 basis points respectively to 1.972% and 2.267%. Breakeven inflation rates rose across the curve, with the 1-year rate rising +13.8 basis points to 4.898% as did both the 5 and 10-year rates, up +10.9 and +7.1 basis points respectively. Based on futures pricing, the market continues to expect six interest rate hikes by the Federal Reserve in 2022 beginning in March. In focus overnight will be the second estimate of U.S. GDP for Q4 2021 expected to show the economy expanded at a +7% annualised rate.

European equities were generally lower weighed by the situation in Ukraine and rising energy prices seen as worsening the inflation outlook, adding further weight to the case for the ECB to raise rates despite a less-forgiving economic and geopolitical backdrop. Data on Wednesday showed inflation was in line with estimates, as core prices rose +2.3% as forecast down from +2.6% previously year-on-year to January, while headline prices rose +5.1% as forecast from +5.0% previously. Elsewhere, German consumer confidence declined more than expected for March to -8.1 from -6.7 missing estimates of a slight improvement to -6.3. The Euro Stoxx 600 declined -0.28% weighed by declines in industrials -0.71% and financials -0.55% with 61% of stocks lower. The DAX also declined -0.42%, as did the CAC -0.10% while the FTSE100 edged +0.05% higher thanks to gains in Barclays of +3.1% after annual profit nearly tripled while bad loans declined, and its investment bank continued to perform strongly.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

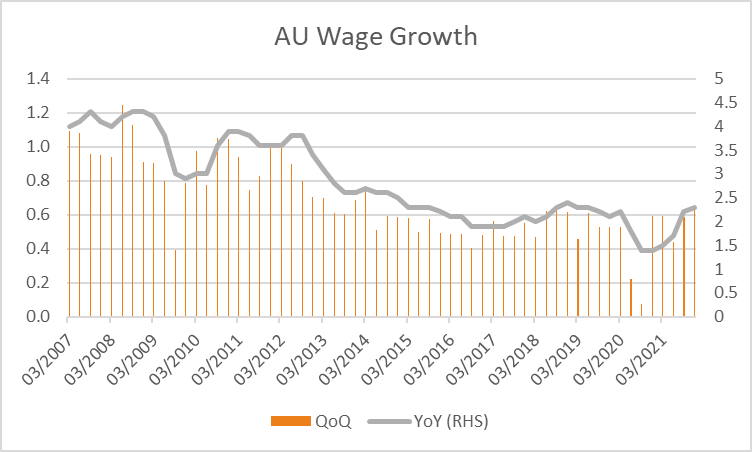

The ASX looks set for a weaker open this morning with ASX200 futures down -91 points or -1.26% to 7,028. The index gained +0.62% on Wednesday with 70% of stocks rising and materials +0.68%, health care +1.19% and financials +0.34% the largest contributors to gain. Shares in WiseTech Global climbed +4.2% after the company upgraded guidance expecting full-year earnings to increase as much as +43% compared to +38% previously. Pilbara Minerals gained +2.2% after reporting soaring profits with net profit for the six months to December rising to $114m from -$21.2m previously. Meanwhile, Domino’s Pizza slumped -14% after warning of slowing revenue growth and challenges from rising prices. In economic data, wage growth for the final quarter of 2021 rose +2.3% from a year earlier from +2.2% previously, slightly below estimates of 2.4% while rising +0.7% over the quarter as forecast from +0.6% previously. The RBA has maintained the view it needs to see wage growth around 3% to sustain inflation within its 2-3% target. The Australian dollar is trading +0.19% higher this morning at 0.7233 and the yield on 10-year government bonds rose +7 basis points to 2.270% on Wednesday.

Oil prices declined on Wednesday with both WTI and Brent crude -0.37% and -0.48% lower at US$91.59 and US$96.40 a barrel. Iron ore futures in Singapore rose +1.79% on Wednesday although are trading -0.22% lower at US$138.80 this morning. Gold rose +0.41% to US$1,906 over geopolitical tensions as well as a decline in real yields, silver rose +1.62% to US$24.51 while Bitcoin weakened -0.91% to US$37,574.

Economic data:

- U.S. GDP (QoQ Q4) 00:30

- U.S. Initial Jobless Claims (19th Feb) 00:30

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.