U.S. equities declined with Treasury yields on Friday as concerns over a potential conflict in the Ukraine weighed on risk sentiment.

On Friday the U.S. warned that a potential invasion of Ukraine could occur as soon as the next week with both the U.K. and the U.S. advising citizens to leave Ukraine as tensions rise, while Russia has repeatedly denied that it plans to invade. The S&P500 finished -1.90% lower on Friday, dragging the benchmark -1.82% down for the week. Energy outperformed +2.79% as oil prices spiked on concerns over a potential conflict, while technology -3.01% and consumer discretionary -2.82% weighed, with 80% of stocks trading lower. The Dow Jones also declined -1.43%, as did the Nasdaq Composite -2.78% and Russell 2000 -1.02% with the VIX spiking +14.43% to 27.36 having risen +37% over the prior two sessions.

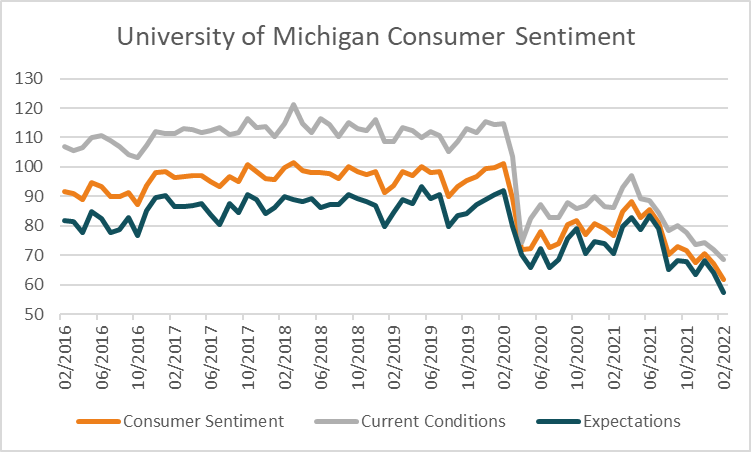

Investors sought the safety of Treasuries which partially reversed the sizeable jump in yields from Thursday following higher than forecast inflation data. The 2-year yield declined -7.7 basis points to 1.505%, as did the 10-year yield -9.1 to 1.941% and 30-year year -7.8 basis points to 2.241% while the U.S. dollar index benefited from its status as a haven, rising +0.55% to 96.08. In economic data, the University of Michigan consumer sentiment survey for February declined to 61.7 from 67.2, missing estimates of a small rise to 67.5 and reaching the lowest level since 2011. The main concern for consumers is rising inflation resulting in a drop in real incomes with nearly two-thirds of consumers anticipating bad financial conditions ahead.

European equities were also broadly lower on Friday with the Euro Stoxx 600 down -0.59% weighed by health care -1.59% and industrials -1.22% while energy +1.23% outperformed with 71% of stocks lower for the session. The DAX also declined -0.42%, as did the CAC -1.27% and FTSE100 -0.15% with all major benchmarks across the region lower. Still, European benchmarks posted their first weekly gain of the year with the Euro Stoxx 600 up +1.6%. In economic data, German inflation rose +4.9% for the year to January as forecast, easing from +5.3% in December. U.K. GDP for the year to the fourth quarter of 2021 was in line with estimates of +6.4% with a reading of +6.5% from a revised higher +7% previously. The Euro weakened -0.68% to 1.1350 while the Pound edged +0.05% higher to 1.3564.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX looks set for a weaker start this morning with futures down -33 points or -0.46% to 7,075. The index declined -0.98% on Friday paring a weekly advance to +1.36% with materials +0.33% the only positive sector on Friday as health care -2.07% and real estate -2.61% weighed in broad selling with 89% of stocks lower. Ahead for the week investors will focus on the release of RBA minutes on Tuesday at 11:30 AEDT, followed by the Westpac leading index on Wednesday and unemployment data for January on Thursday. Estimates are for employment to declined -15k and the unemployment rate to remain stable at +4.2% although the Omicron variant is expected to still cloud the numbers while the recent strength in the labour market is expected to remain intact. The Australian dollar weakened -0.42% on Friday to 0.7137 and the 10-year government bond yield rose +10.5 basis points to 2.21%.

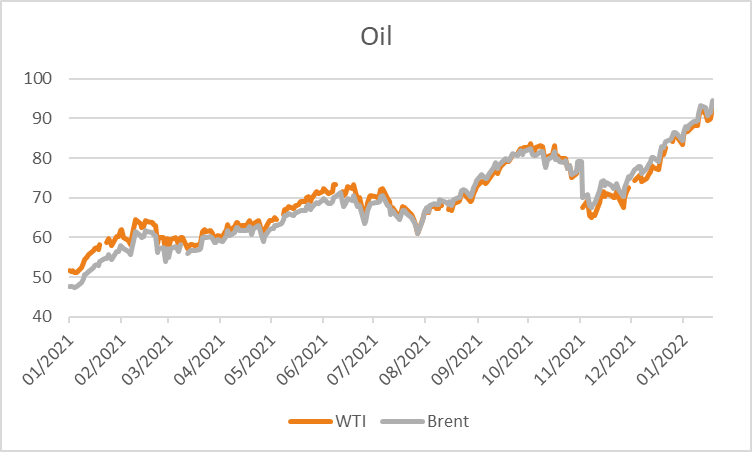

Oil prices spiked on Friday over the potential escalation of tensions in Ukraine with both WTI and Brent crude rising +3.58% and +3.31% respectively to US$93.10 and US$94.44 a barrel. Base metals were higher for the week with aluminium rising +2.03%, as did copper +0.41%, lead +4.18%, nickel +0.26%, tin +1.23% and zinc +0.39%. Iron ore futures declined -2.15% on Friday and are a further -2.10% weaker this morning at US$146.65. Gold rose +1.75% to US$1,858 benefiting from its haven status as well as a hedge against inflation, silver also rose +1.66% to US$23.58 while Bitcoin declined -2.77% to US42,563.

Economic data:

- ECB President Lagarde Speech 03:15

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.