Stocks declined on Monday as investors await key U.S. inflation data on Wednesday as well as the start of Q2 earnings, while rising COVID cases in China also weighed on sentiment.

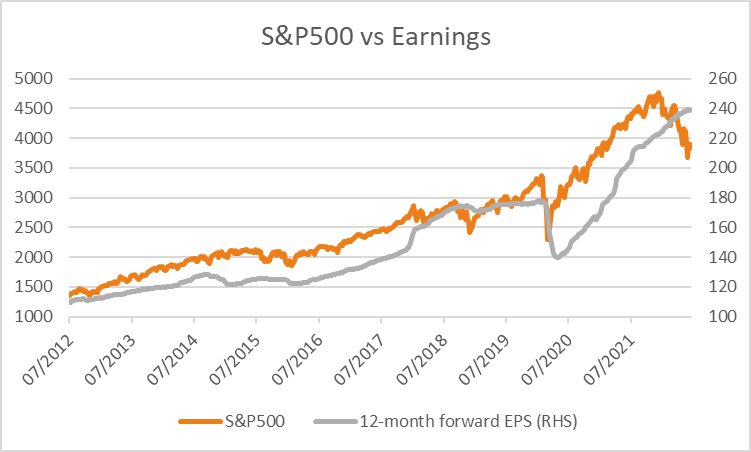

The S&P500 declined -1.15% weighed by technology -1.42% and consumer discretionary -2.76% while utilities outperformed +0.64% in weak breadth with 73% of stocks trading lower. The Dow Jones also weakened -0.52% along with the Nasdaq Composite -2.26% and Russell 2000 -2.11% with the VIX rising +6.21% to 26.17. Shares in Twitter slumped -10.02% after Elon Musk walked away from his $44 billion deal to buy the company, setting up a legal battle. Thursday will also see the Q2 earnings season begin in earnest with Morgan Stanley, JP Morgan, Wells Fargo, State Street, Citigroup, and Blackrock all due to report this week. Despite growing concerns of a recession, inflation and a strong USD analysts continue to bet company earnings are resilient enough on higher costs to consumers with forward EPS estimates on the S&P500 remaining near record highs, in part buoyed by expectations of strong earnings from energy stocks.

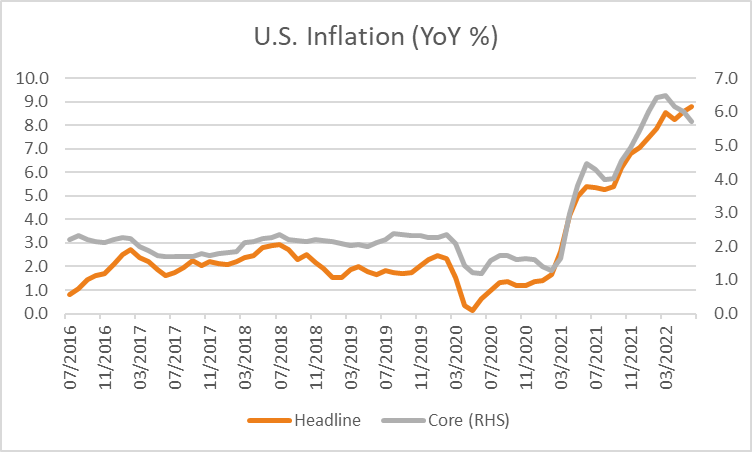

Also in focus this week is U.S. inflation data year-on-year for June released on Wednesday forecast to show headline inflation rose +8.8% from +8.6% previously while core prices are expected to moderate to +5.7% from +6%. Treasury yields were lower overnight with the 2-year yield down -3.3 basis points to 3.072% along with the 10 and 30-year rates by -8.4 and -6.7 basis points respectively while the U.S. dollar index strengthened +1.12% to 108.20.

European equities were also lower, weighed by rising COVID cases in China prompting concerns of tighter restrictions that would lead for further supply chain disruptions. Meanwhile, the Nord Stream 1 pipeline carrying gas from Russia to Germany has begun 10 days of annual maintenance, although there are concerns the shutdown may be extended due to the war in Ukraine worsening the energy crisis and inflation in Europe. The Euro Stoxx declined -0.50% on Monday along with the DAX -1.40%, CAC -0.61% while the FTSE100 was unchanged. Concerns around inflation and slowing economic growth continue to see the Euro weaken, which is now within touching distance of parity, down -1.40% overnight to 1.0042 its lowest level since 2002.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

Despite the weak lead from overseas markets, the ASX200 is expected to rise +20 points or +0.31% this morning with ASX200 futures trading at 6,523. The index weakened -1.14% on Monday weighed by materials -2.78% and financials -0.47% while health care +0.12% was the only positive sector. Shares in EML Payments slumped -24.6% after CEO Tom Cregan exited the company “effective immediately” in an unexplained departure. Shares in Lind Administration rose +0.3% to $4.03 after rejecting Dye & Durham’s improved $4.57 offer, with the company board “unable to recommend “ the revised offer after stakeholder feedback and will look at alternative options should the deal fall over. The Australian dollar slumped -1.81% overnight to 0.6733 weighed by risk off sentiment as well as weaker commodity prices on news of rising COVID cases in Shanghai.

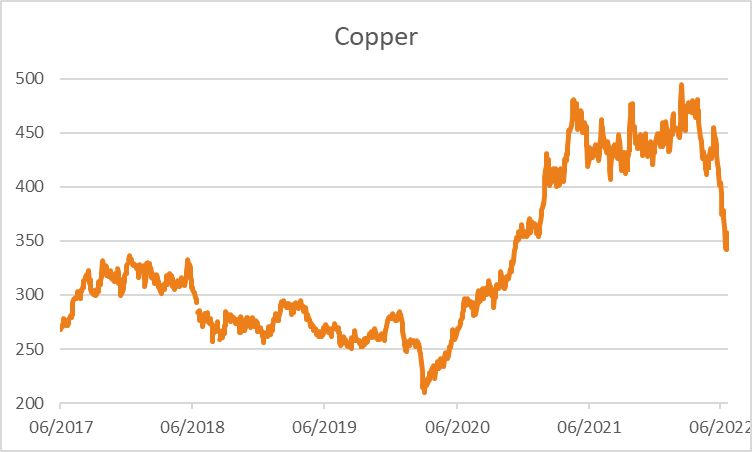

Both WTI and Brent crude were -1.40% and -0.70% weaker overnight at US$103.32 and US$106.27 a barrel. Iron ore futures in Singapore weakened -2.56% on Monday and are trading a further -2.47% lower this morning at US$107.30. Copper futures in the U.S. fell -2.89% over concerns of further restrictions in China to combat rising COVID cases with the metal slumping as much as -30% since early March on concerns of a slowdown in economic growth. Gold weakened -0.49% to US$1,733.996 an oz on Monday along with silver -1.0% to US$19.12 with Bitcoin also -2.67% lower at US$20,409.

Economic data:

- Eurozone ZEW Economic Sentiment (MoM Jul) 19:00

- German ZEW Economic Sentiment (MoM Jul) 19:00

- Fed Barkin Speech 02:30

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.