Global equities declined on Tuesday as rising energy prices stoked inflation concerns, while investors continued to seek the safety of government bonds, driving yields lower.

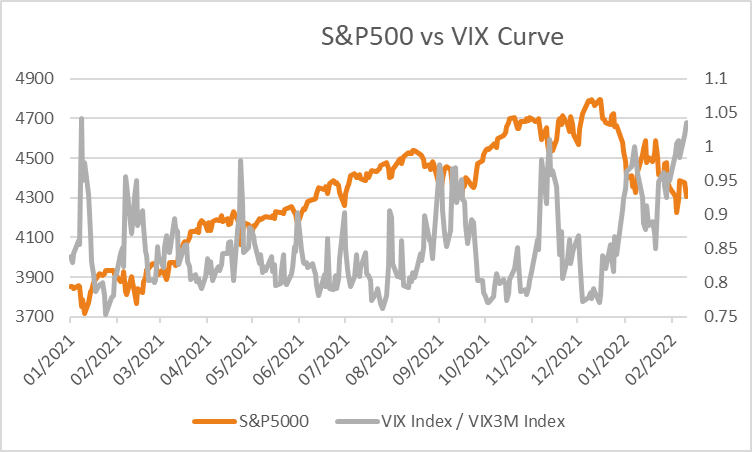

As of 07:36 am AEDT the S&P500 was -1.46% lower, with 77% of stocks lower with technology -1.98% and financials -3.50% weighing while energy +0.87% was the only positive sector. The Dow Jones also declined -1.78%, as did the Nasdaq Composite +1.70% and Russell 2000 -1.69%. The VIX climbed +12.6% with the VIX curve once again in backwardation, signaling short term fear is elevated versus the intermediate-term. Fed Chair Powell is due to give semi-annual testimony before lawmakers overnight as he tries to reassure lawmakers the central bank will act to curb inflation while remaining flexible in the face of geopolitical uncertainty.

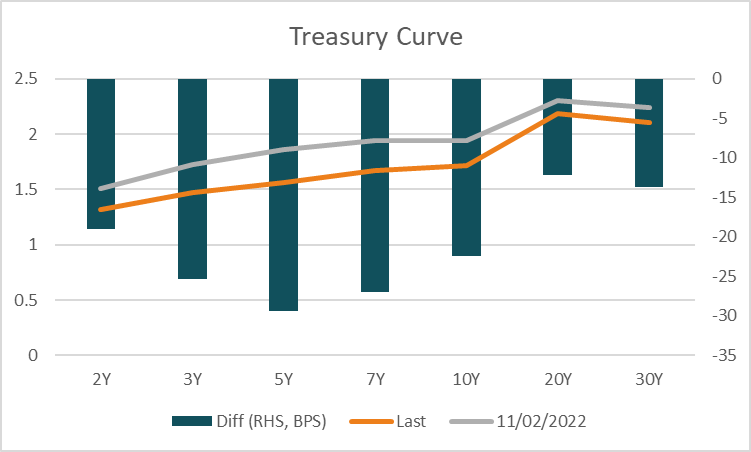

In economic data, the U.S. ISM manufacturing survey for February rose to 58.6 from 57.6 previously, beating estimates of a rise to 58. Commentary as part of the survey was positive, pointing to strong demand and higher prices, with the main constraints continuing to be transportation services and raw materials. Investors continued to seek the safety of U.S. Treasuries with yields declining across the curve while Fed Fund futures are now pricing +4.6 rate hikes by the end of 2022, down from over 6 in mid-February. The 2-year yield declined -11.9 basis points to 1.313%, as did both the 10 and 30-year yields down -10.9 and -5.8 basis points respectively. Breakeven inflation rates continued to rise, pushing real yields lower across 5 and 10-years by -23.6 and -13.5 basis points respectively. Despite lower real yields, the U.S. dollar rose +0.70% to 97.39 benefiting from its status as a haven.

European equities weakened with the conflict in Ukraine continuing to weigh on sentiment. The Euro Stoxx 600 declined -2.37% as did the DAX -3.85%, CAC -3.94%, and FTSE100 -1.72% with major benchmarks across Europe broadly lower. Weighing on sentiment was agreement by the European Union to exclude seven Russian banks from the SWIFT financial messaging system, although spared the largest lender Sberbank. 10-year government bond yields across the region plunged ranging from -30.5 basis points in Italy to -15.5 in Sweden weighing on both the Euro and Pound which declined -0.81% to 1.1128 and -0.73% to 1.3322 respectively. Eurozone manufacturing PMI for February was slightly below estimates at 58.2 versus 58.4 predicted, down from 58.7 previously. The headline decline in manufacturing PMI was seen as masking the underlying strength of a largely positive month with demand for goods trending higher expanding at a six-month high with underlying sales conditions strengthening. The report also noted stabilization across supply chains which will help increase production capacities and cool inflation which the report showed remained elevated.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

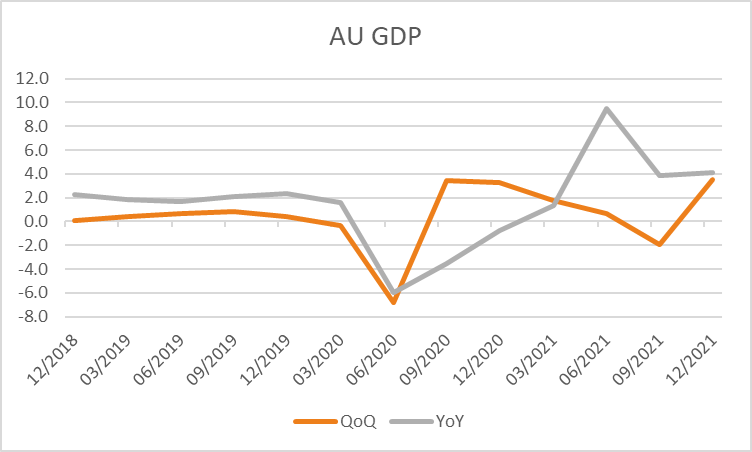

The ASX is set to open lower this morning with ASX200 futures down -65 points or -0.92% to 6,981. The index rose +0.67% on Tuesday, paring initial gains of as much as +1.4% with financials +1.02% and technology +5.66% the largest contributor to the index’s gains. At the conclusion of its monetary policy meeting, the RBA signalled it doesn’t intend to rush to raise interest rates in contrast to market pricing. “Wages growth remains modest, and it is likely to be some time yet before growth in labour costs is at a rate consistent with inflation being sustainably at target,” Lowe noted on Tuesday while adding the war in Ukraine is a “major new source of uncertainty” adding complications to the inflation outlook. The Australian dollar weakened -0.23% to 0.7246 on Tuesday and the yield on 10-year government bonds rose +5 basis points to 2.188% although we should expect weakness today given the sharp decline in global yields overnight. Investors will focus on the release of Q4 2021 GDP at 11:30 AEDT this morning, expected to show the economy expanded at +4.1%.

Energy prices jumped overnight with both WTI and Brent crude rising +9.01% and +7.96% to US$104.29 and US$105.77 a barrel despite the U.S. and other major nations agreed to release up to 60 million barrels from strategic oil reserves. Natural gas prices for delivery in the U.K. and Netherlands also rose +21.95% and 23.41% respectively. Iron ore futures in Singapore rose +4.35% on Tuesday and are a further +1.04% higher at US$149.65 this morning. Reduced supply from Russia and Ukraine are seen as supporting prices, as well as improving factory data from China and bets of additional stimulus. Gold climbed +1.63% to US$1,940 driven by sharply lower real yields, silver also gained +3.61% to US$25.33 with Bitcoin rising +5.49% to US$43,941.

Economic data:

- Australian GDP (YoY Q4) 11:30

- German Unemployment (MoM Feb) 19:55

- Eurozone Inflation (MoM Feb) 21:00

- U.S. ADP Employment Change (MoM Feb) 00:15

- Fed Bullard Speech 01:30

- Fed Powell Testimony 02:00

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.