U.S. equities declined on Tuesday while Treasury yields declined as investors positioned ahead of Wednesday’s inflation data and concerns over the outlook for economic growth and rising COVID cases.

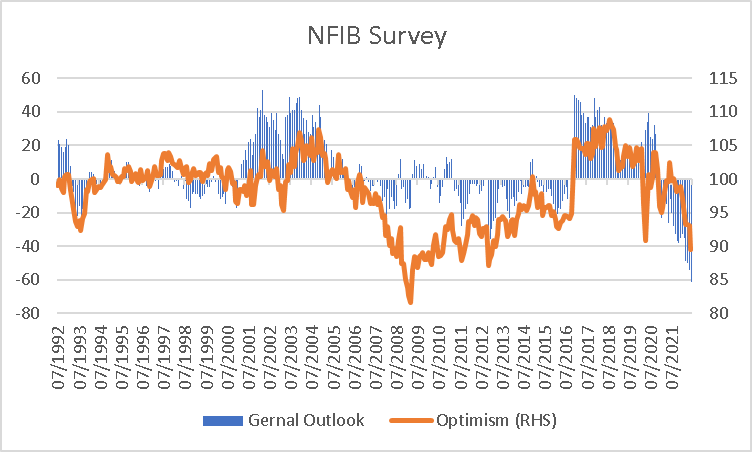

The S&P500 retreated -0.92% with all sectors negative led by energy -2.03% following weaker oil prices and technology -1.34%. The Dow Jones also finished -0.62% lower along with the Nasdaq Composite -0.95% and Russell 2000 -0.22% with the VIX +4.28% higher at 27.29. The National Federal of Independent Businesses said its Small Business Optimism Index declined -3.6 points in June to 89.5, the lowest level since January 2013 with 34% of businesses citing inflation as their biggest problem. The survey also showed 50% of businesses reported jobs openings they could not fill with NFIB Chief Economist William Dunkelberg noting “The persistence of record-high levels of unfilled openings indicates that owners are still seeing opportunities to grow their business, in spite of their negative outlook for the future”.

Treasury yields were lower with the 2-year rate down -2.5 basis points to 3.047% along with the 10 and 30-year yields by -2.2 and -1.8 basis points respectively. Key spreads across the yield curve remained inverted, signaling investors expect a recession in the coming months with the U.S. dollar index continuing to benefit from its haven status, rising +0.13% to 108.16. Investors await consumer price inflation data due tonight, with any signs of moderation in headline prices likely to be received positively and would keep hopes of a Fed pause in late 2022 alive.

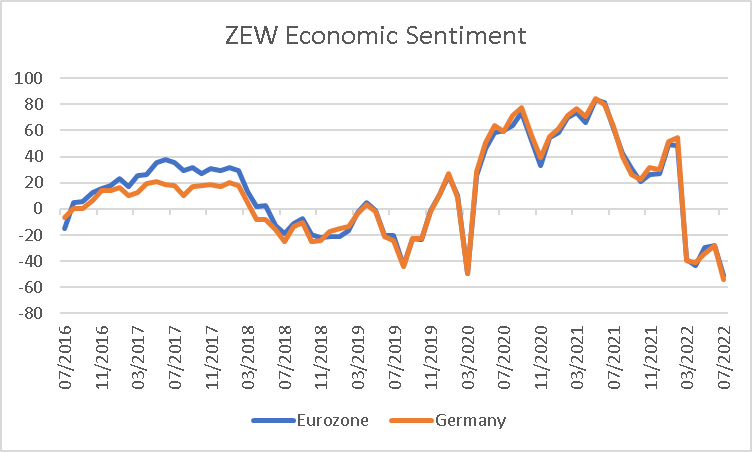

European stocks rose as a drop in oil help alleviate inflation concerns with investors also awaiting the start of earnings season this week. The Euro Stoxx 600 rose +0.49% along with the DAX +0.57%, CAC +0.80% and FTSE100 +0.18%. In economic data, German economic sentiment declined to the lowest levels since 2011 amid an ongoing energy crisis, declining to -53.8 from -28 previously, larger than the forecast –40.5 with Eurozone economic sentiment also declined to -51.1 from -28 in June. 10-year government bond yields were lower across the region, ranging from -13 basis points in Greece to -6.3 in Sweden with the Euro little changed at 1.0037 along with the Pound at 1.1888.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX looks set for a flat open this morning with ASX200 futures down just -2 points or -0.02% to 6,505. The index pared initial gains to edge +0.06% higher on Tuesday with financials +0.68% and health care +1.11% offsetting a decline of -1.17% in materials. Shares in Sezzle slumped -38.6 on Tuesday after merger partner Zip Co said it had mutually agreed to terminate the proposed merger, Zip Co will pay US$11m in compensation costs with its shares rising +6%. E-commerce stocks were also under pressure with sentiment weighed by rising interest rates and declining consumer confidence with furniture retailer TPW down -16.6% along with KGN -10.7%, ABY -8.9% and RBL -2.7%. Separately, data on Tuesday showed the Westpac Consumer Confidence index for July declined to 83.8 from 86.4 previously. The Australian dollar is -0.06% lower overnight at 0.6754 with the 10-year bond yield declining -9.4 basis points to 3.416%.

Oil prices fell overnight on concerns of a recession with both WTI and Brent crude -8.21% and -7.53% lower at US$95.54 and US$99.04 a barrel respectively. Copper futures in the U.S. also declined -5.03% along with iron ore futures over concerns of rising COVID cases in China. Iron ore futures in Singapore declined -4.59% on Tuesday although are +1.03% higher at US$106.05 in early trade this morning. Gold traded -0.46% weaker overnight to US$1,726 an oz with silver -0.96% lower at US$18.94 while Bitcoin declined -4.73% to US$19,443.

Economic data:

- RBNZ Rate Decision 12:00

- German Inflation Final (YoY Jun) 16:00

- U.K. GDP (3-months May) 16:00

- IEA Oil Market Report 18:00

- Eurozone Industrial Production (YoY May) 19:00

- U.S CPI (YoY Jun) 22:30

- Bank of Canada Rate Decision 00:00

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.