U.S. equities rallied on Friday boosted by better-than-expected earnings and economic data, as well as Federal Reserve policymakers talking down the prospect of a +1% rate increase this month.

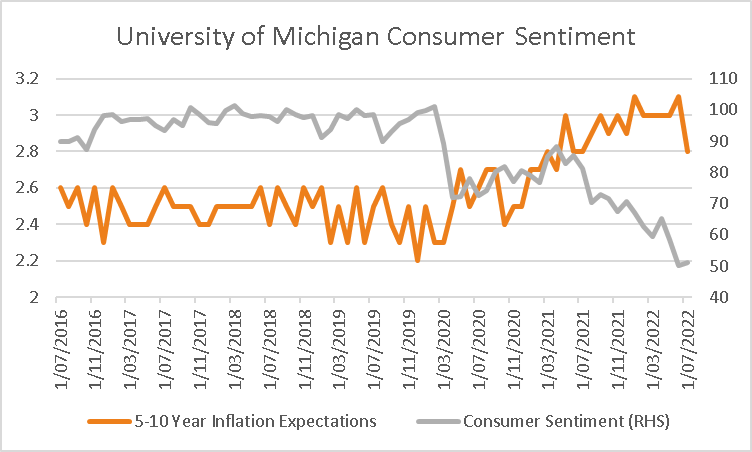

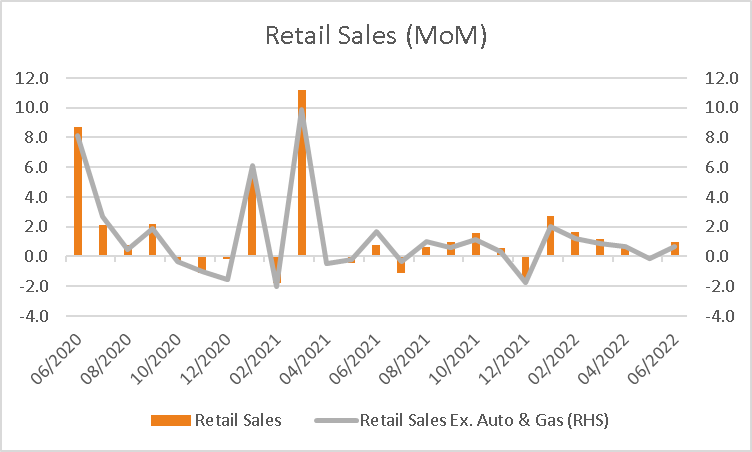

Retail sales for the month of June advanced +1.0% modestly above estimates, with the prior reading in May revised higher to -0.1% from -0.3%. While real sales declined around -1% on an inflation-adjusted basis according to Bloomberg economist estimates, the data suggests there is still enough momentum for the economy to grow over the remainder of the year. Elsewhere the University of Michigan preliminary consumer sentiment survey for July was better than expected at 51.1 compared to expectations to remain unchanged at 50. A decline in long-term consumer inflation expectations over the next five years within the survey caught traders’ attention, declining to a 1-year low at 2.8% down from 3.1% in June and should provide comfort to the Federal Reserve that inflation is not becoming embedded.

Both Atlanta Fed President Raphael Bostic and St. Louis President James Bullard voiced caution about a super-sized 1% increase at this month’s FOMC meeting on the 27th suggesting a +0.75% increase is more probable than a +1% hike. The S&P500 climbed +1.92% boosted by communications +1.33% and technology +1.76% with financials pacing gains rising +3.51% after Citigroup shares climbed +13.2% after it posted a smaller than expected 27% decrease in quarterly profit due to strength within its treasury services business and trading desks amid market volatility. The Dow Jones also rose +2.15% along with the Nasdaq Composite +1.79% and Russell 2000 +2.16% with the VIX retreating -8.22% to 24.23.

European shares were broadly higher, lifted by gains in the U.S. as well as Italy’s President rejecting an offer from Prime Minister Mario Draghi to resign, asking him to address parliament next week in a bid to avert a political crisis that could potentially lead to elections in the coming months. The Euro Stoxx 600 rose +1.79% along with the DAX +2.76%, CAC +2.04% and FTSE100 +1.69%. Ahead for the week investors will be focused on U.K. unemployment on Tuesday along with the final reading of Eurozone inflation for June with U.K. inflation data also out on Wednesday. The ECB will meet on Thursday where the central bank is widely expected to raise interest rates by +0.25% and the week will be rounded off with flash PMI reports for July across the region expected to show a modest slowdown since June.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX looks set to open higher this morning with ASX200 futures finishing +57 points or +0.88% higher on Friday at 6,559. The index declined -0.68% on Friday, paring larger losses of up to -1.7% with materials -3.23% weighing the most heavily on the index. RIO shares declined -2.85% after noting it had suffered an increase in absenteeism over the past fortnight and warned higher interest rates could affect demand. Elsewhere, Pendal the listed investment manager declined -7.84% after reporting worse than expected outflows in the June quarter while shares in WiseTech climbed +3.42% after lifting its annual earnings forecast on stronger top-line growth and improved cost savings. In economic news, Chinese GDP for the 12 months to Q2 was lower than forecast, rising +0.4% compared to estimates of +1.2% and down from +4.8% in Q1. Meanwhile, retail sales in China were better than expected at +3.1% against estimates of +0.3% along with fixed asset investment +6.1% vs +6.0% while industrial production was slightly weaker than expected at +3.9% vs +4%.

Oil prices finished higher on Friday with both WTI and Brent crude up +1.89% and +2.08% respectively at US$97.59 and US$101.16 a barrel. Over the weekend, Saudi ministers insisted that oil policy decisions were based on market logic within the OPEC+ coalition as U.S. President Joe Biden wrapped up a landmark trip to the kingdom where he sought an increase in oil supplies. Metals were lower for the week with aluminium down -3.84% along with copper -7.88%, nickel -10.18%, tin -2.03% and zinc -5.94% while lead rose +1.38%. Iron ore futures in Singapore declined -3.74% on Friday although are trading +1.56% higher this morning at US$98. Coal futures in China were higher by +4.21% along with coking futures +1.01% on signs that an unofficial import ban of Australian coal may be removed in the coming months. Gold edged -0.10% lower on Friday to US$1,708.17 an oz while silver rose +1.56% to US$18.71 with Bitcoin +1.25% which is a further +2% higher over the weekend at US$21,378.

Economic data:

- New Zealand Inflation (QoQ Q2) 08:45

- U.S. NAHB Housing Index (MoM Jul) 00:00

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.