Global equities rose with yields on Wednesday following stronger economic data as well as comments from Fed Chairman Jerome Powell that the economy is expanding enough to withstand rate hikes while pledging to proceed carefully.

Speaking before Congress in semi-annual testimony, Jerome Powell backed a quarter-point rate hike this month to commence a series of increases despite uncertainty caused by Russia’s invasion of Ukraine. Powell acknowledged recent uncertainty surrounding Ukraine but the need to remove pandemic policy support has not changed, “the bottom line is that we will proceed but we will proceed carefully as we learn more about the implications of the Ukraine war for the economy”. On the potential for more than a 25-basis point increase Powell noted, “To the extent that inflation comes in higher or is more persistently high than that, then we would be prepared to move more aggressively by raising the federal funds rate by more than 25 basis points at a meeting or meeting”. Powell will continue the two-day testimony on Thursday.

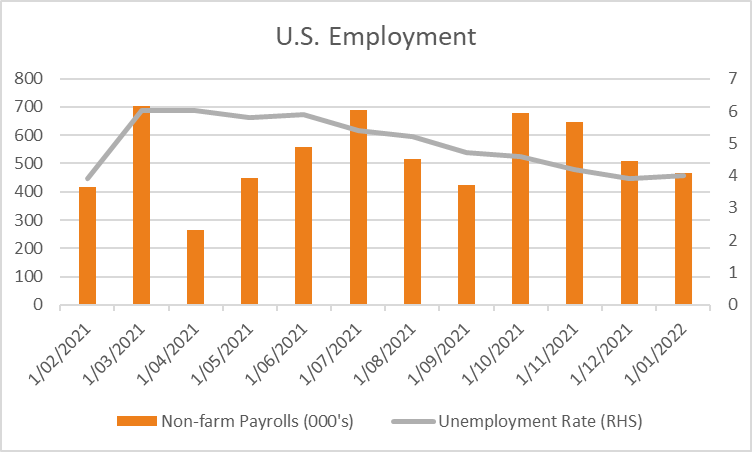

In economic data, the private ADP employment report for February was higher than estimated at 475k versus 375k forecast while the prior month saw a massive revision to 509k from -301k previously. Investors will get a better idea of the labour market on Friday with the release of non-farm payrolls for February expected to show 418k jobs were added, down from 467k previously with the unemployment rate expected to edge lower to 3.9% from 4.0% previously. As of 07:21 am AEDT the S&P500 was +1.87% higher in broad-based buying with 93% of stocks rising, as technology +2.31% and financials +2.50% contributed the most to the index’s gains. The Dow Jones also rose +1.81%, as did the Nasdaq Composite +1.69% and Russell 2000 +2.65% with the VIX retreating -8.64% to 30.44. Following Powell’s comments, Treasury yields reversed Tuesday’s declines, with the 2-year rate up +16.7 basis points to 1.508%, with both the 10 and 30-year rates +13.2 and +12.5 basis points higher respectively. Traders increased rate hike expectations for 2022 from 4.82 rate hikes to 5.79 by the end of 2022 while the U.S. dollar index was little changed at 97.37.

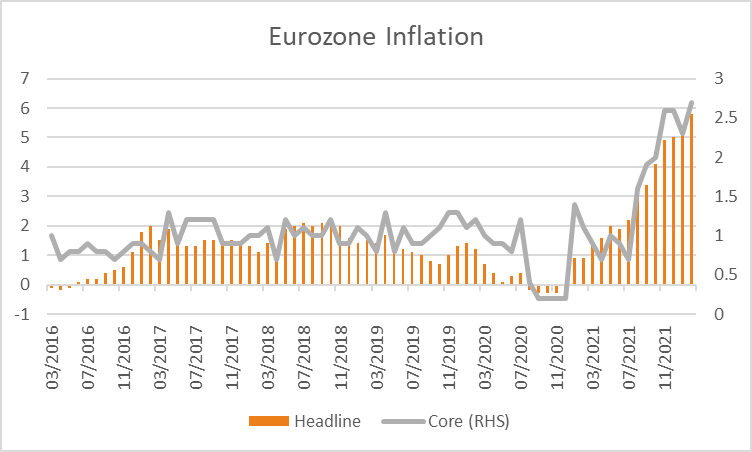

European equities also rebounded with gains in commodities supporting miners and higher yields lifting financials. The Euro Stoxx 600 rose +0.90%, as did the DAX +0.69%, CAC +1.59% and FTSE100 +1.36% despite data that showed inflation rose to a new record high, further complicating the outlook for the ECB. Headline inflation rose to +5.8% from +5.1% previously, above estimates of a +5.6% gain over the year to February with core inflation also higher than expected at +2.7% versus +2.6% forecast and +2.3% previously. In other economic data, German unemployment declined -33k in February, better than the -25k forecast with the unemployment rate slightly lower to +5.1% from +5.1% previously. Government bond yields also moved higher with 10-year yields ranging from +1.3 basis points in Sweden to +15 basis points in Italy, the Euro was little changed at 1.1127 while the Pound advanced +0.43% to 1.3382.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX looks set to follow global equities higher with ASX200 futures up +45 points or +0.63% to 7,138. The index rose +0.28% on Wednesday with a +3.0% gain in materials offsetting a -1.44% decline in financials, while energy continued to outperform, rising +4.88% on higher oil prices. In economic data, the economy expanded at +3.4% over the final quarter of 2021 slightly below estimates of +3.5% while expanding +4.2% over the year, modestly above estimates of +4.1%. The Australian dollar is trading +0.62% higher at 0.7297 while the yield on 10-year bonds fell -11.2 basis points to 2.075% although we should expect a reversal of this today given the move higher in global yields overnight.

Oil prices extended gains on Wednesday despite the U.S. and major consumers announcing the release of strategic oil reserves. Both WTI and Brent crude rose +8.34% and +9.42% respectively to US$112.15 and US$114.86 a barrel taking gains over the past year to +93.36% and +112.71%. Iron ore futures in Singapore also extended recent gains, rising +0.67% on Wednesday and trading a further +1.58% higher this morning at US$151.45. A rise in real yields weighed on gold which weakened -0.70% to US$1,931 an oz, silver edged -0.08% lower to US$25.36 as did Bitcoin, down -0.39% to US$43,727.

Economic data:

- Australian Services PMI (MoM Feb) 09:00

- Chinese PMI (MoM Feb) 12;45

- Eurozone PMI (MoM Feb) 20:00

- U.K. PMI (MoM Feb) 20:30

- Eurozone Unemployment Rate (MoM Jan) 21:00

- U.S. Initial Jobless Claims (26th Feb) 00:30

- Fed Chairman Powell Testimony 02:00

- U.S. ISM Non-manufacturing PMI (MoM Feb) 02:00

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.