Global equities rose on Wednesday as weaker economic data offset hawkish comments from the Federal Reserve’s last policy meeting which were seen as out of date given economic data has deteriorated meaningfully since.

In the minutes from the latest meeting, officials resolved to keep raising interest rates for longer to prevent higher inflation from becoming entrenched, even if that slowed the U.S. economy. Policy makers debated an increase of 0.50% to +0.75% at the next meeting in July while noting “that policy firming could slow the pace of economic growth for a time, but they saw the return of inflation to 2% as critical to achieving maximum employment on a sustained basis”. Chris Hodge, chief investment officer at Cornerstone Wealth highlighted a potential dovish point in the minutes “referencing a potential pause at year-end” which is an “extremely important. They were already thinking about where the appropriate level is to stop tightening policy in June, before the spate of economic data really deteriorated”. While the market has increasingly become convinced the Fed will pivot to save the economy, the minutes certainly drive home that inflation remains the focus over the economy for now with comments from Federal Reserve members and the minutes suggesting the Fed won’t blink for now.

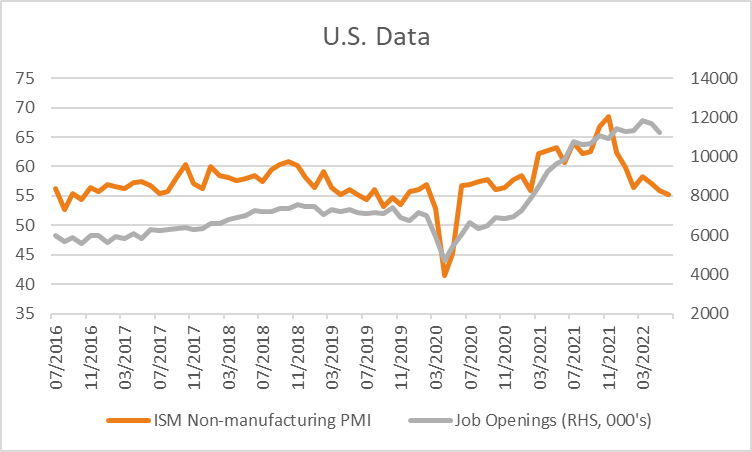

The S&P500 rose +0.36% on Wednesday, lifted by technology +0.88% and health care +0.66% while energy lagged -1.74% on lower oil prices. The Dow Jones also rose +0.23% along with the Nasdaq Composite +0.35% while the Russell 2000 was -0.79% weaker along with the VIX, down -2.94% to 26.73. The ISM non-manufacturing PMI report for June showed a slowdown from 55.9 in May to 55.3 in June as orders softened amid higher challenges and capacity constraints, although this was higher than expectations of a decline to 54.3. Meanwhile, job openings dropped 427k to 11.3 in May according to the Labor Department, a second monthly decline. In focus tonight is the ADP private employment change forecast to show +200k jobs were added in June from +128k in April, ahead of Friday’s all-important non-farm payroll data expected to show the number of jobs added slowed in June to 268k from +390k.

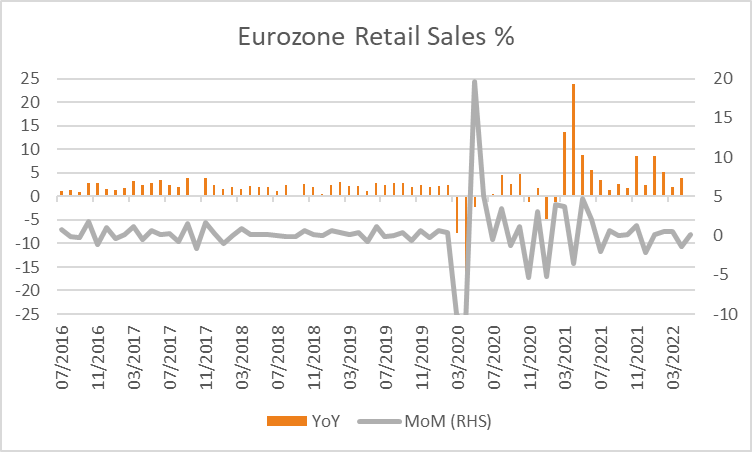

European equities climbed on Wednesday after Norwegian oil and gas workers ended their strike, easing energy supply concerns. The Euro Stoxx 600 rose +1.66% with all sectors positive except energy which fell -1.98%. The DAX also gained +1.56%, along with the CAC +2.03% and FTSE100 +1.17% with most major benchmarks higher for the session. The Pound was -0.18% lower at 1.1925 weighed by the turmoil of multiple resignations of members of Prime Minister Boris Johnson’s government as he faces yet for political turmoil over allegations of wrongdoing. Eurozone retail sales year-on-year in May unexpectedly rose +0.2% compared to estimates of a -0.4% decline, while the prior reading was revised higher to +4% from +3.9%.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX looks set to open higher this morning with ASX200 futures up +37 points or +0.57% to 6,530. The index weakened -0.53% on Wednesday weighed by a drop in materials -5.05% and energy -5.81% as commodity prices fell over recession concerns. Meanwhile, beaten-down technology names outperformed on declining peak interest rate expectations with the sector rising +3.09%. While these stocks are enjoying a recovery from their lows on declining interest rates, it should be noted that if a recession eventuates, it may weigh heavily of appetite for risk assets. The Australian dollar is -0.34% weaker overnight at 0.6779 while the 10-year bond yield is -1.3 basis points lower at 3.548%. In focus today for economic data in the Ai Group services index for June at 08:30 AEDT along with balance of trade data for May at 11:30.

Oil prices were lower overnight with both WTI and Brent crude -1.38% and -2.67% lower at US$98.11 and US$100.03 a barrel. Recent weakness is attributed to the easing of strikes in Norway as well as the potential for demand destruction amid slowing growth, however, supply-side issues of underinvestment and spare capacity remain. In a note, Goldman Sachs linked the decline to rising recession risks, noting ““We believe this move has overshot – while risks of a future recession are growing, key to our bullish view is that the current oil deficit remains unresolved, with demand destruction through high prices the only solver left as still declining inventories approach critically low levels”. Iron ore futures in Singapore finished -1.16% lower on Wednesday although are +0.31% higher this morning at US$111.15. Gold weakened a further -1.47% to US$1,738 on easing concerns of persistent inflation, rising real yields and a stronger USD. Silver was little changed at US$19.21 and Bitcoin edged -0.30% lower to US$20,380.

Economic data:

- Australian Ai Group Services Index (MoM Jun) 08:30

- Australian Balance of Trade (MoM May) 11:30

- ECB Policy Minutes 21:30

- U.S. ADP Employment (MoM Jun) 22:15

- Fed Bullard Speech 03:00

- Fed Waller Speech 03:00

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.