U.S. equities extended a bounce on Monday as investors bought the recent dip, although there was little in economic data to guide markets.

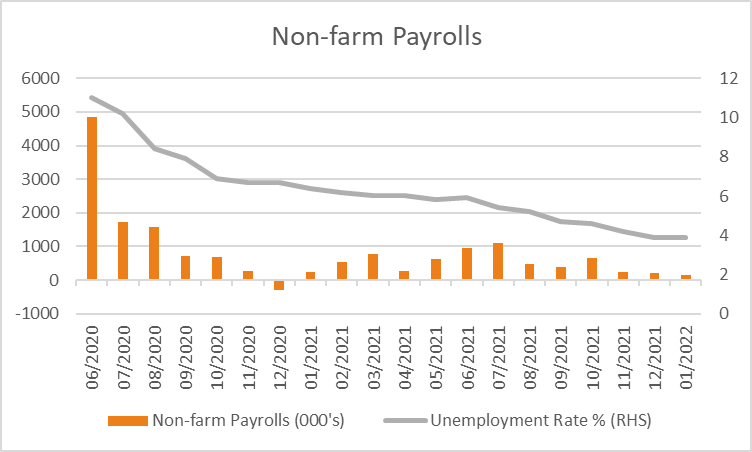

As of 07:35 am AEDT the S&P500 rose +1.0% in broad-based buying with 77% of stocks higher and all sectors positive, led by gains in consumer discretionary +3.36% and technology +2.06%. The Dow Jones also rose +0.85%, as did the Nasdaq Composite +2.82% and the Russell 2000 +1.60% with the VIX retreating -7.85% 25.49 having peaked at 31.96 last week. Ahead for the week investors will focus on the release of PMI manufacturing data for January tonight, ADP private employment on Tuesday night AEDT, ISM non-manufacturing PMI on Thursday and non-farm payroll data for January on Friday. Estimates are for +150k jobs to have been added in January with the unemployment rate to remain at 3.9%.

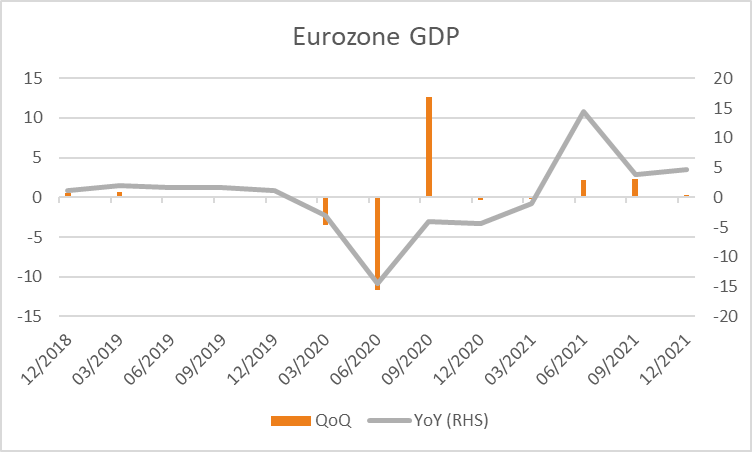

European equities were generally higher with GDP data in line with forecasts. Flash Eurozone GDP for Q4 2021 expanded at +0.3% over the quarter as forecast, down from a revised higher +2.3% in Q3. Over the year the economy expanded at +4.6% from +3.9% previously, slightly lower than the +4.7% expected by analysts. The Euro Stoxx 600 rose +0.72% lifted by technology +3.32% and industrials +1.40%. The DAX also gained +0.99%, as did the CAC +0.48%, while the FTSE100 was little changed -0.02%. The Euro rose +0.83% to 1.1244 and the Pound gained +0.39% to 1.3453 with 10-year yields across the region higher, ranging from +5.8 basis points in the U.K. to +1.2 basis points in Italy.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

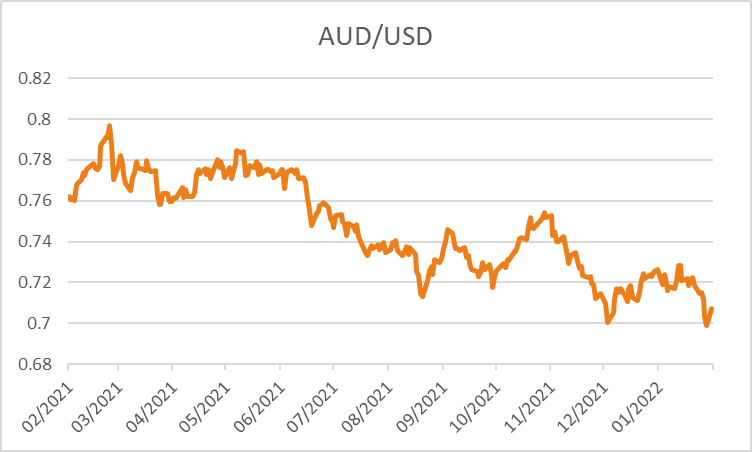

The ASX looks set to open higher this morning with ASX200 futures up +13 points or +0.19% to 6,882. The index weakened -0.24% on Monday with a -1.83% decline in financials weighing on the index while technology was the top performer rising +3.69%. A fall in the price of iron ore weighed on major miners with BHP down -1.2%, as was RIO -1.9% however, FMG rose +2.2% having declined the prior five sessions. Investors are focused on the Reserve Bank of Australia meeting today where economists are predicting the bank will end extraordinary monetary stimulus, while upgrading economist forecast and potentially bringing forward rate-hike guidance. The central bank has previously argued it will not raise the cash rate until 2023 or more likely 2024, however market pricing disagrees, pricing in a 15-bps hike by May and a total of four hikes in 2022. The Australian dollar gained +1.13% overnight to 0.7067 while the 10-year government bond yield declined -4.5 basis points on Monday to 1.895%.

Oil prices rose ahead of Wednesday’s OPEC+ meeting to discuss output with both WTI and Brent crude +1.53% and +0.87% higher at US$88.15 and US$89.30 a barrel. Iron ore futures fell -6.80% on Monday and are modestly higher this morning +1.26% at US$137.85. Gold is +0.33% higher at US$1,797 while silver is little changed -0.07% to US$22.46 and Bitcoin rose +1.74% to US$38,409.

Economic data:

- Australian Manufacturing PMI (MoM Jan) 09:00

- RBA Rate Decision 14:30

- German Retail Sales (YoY Dec) 18:00

- German Unemployment (MoM Jan) 19:55

- Eurozone Manufacturing PMI (MoM Jan)

- Eurozone Unemployment (MoM Dec) 21:00

- U.S. Manufacturing PMI (MoM Jan) 01:45

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.