Global equities surged on Friday as some investors pared bets central banks will aggressively raise rates amid mixed economic data, with some analysts also pointing to short-covering as contributing to gains.

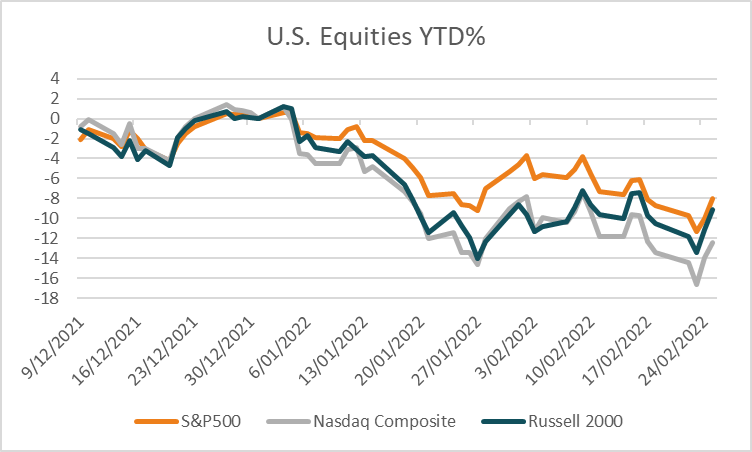

The S&P500 climbed +2.24% on Friday to edge +0.10% higher for the week with all sectors positive in broad-based buying with 97% of stocks rising. Health care +3.03%, technology +1.37% and financials +3.16% were the largest contributors to the index’s gains accounting for half of the 95.96 index points. The Dow Jones also gained +2.51%, as did the Nasdaq Composite +1.64% and Russell 2000 +2.25%. The VIX retreated -9.0% with the VIX curve back in contango, signalling short-term fear is receding and increasing the likelihood that a near term low is in place for equities. However, some analysts continue to caution about the potential for the size of gains given the ongoing conflict in Ukraine and its potential to keep inflation elevated which could weigh on growth at a time when central banks are looking to increase interest rates.

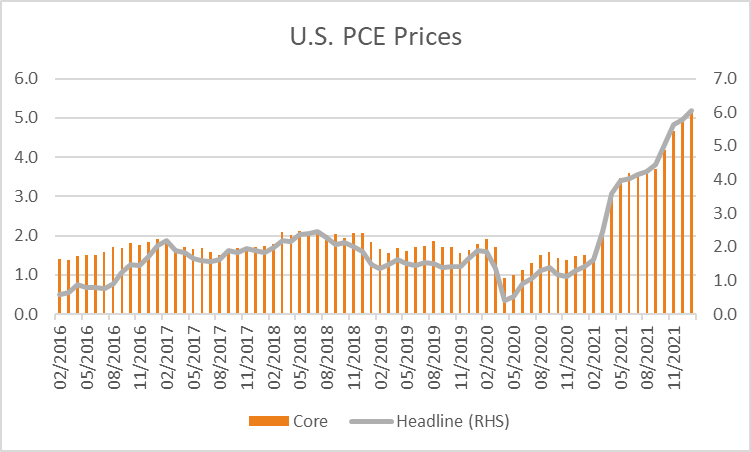

Core PCE inflation data for January on Friday showed prices rose +5.2% over the year from +4.9% previously, modestly higher than the +5.1% expected. Headline prices over the same period rose +6.1% from 5.8% previously, adding more pressure on the Federal Reserve to begin to raise rates. Meanwhile, the final reading of the University of Michigan consumer sentiment survey declined to 62.8 from 67.2 previously, although modestly higher than estimates of 61.7. Personal income for January was flat at 0%, better than the -0.3% forecast, while spending remained robust rising +2.1% versus +1.5% predicted for the month. Pricing based on Fed Fund futures still expects the Federal Reserve to raise rates next month and continue to price in 6 rate hikes by the end of 2022.

European equities also rebounded after recent selling with the Euro Stoxx 600 rising +3.32% with 96% of stocks trading higher and all sectors positive. Major European benchmarks were broadly higher across the region with the DAX rising +3.67%, as did the CAC +3.55% and FTSE100 +3.91%. Analysts are paring back bets on European equity outperformance in 2022 given a rotation into value and cyclical stocks with Goldman Sachs strategists lowering their year end target to 490 from 530 previously, implying no gains from current levels. The analysts noted the rise in risk-aversion as part of the Ukraine conflict as well as impact on both inflation and growth for lowering their price target. In economic data, the final reading of Eurozone consumer confidence for February was in line with estimates of -8.8 down from -8.5 previously while economic sentiment lifted modestly to 114 from 112.7 previously and expectations of 113.1. The Euro finished -0.97% lower on Friday at 1.1159 while the Pound rose +0.22% to 1.3409.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX is set to open decisively higher this morning with ASX200 futures up +166 points or +2.39% to 7,118 although the futures last traded before North American and European nations announced a further round of sanctions targeting Russia’s financial system. The index finished +0.10% higher on Friday, taking a weekly decline to -3.10% with a -0.99% decline in financials on Friday offsetting an +8.14% gain for technology. Ahead for the week investors will focus on retail sales for January at 11:30 AEDT today, followed by manufacturing PMI for February on Tuesday along with a policy decision by the RBA at 14:30 AEDT on Tuesday. Wednesday will bring Q4 2021 GDP data expected to show the economy expanded at +3.6% over the year and +3.0% over the quarter, followed by services PMI data on Thursday.

Oil prices declined on Friday with both WTI and Brent crude -1.31% and -1.16% lower at US$91.59 and US$97.93 a barrel. Natural gas futures for delivery in the U.K. and Netherlands slumped -30.24% and -29.81% respectively after recent surges following the invasion of Ukraine. Base metals were mixed for the week with aluminium rising +2.91%, as did lead +0.85%, nickel +0.90%, tin +0.75% and zinc +1.29% while copper declined -0.83%. Iron ore futures in Singapore declined -1.71% on Friday, although have partially reversed those declines trading +0.74% higher at US$137.75 this morning. Gold declined -0.76% on Friday to US$1,889 as risk-on assets rose, silver edged +0.23% higher to US$24.22 and Bitcoin rose +1.51% on Friday although has given back those gains trading -3.09% weaker over the weekend.

Economic data:

- Australian Retail Sales (MoM Jan) 11:30

- U.S. Advance Goods Trade Balance (MoM Jan) 00:30

- ECB President Lagarde Speech 02:50

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.