U.S. equities rose on Thursday supported by stronger economic data, while yields pushed higher and bonds declined.

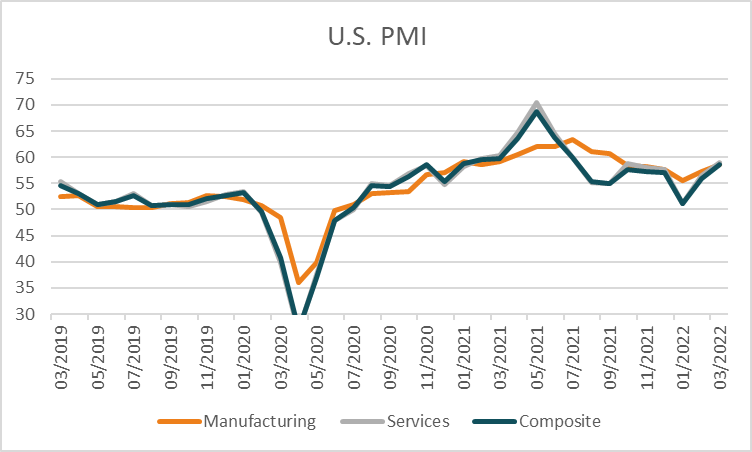

The flash reading of Markit manufacturing PMI for March rose to 58.5 from 57.3 previously, while the average estimate called for a decline to 56.3. The survey noted the pace of U.S. growth accelerated in March as COVID-19 restrictions eased and less supply chain disruptions, offsetting a drag over growing concerns from the war in Ukraine. Services also rose to 58.9 from 56.5 previously versus 56 forecast, and the composite measure rose to 58.5 from 55.9 previously. Elsewhere, U.S. initial jobless claims fell to the lowest since 1969 for the week ending March 19th with a reading of 187k from 215k previously and average estimates of 212k.

The S&P500 advanced +1.43% with 88% of stocks higher and all sectors positive, boosted by technology +2.71%, communications +1.68% and health care +1.15%. The Dow Jones also rose +1.02%, as did the Nasdaq Composite +1.93% and Russell 2000 +1.13% with the VIX declining -8.57% to 21.55. Treasuries continued to fall, pushing yields higher with the 2-year rate up +2.6 basis points to 2.122% with both the 10 and 30-year rates rising +6.0 and +3.0 basis points respectively. Chicago Fed President Charles Evan’s, who doesn’t vote on policy this year, added to recent comments by other Fed members that 0.50% rate hikes were on the table at coming policy meetings if needed. “We want to be careful, we want to be humble and nimble, and get to neutral before too long — maybe 50 helps, I’m open to that,” Evans said.

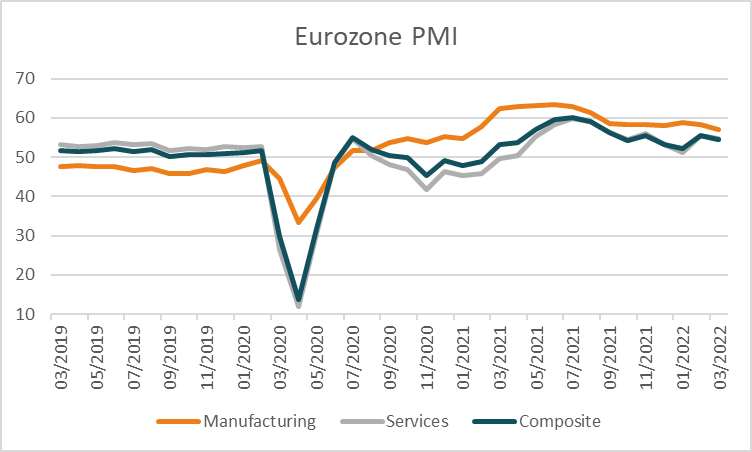

European equities were mixed after NATO agreed to boost deployments to the eastern portion of the defence alliance and the U.S. announced a new package of sanctions on Russian elites, lawmakers and defence companies. The Euro Stoxx 600 declined -0.21%, as did the DAX -0.07% and CAC -0.39% while the FTSE100 edged +0.09% higher. Eurozone manufacturing PMI declined less than forecast to 57 from 58.2 previously, against estimates of 56 with composite PMI also falling less than expected to 54.5 from 55.5 previously. Readings above 50 signal economic expansion, with the report noting the readings benefited from easing COVID-19 restrictions offsetting the impact of the war in Ukraine. Still, the short term boost is expected to fade in the coming months as the war has aggravated existing price pressures and supply chain constraints, in turn leading to record inflation in costs and selling prices that will feed through to higher consumer prices. The Euro was little changed at 1.0999 and the Pound edged -0.12% lower to 1.3189.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX looks set to follow Wall Street higher with ASX200 futures up +38 points or +0.52% to 7,386. The index pared initial losses on Thursday to edge +0.12% higher in weak breadth with only 31% of stocks rising as materials +0.97% and energy +1.95% offset a -0.38% decline in financials. JB Hi-Fi advanced +4.3% after reporting heightened consumer demand and strong sales growth in the third quarter of the financial year with sales growth up +11.3% and comparable store sales up +10.5%. Brickworks was another notable performer, rising +5% after reporting a record half-year profit of $581 million for the six months to January 31st. The economy remains in expansionary territory according to the latest PMI readings for March with manufacturing rising to 57.3 from 57 previously and services rising to 57.9 from 57.4 previously. The Australian dollar is +0.23% higher at 0.7516 while the yield on 10-year government bonds was little changed at 2.767%.

Oil prices retreated overnight with both WTI and Brent crude down -3.28% and -3.11% respectively to US$111.17 and US$117.82 as the price continues to consolidate following a sizeable rally. Iron ore futures in Singapore edged -0.11% lower on Thursday but are trading +2.0% higher this morning at US$150.75. Gold rose +0.94% to US$1,962 as did silver +1.82% to US$25.57 and Bitcoin climbed +3.53% to US$43,863.

Economic data:

- U.K. Retail Sales (YoY Feb) 18:00

- German Ifo Business Climate (MoM Mar) 20:00

- U.S. Consumer Sentiment (MoM Mar) 01:00

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.