U.S. equities rose on Monday in choppy trading while Treasury yields were mixed as investors await Friday’s inflation data.

As of 07:24 am AEDT the S&P500 was +0.32% higher with financials +0.70% and consumer discretionary +0.59% offsetting weakness in communications -1.47% while breadth was strong as 73% of stocks traded higher. The Dow Jones also rose +0.51%, as did the Nasdaq Composite +0.18% and Russell 2000 +1.14% with the VIX trading -3.88% lower at 22.30.

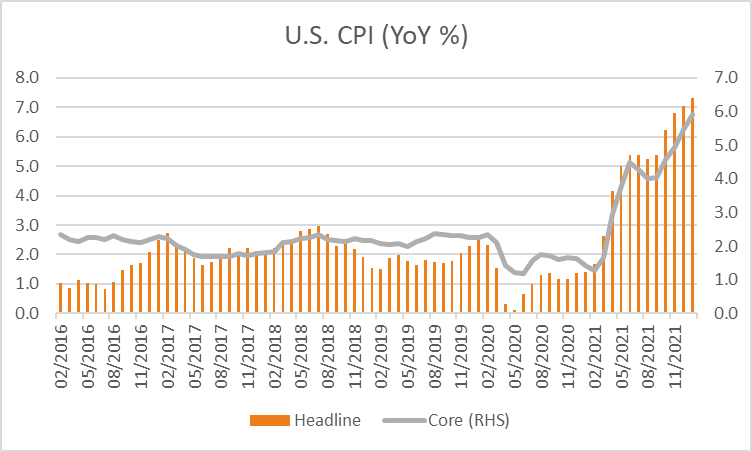

There was little in the way of economic data to guide markets with Treasury yields mixed, with the 2-year down -2 basis points at 1.290% while the 10 and 30-year rates rose +0.4 and +0.8 basis points to 1.912% and 2.218% respectively. Investors are awaiting Friday’s inflation data for January which is expected to show headline prices rose +7.3% over the year from +7% previously, with core prices rising +5.9% over the year from +5.5% in December. Based on Fed Fund futures traders expect a 0.25% rate hike in March, followed by a further +0.25% in April and a total of 5 rate increases by the end of 2022.

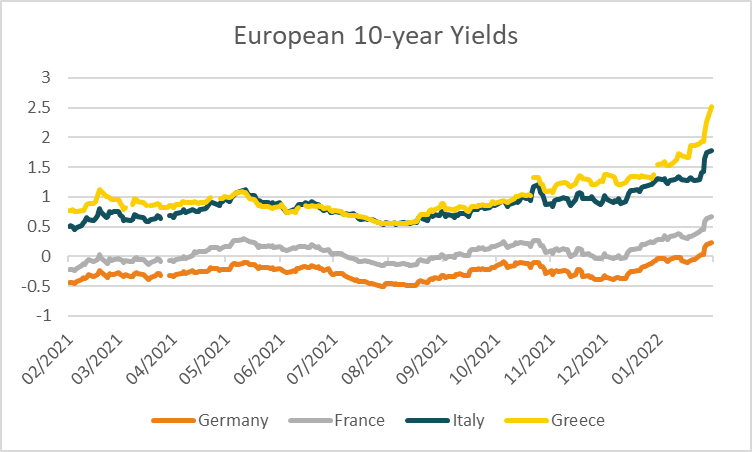

European equities were mixed with government bond yields rising after ECB member Klaas Knot said he expects a rate increase as early as the fourth quarter. The comments follow a more hawkish shift from the ECB last week with President Christine Lagarde no longer excluding a rate hike this year, although noted on Monday to European lawmakers that adjustments to policy will be “gradual” and remain data-dependent “We will remain attentive to the incoming data and carefully assess the implications for the medium-term inflation outlook,”. The Euro Stoxx 600 rose +0.68%, as did the DAX +0.71%, CAC +0.83% and FTSe100 +0.76% while Spain’s IBEX declined -0.36% along with Italy’s FTSE MIB -1.03%. 10-year government bond yields traded higher paced by Greek debt where the yield jumped +22 basis points to 2.453%, with most averaging between +5.7 and +1.8 basis points across European Union nations. The Euro edged -0.08% lower to 1.1440 and the Pound edged +0.04% higher to 1.3536.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX looks set to edge higher at the open with ASX200 futures up +11 points or +0.16% to 7,023. The index weakened -0.13% on Monday with health care -1.28% and financials -0.35% offsetting a +0.78% gain for materials. Travel stocks were notable performers after the government announced the reopening of international borders to fully vaccinated travellers in two weeks’ time with FLT up +7.8%, as was CTD +7.0%, WEB +6.17% and QAN +4.62%. Graincop gained +12.34% after providing a strong outlook and earnings guidance for 2022 expecting $480 to $540 million in EBITDA compared to $331 million reported for the 2021 financial year. In focus for earnings today is Macquarie Group, Suncorp, Computershare and GUD holdings.

Oil prices traded lower overnight with U.S. diplomats set to return to Vienna on Tuesday, resuming Iran nuclear negotiations which may path the way to restore the nations’ oil to global markets following sanctions. Both WTI and Brent crude were -0.95% and -0.51% lower at US$91.44 and US$92.78 a barrel. Iron ore futures in Singapore rose +1.65% on Monday and are a further +2.48% higher at US$151.10 in early trade this morning. Gold rose +0.73% to US$1,821 as did silver +2.37% to US$23.05 with Bitcoin extended gains rising +6.50% on Monday to US$44,395.

Economic data:

- Canadian Balance of Trade (MoM Dec) 00:30

- U.S. Balance of Trade (MoM Dec) 00:30

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.