U.S. equities extended a four-day advance on Wednesday while Treasury yields dipped with the U.S. dollar after ADP employment figures missed estimates.

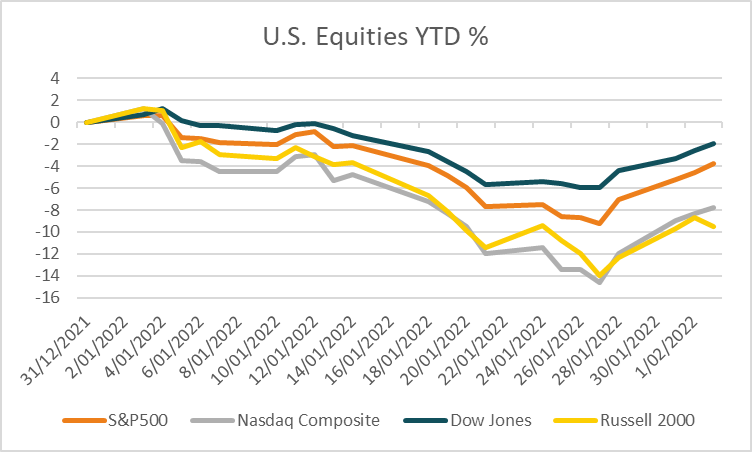

As of 07:29 am AEDT the S&P500 was +0.85% higher taking gains over the prior four sessions to +6.01% the biggest rally since November 2020. The index was lifted by communications +3.39% as Alphabet Inc. jumped +8.2% after surpassing analyst estimates for earnings after the close on Tuesday. The Dow Jones rose +0.60%, as did the Nasdaq Composite +0.40%, while the Russell 2000 slipped -0.96% and the VIX retreated -5.24% to 20.81 having traded as high as 31.96 last week.

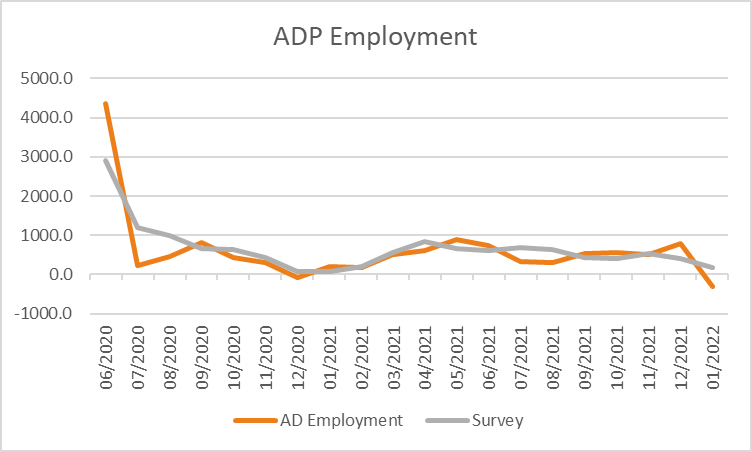

Private ADP employment for January showed the number of employed fell -301k missing estimates for a gain of +180k ahead of Friday’s non-farm payroll data. The ADP employment figures are not always a great indicator of non-farm payrolls, generally subject to revisions in the following month and the numbers as certainly impacted by the outbreak of the Omicron variant and doesn’t signal a change in the underlying strength of the labour market. Friday’s non-farm payrolls are expected to increase by +150k and impacts from the Omicron variant are expected to fade in the coming months, doing little to alter the Fed’s recent hawkish views. The 2-year Treasury yield declined -1.2 basis points to 1.154%, as did both the 10 and 30-year rates down -2.1 and -1.3 basis points to 1.766% and 2.096% respectively. Real yields across 5 and 10-years declined -1.2 and -1 basis points respectively with the U.S. dollar index weakening -0.46% to 95.94.

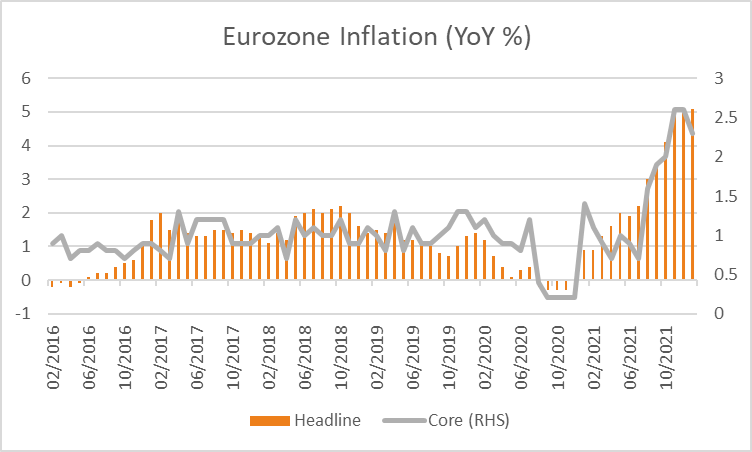

European equities were mixed on Wednesday as inflation rose more than forecast. The Euro Stoxx 600 rose +0.45%, as did the CAC +0.22% and FTSE100 +0.63% while the DAX edged -0.04% lower along with Spain’s IBEX -0.15%. Core inflation for the year to January rose +2.3%, while down from +2.6% previously, this was higher than analyst estimates of +1.9% with headline inflation rising to +5.1% from +5.0% previously against estimates for a decline to +4.4%. The data marks the seventh consecutive upside surprise in the headline rate and places further pressure on the ECB ahead of its monetary policy meeting on Thursday. The Bank of England also concludes a monetary policy meeting on Thursday where economists are forecasting a +0.25% rate hike. The Pound strengthened +0.46% to 1.3584 as did the Euro +0.33% to 1.1309 with 10-year government bond yields across the region mixed ranging from -4.3 basis points in the U.K. to +1.9 in Portugal.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX looks set to edge up at the open with ASX200 futures +14 points or +0.20% higher at 6,996. The index climbed +1.17% on Wednesday lifted by materials +1.96% and financials +1.05% with 84% of stocks trading higher in broad breadth. In a speech on Wednesday, RBA governor Philip Lowe signalled a shift in the banks’ outlook conceded the potential for a rate hike in 2022 in line with market pricing. Still, Lowe had an upbeat tone on the economy and downplayed the risks of inflation. Lowe noted, “Faster progress towards full employment and inflation consistent with the target does bring forward the timing of the likely increase in interest rates”. “It will depend upon how the supply issues are resolved and the strength of the pickup in labour costs. If things go well and the economy performs stronger, there is clearly scenarios where we’d increase rates later this year.” The Australian dollar rose +0.24% to 0.7146 and the 10-year government bond yield rose +1 basis point to +1.913%.

Oil prices edged higher after OPEC+ agreed to increase production by a further +400k barrels per day from March as widely forecast despite the group struggling so far to fulfil its supply increases so far and concerns over low inventories and space capacity have helped propel the rally in oil prices. Both WTI and Brent crude traded +0.14% and +0.44% higher respectively at US$88.31 and US$89.54 a barrel. Iron ore futures in Singapore rose +2.01% on Wednesday and are a further +1.27% higher this morning at US$141.60. Gold rose +0.36% to US$1,807 benefiting from a weaker USD and slightly lower real yields, silver gained +0.20% to US$22.69 while Bitcoin slipped -2.95% to US$37,670.

Economic data:

- Australian Services PMI (MoM Jan) 09:00

- Eurozone Composite PMI (MoM Jan) 20:00

- U.K. Composite PMI (MoM Jan) 20:30

- BOE Rate Decision 23:00

- ECB Rate Decision 23:45

- U.S. ISM Non-manufacturing PMI (MoM Jan) 02:00

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.