US Equities rallied on the back of weak manufacturing data with investors reassessing how high the Federal Reserve will need to hike rates.

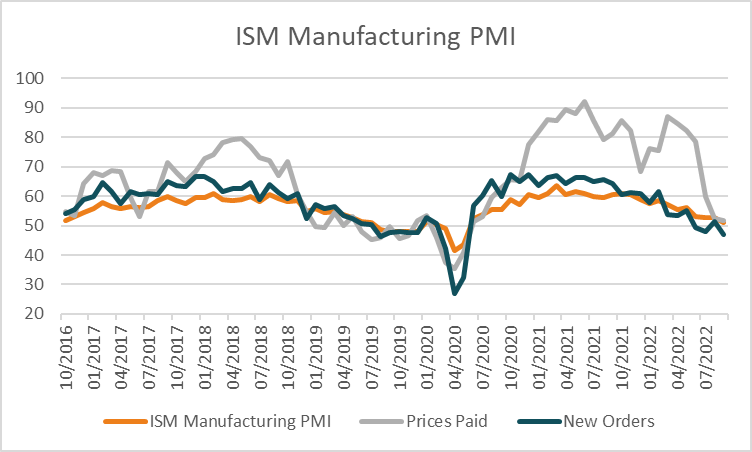

The S&P 500 was up by +3.04% with all sectors closing higher. Energy, materials and information technology made the largest gains, rising by +6.1%, 3.69% and 3.49% respectively. The Dow rose by +3.01% the Nasdaq gained +2.65% and the Russell 2000 closed +3% higher. The ISM Manufacturing PMI for September declined to 50.9, below forecasts of 52.2, with new orders declined more than expected to 47.1 from 51.3 previously, missing estimates of 50.5, encouraging investors to believe inflation would be slowing down and reduced hikes in the Fed rate. David Madden of Equiti Capital explains, “High inflation is the reason why the Fed is tightening monetary policy and considering the fall in prices paid, we could be witnessing further signs that we are beyond peak inflation.” Investors in the US are concerned about the Fed’s decision on aggressive monetary ning to plunge the economy into recession. Chief Market strategist for Miller Tabak, Matt Maley commented, “The market is oversold, and sentiment is extremely negative, so a bounce…even a sharp one…could happen at any time”, adding “However, we see lower-lows before the ultimate bottom is reached for this bear market…as the stock market has not fully priced-in a recession.”. The yields on U.S. Treasuries slumped with the 2-year rate down -15.9 basis points to 4.12% with the 10 and 30-year rates also -16.6 and -7.8 basis points lower at 3.65% and 3.69% respectively.

Markets in Europe rallied on Monday on Britain’s tax cut reversal and high oil prices. The Euro STOXX 600 closed +0.67% higher, with energy rising +2.85%, utilities up +2.18% and communications gaining +1.94%. The FTSE 100 gained +0.22%, the CAC 40 was up 0.55%, the DAX +0.79%. The markets have headwinds in the region due to political turmoil in the UK, and the Russia-Ukraine conflict leading to an energy crisis. Analysts at Nordea Asset Management commented on the recent market’s performance, “Bond market turmoil is shaking equity markets as investors struggle to understand the future path of growth and inflation.” Strategists at BNP Paribas meanwhile reduced their outlook for the region, citing pressure on 2023 corporate earnings.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX is expected to open higher this morning, with ASX futures up 118 points or 1.83% to 6570. The index shed -0.3% on Monday with information technology, consumer staples and consumer discretionary weighing the most heavily, down -1.34%, -1.13% and -0.83% respectively, offsetting the gains made by utilities which rose +1.55% and energy that was up by +1.01%. Iluka Resources climbed +2.9%, becoming one of the top performers of the index. Yancoal Australia gained +4.9% after announcing plans to repay its debt as a result of robust coal prices. BHP Group rose +0.2%, Fortescue Metals was up +0.6%, while Rio Tinto slipped -0.3%. Lithium miners underperformed, with Core Lithium falling by -4.1% while Allkem declined -4.8%. Liontown Resources fell -2.3% after receiving state approval from WA for closing down operations at Kathleen Valley. Mineral Resources outperformed the sector rising +0.6%. Janus Henderson dropped -5.1% after announcing the retirement of chairman Richard Gillinwater. Pendal shares fell -2.2%, after the board announced it had accepted Perpetual’s proposal of one share for every 7.5 Pendal shares, in addition to $1.96 of cash. Investor focus will be on the RBAs meeting today, where the cash rate is forecast to be raised by half a percent to 2.85%. The yield on the 10-year Australian treasury bond rose +1.4 basis points to 3.899% on Monday while the Australian dollar is +1.80% higher at 0.6515.

In commodities, oil prices rallied on the rumor that OPEC+ would curtail production by more than 1 million barrels/day this week to stabilize prices, prior to their official announcement on Wednesday. WTI crude and Brent Crude rose by +5.25% and +4.33% to $83.62 and $88.79 respectively. In precious metals, spot gold jumped +2.18% to $7,696.86, spot silver closed +8.45% higher at $20.64, copper prices edged +0.12% higher, SGX Iron Ore is +0.16% higher this morning at US$92.40 after falling -2.11% on Monday.

Economic Calendar:

- Australian Manufacturing Index (MoM Sep) 08:30

- US Fed Bostic Speech 09:45

- Australian Building Permits (MoM Aug) 11:30

- RBA Interest Rate Decision 14:30

- Fed Williams Speech 00:00

- Fed Mester Speech 00:15

- ECB Lagarde Speech 02:00

- Fed Daly Speech 04:00

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.