U.S. equities finished modestly higher on Thursday, lifted by better-than-expected economic data.

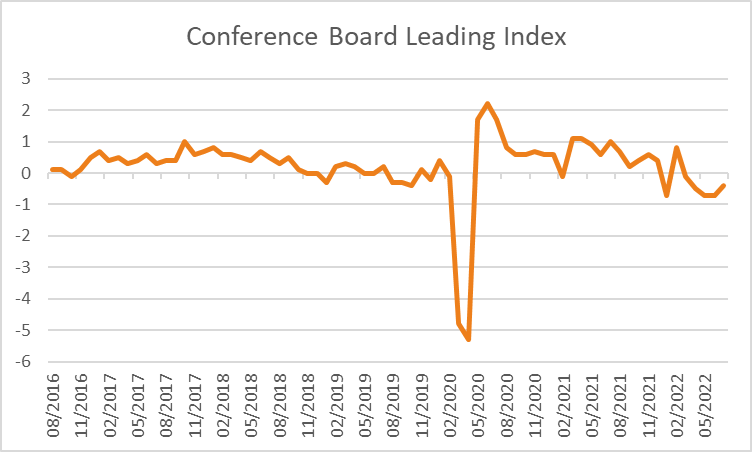

The S&P500 closed +0.23% higher boosted by technology +0.49% and energy +2.53% following lower yields and higher oil prices. The Dow Jones edged +0.06% higher, as did the Nasdaq Composite +0.21% and Russell 2000 +0.68% with the VIX finishing -1.71% lower at 19.56. Initial jobless claim data for the weekend ending 13th August was better-than-expected at +250k versus +264k expected with the prior weeks figure revised lower from +262k to +252k pointing to strength in demand for labour. Elsewhere, the Conference Board’s leading index declined less than forecast for the month of July, down -0.4% compared to forecasts of -0.5% while existing home sales declined -5.9% in July from -5.5% in June as higher interest rates continue to cool the housing market.

As attention turns to next weeks Federal Reserve Jackson Hole symposium, St Louis Federal Reserve President James Bullard told the Wall Street Journal he backed another +0.75% increase in September while Minneapolis Fed’s Neel Kashkari said the central bank has “more work to do” in raising rates to curb inflation. Despite those comments, Treasury yields declined with the 2-year rate down -8.1 basis points along with the 10 and 30-year rates by -1.3 and -1.1 basis points respectively.

European equities were also higher as the final reading of Eurozone inflation data for July was unchanged. Core prices rose +4% over the year to July as forecast, up from +3.7% previously and gained +0.1% over the month while headline prices rose +8.9% from +8.6% in June with slightly over +4% of the increase related to higher energy prices. The Euro Stoxx 600 rose +0.39% along with the DAX +0.52%, CAC +0.45% and FTSE100 +0.35% with most benchmarks higher across the region.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

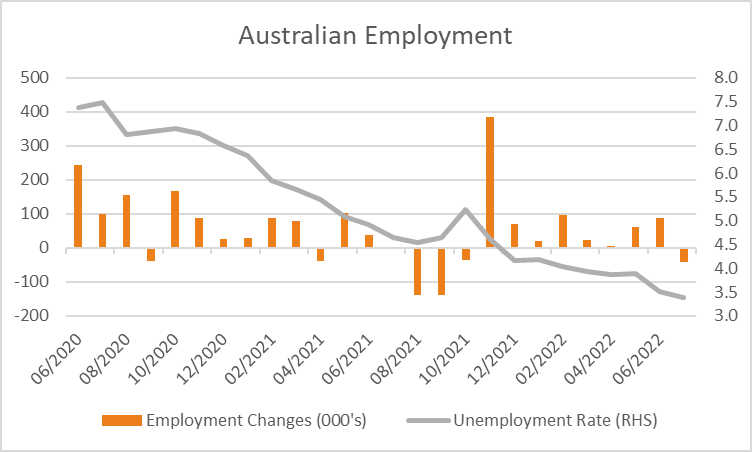

The ASX is expected to open higher this morning with ASX200 futures up +23 points or +0.33% to 7,043. The index declined -0.21% on Thursday as declines in materials -0.39% and consumer discretionary -1.27% offset gains in health care +1.11% and energy +1.37%. Shares in Blackmores slumped -10.1% after reporting a rise in profit and revenue but warning of rising costs and supply chain issues. In economic data, the number of employed unexpectedly declined in July by -40.9k compared to estimates of +25k while the unemployment rate edged lower to +3.4% from +3.5% previously as the participation rate moved lower due to illness, flooding and school holidays. According to Bloomberg Economists, “The data showed growth in labor supply continued to accelerate. We expect employment to start expanding again in August, and the unemployment rate to begin rising over the second half of 2022. The latter should pave the way for the RBA to shift to a more gradual pace of policy tightening over coming months”. The Australian dollar weakened a further -0.29% overnight to 0.6914 declining for a fourth consecutive session while the 10-year government bond yield was +6 basis points higher at 3.334%.

Oil prices rose overnight with both WTI and Brent crude up +2.72% and +3.14% respectively at US$90.51 and US$96.59 supported by a larger than expected draw in U.S. inventories on Wednesday as well as an apparent stall in Iranian nuclear negotiations according to analysts at energy consulting firm Ritterbusch and Associates. Iron ore futures in Singapore edged +0.11% higher on Thursday although are trading -0.55% lower at US$101.20 this morning while copper prices rose +1.74%. Gold traded -0.17% lower at US$1,758.74 an oz along with silver -1.29% to US$19.55 while Bitcoin was little changed at US$23,428.

Economic data:

- U.K. Retail Sales (YoY Jul) 16:00

- Fed Barkin Speech 23:00

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.