US equity markets fell on Friday after non-farm payroll data pointed to continued hikes by the Federal Reserve.

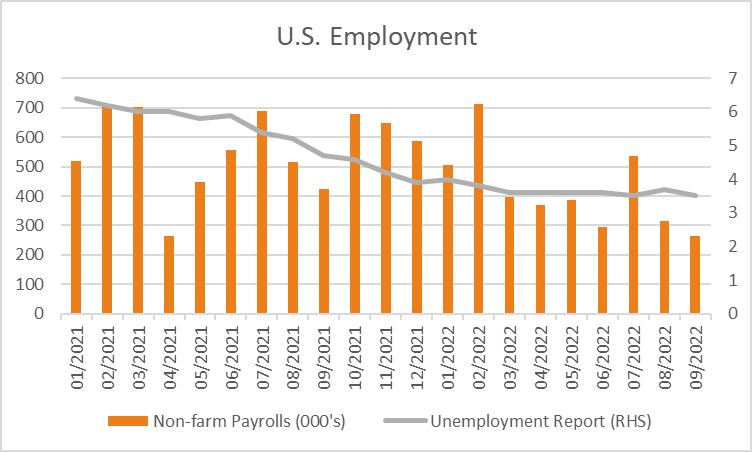

The S&P 500 closed -2.8% lower in broad-based selling with 94% of stocks lower as information technology sunk by -4.14%, consumer discretionary was down -3.54% while communications lost -2.85%. The Dow slipped -2.11%, the Nasdaq Composite fell -3.8%, the Russell 2000 declined -2.11%, while the VIX index was up by +2.75% to 31.36. In economic data, the monthly non-farm payrolls survey revealed 263k jobs were added in September beating forecasts of 250k, while the unemployment rate receded to 3.5% from 3.7% in the previous month. The hourly earnings rose by 0.3% or 10c to $32.46. The average hourly earnings were steady at 0.3% on a month-on-month basis, however, fell to 5% compared to 5.2% on a year-on-year comparison. CIO of Schroders commented on the possibility of a reduction in the cash rate, “You’re not seeing enough evidence to give the Fed the freedom to moderate the pace of tightening.” This week will be filled with the release of more economic data used to assess further hikes in the Fed rate. The PPI report for September is expected to be released on Wednesday, followed by inflation data on Thursday, expected to show headline prices rose +8.1% over the 12 months and core prices increased +6.5%. Also in focus is the release of retail sales on Friday along with the Michigan Consumer Sentiment report as Q3 earnings season begins. Minutes from the Fed’s September meeting will also provide signs for the Fed’s appetite for further interest rate hikes. The 10-year treasury bond yield rose 6 basis points to 3.88%, while the treasury market will be closed on Monday on account of Columbus Day.

In Europe, markets closed lower on Friday amid growing regional geopolitical uncertainty. The Euro STOXX 600 was -1.75% lower, weighed down by information technology, real estate and consumer discretionary falling by -4.04%, -2.38%, -2.28%. The FTSE was down by -1.13%, the CAC declined -1.17% and the DAX fell -1.59%. Traders were still recovering from the UK’s bond market decline and now will be preparing for the possibility of Italy’s newly elected government’s economic policies causing further hurdles for policymakers. Portfolio manager at Federated Hermes stated that the Italian budget, “will be even more closely scrutinized given what has unfolded in the UK.”

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX is set to open lower today, with ASX futures down 61 points or 0.9% to 6703. The ASX 200 closed -0.8% lower on Friday, falling 54.7 points to 6762.8 with the energy sector being the only sector gaining +0.95% due to higher oil prices. The biggest laggards were real estate, information technology and materials slumping by -2.0%, -1.77% and -1.17% respectively. Energy stocks performed well, with Woodside rising 10% over the week, Karoon Energy up +9.2%, and Stanmore Resources soared +9.6%. GQG partners fell -9.3% after announcing Assets Under Management in September fell to $1.5 billion, while Magellan shares tumbled -11.6%. The chief economist at AMP, Shane Oliver, shared his thoughts on the impact of rising cash rates on stocks, ”Shares remain at high risk of further falls in the short term as central banks continue to tighten, uncertainty about recession remains high and geopolitical risks continue.” The Australian 10-year bond yield added 6 basis points to close at 3.8%, while the local currency was down 0.5% to $63.75.

In commodities, oil prices continued to rise with the WTI and Brent jumping +4.74% and +3.71% to $92.64 and $97.92. Precious metals were lower as spot gold declined -1.03% to $1,694.82, spot silver was down by -2.45% to $20.13 while the price of bitcoin declined by -0.6% to $19,411. Copper fell -1.73% to $339, SGX Iron Ore was steady at $95.8, nickel slipped -1.35% to $22,366,

Economic Calendar

- AUS Ai Group Services Index (MoM Sep) 08:30

- Fed Evans Speech 00:00

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.