U.S. equities reversed initial gains to finish mixed on Thursday while Treasury yields climbed after weak demand at a 30-year auction.

The S&P500 reversed initial gains of as much as +1.1% before finishing -0.07% lower weighed by declines in technology -0.48% and health care -0.71% while energy outperformed +3.19% on higher oil prices. The Nasdaq Composite was also -0.58% weaker while the Russell 2000 rose +0.31% along with the Dow Jones +0.08% and the VIX rose +2.33% to 20.20.

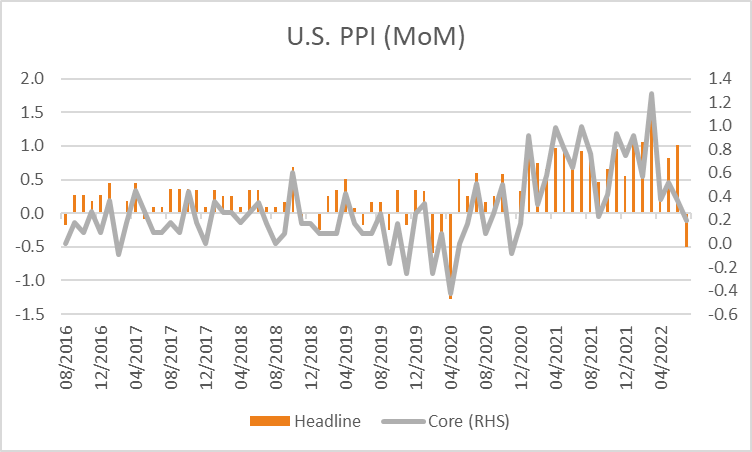

In economic data, U.S. producer prices declined for the first time in two years, reflecting a drop in energy costs. For the month of July, prices declined -0.5% compared to forecasts for a +0.2% increase with a core measure excluding food and energy rising +0.2% also lower than the +0.4% predicted, adding weight to the view inflation may have finally peaked following Wednesday’s softer-than-expected inflation data. Treasury yields were higher across the curve after a 30-year auction of Treasuries drew a higher yield than pre-auction trading with the 2-year yield rising +1.1 basis point along with the 10 and 30-year rates by +10.5 and +13.5 basis points respectively.

European equities were also mixed following sizeable gains on Wednesday with the Euro Stoxx 600 rising just +0.06% along with the CAC +0.33% while the DAX and FTSE100 were -0.05% and -0.55% lower respectively. In focus tonight is the release of U.K. GDP for the second quarter expected to show growth of +2.8%, down from +8.7% previously while year-on-year Eurozone industrial production is expected to show a moderation to +0.8% from +1.6% previously. Economists at Citi expect a 1% contraction in Eurozone real GDP next year, noting “with this deeper recession implying a 10% EPS contraction over the next 12-months, a more bearish forecast than analyst consensus” citing rising energy prices as the main culprit.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX looks set to open lower this morning with ASX200 futures down -0.24% or -17 points to 6,949. The index climbed +1.12% on Thursday boosted by gains in materials +1.50% and financials +1.01% in broad-based buying with 80% of stocks rising, while utilities -1.49% was the only sector negative. Shares in Telstra weakened -1.25% after reporting a dip in revenue and profits although did announce a surprise increase in the final dividend to $0.085. Elsewhere, Mirvac rose +3.85% after reporting a rise in earnings of +4.6% with revenue climbing +20% to $2.8 billion. The Australian dollar is modestly higher by +0.24% to 0.7106 with the 10-year government bond yield up +4.5 basis points on Thursday to 3.289%.

Oil prices climbed overnight despite OPEC cutting its 2022 forecast for oil demand for a third time since April expecting demand to rise by +3.1 million barrels per day, down -3.2% or -260k from its previous forecast. This was offset after the International Energy Agency released a report show it expects “soaring oil use for power generation” expecting global demand to rise +380k barrels per day to 2.1 million. Both WTI and Brent crude rose +2.46% and +2.11% respectively to US$94.17 and US$99.46 a barrel. Iron ore futures in Singapore rose +2.18% on Thursday although are -0.43% weaker this morning at US$111.80 while copper rose +1.22%. Gold edged -0.13% lower to US$1,789.99 an oz overnight with silver -1.38% lower to US$20.31 while Bitcoin gained +1.29% to US$24,212.

Economic data:

- U.K. GDP (QoQ Q2) 16:00

- Eurozone Industrial Production (YoY Jun) 19:00

- University of Michigan Consumer Sentiment (MoM Aug) 00:00

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.