Global equities rallied on Monday, boosted by a drop in U.K. bond yields after new finance minister Jeremy Hunt scrapped most of the proposed 45 billion pounds of unfunded tax cuts.

The S&P 500 rose +2.57% with all sectors closing higher. Consumer discretionary, real estate and communications leapt +4.06%, +3.70% and +3.44% respectively. The Dow rose +1.8% the Nasdaq gained +3.24%, The Russell 2000 index climbed +2.63%. The VIX index fell -2.94% to 31.08, while the yield on the US 10-year note was 4 basis points lower to 3.98%.

Mark Haefele at UBS Global Wealth Management commented on the market’s performance, “Despite the increased risks to growth and the rise in volatility, equity markets have neither become cheaper relative to bonds, nor yet priced in a material slowdown in growth and earnings.” Corporate earnings will be released this week, starting with the Bank of America announcing a drop in quarterly earnings by 9%, lower than forecast. Goldman Sachs announced a major reorganization into three divisions, details of the plan are expected to be shared today along with their third-quarter earnings. Silvercrest Asset Management managing director, Robert Teeter commented, “Inflation clearly remains a problem until proven otherwise, and disappointing earnings, particularly from consumer facing companies, could trigger another rough stretch, with recession fears at the fore.” Meanwhile, technology stocks rallied with Tesla up by +7%, Netflix +6.5%, Amazon +5.7% and Apple +2.2%.

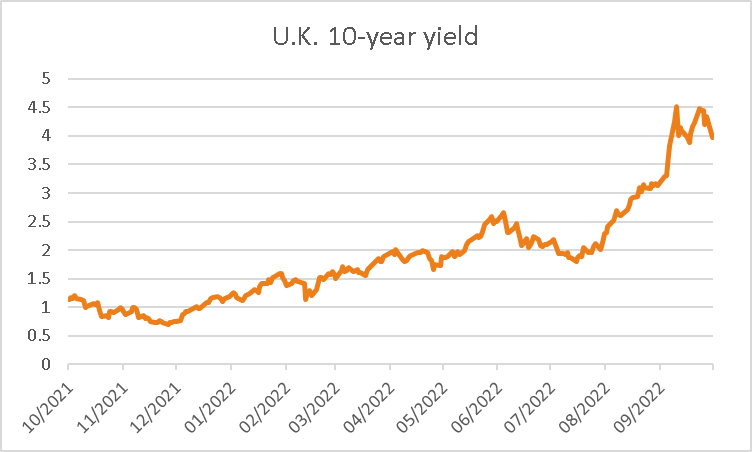

In Europe, markets closed rallied on Monday, after the UK abandoned plans for tax cuts which had rattled markets last week. The Euro STOXX 600 index closed +1.6% higher with all sectors closing higher. Real estate, consumer discretionary and utilities lead the gains by closing +3.66%, +2.61% and +2.22 higher. Jeremy Hunt, the new Chancellor of the Exchequer confirmed the UK’s policy U-turn, boosting market sentiment. The FTSE closed +1.86% higher, the CAC gained +1.83% and the Dax jumped +1.7 respectively, while the UK 10-year yield tumbled 36 basis points to 3.96%. Strategists at Liberum commented on the impact of the change in UK government’s policy on the markets, “We see this as a major positive to calm markets down and expect gilt yields to decline further in coming weeks.”

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX is expected to open higher today, as ASX futures were up 62 points or 0.93% to 6724. The ASX 200 closed -1.4% lower on Monday in broad-based selling following losses on Wall Street on Friday. Energy and materials were the biggest laggards down by -2.11% each, followed by consumer discretionary and consumer staples down by -1.43% and -1.32% respectively. Lithium stocks outperformed the index, after the price of lithium batteries soared in China to a record $118,807.2. Core lithium rose by +5.2%, Liontown Resources gained 4.9%, Lake Resources advanced 3.1% and Pilbara Minerals jumped 2.1%. Beach Energy lost -3.7%, Woodside Energy fell by -2.4% while Santos lost -2.9%, Whitehaven -0.2%, New Hope gained +0.1%. Amongst the bigger names, BHP lost -2.3%, Fortescue metals was down by -1.2% and Rio Tinto slide -2.6%. Costa Group’s share price plunged -13.4% due to “adverse weather conditions” hurting citrus crop yield, translating to ‘considerably lower’ earnings. In insurance, Medibank declined by -3.4% after resuming trading following a forced shutdown of systems due to a ransomware attack. Insurance Australia rose +1.6% following an announcement of a $350 million buyback. Meanwhile, Endeavour Group, the biggest pub operator in Australia, gained +1.5% after sales jumped to $3 billion in the first quarter. The yield on the 10-year Australian bond was +1.5 basis points higher at 4.023%, while the Australian dollar gained strength against the greenback by rising 1.42% to 0.6287.

China announced there would be a delay in the release of the country’s third-quarter GDP figures due to the national party meeting. Oil prices slipped with WTI and Brent down -0.14% and -0.01% to $85.49 and $91.66 respectively. In precious metals, spot gold edged +0.45% higher and spot silver rose +2.05% to $18.66. Industrial metals were mixed with copper slipping -0.58% to $340, SGX Iron ore rose up by +1.95% to $93.77, and the price of bitcoin gained 1.9% to $19,506.

Economic Calendar:

- Inflation Rate YoY (Q3) 08:45

- RBA Bullock Speech 11:05

- RBA Meeting Minutes 11:30

- Eurozone Economic Sentiment Index (MoM Oct) 20:00

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.