Global equities fell on Tuesday after the Bank of England warned it would remove market support aimed at addressing volatility in the bond market at the end of this week, rattling investor sentiment.

As of 3:50pm New York time the S&P 500 weakened -0.65% lower, with information technology, communications and financials down -1.52%, -1.64% and -1.30% respectively. The Dow rose +0.12%, the Nasdaq Composite fell -1.10% and the Russell 2000 declined by -0.84%. The VIX index rose by +4.65% to 33.96, while the US 10-year bond gained +5.3 basis points to 3.935%. The IMF shared warnings of a global recession impacting the markets, as financial instability will have spillover effects between economies. The global lender warned of “storm clouds” looming, citing persistent inflation and a decline in China’s output due to the ongoing Russian-Ukraine conflict. Director of the IMF’s Monetary and Capital Markets Department Tobias Adrian stated, “It’s difficult to think of a time where uncertainty was so high”. The IMF has reduced its forecast for global growth next year to 2.7%, with a 25% probability of a further decline to 2%. Inflationary data on Thursday are expected to help confirm another 75-basis point hike in the fed rate while the latest policy minutes from the Federal Reserve will be released overnight along with producer price inflation data expected to show a +0.2% increase over the month of September.

European markets declined on Tuesday, as traders await inflation data from the US while recession fears and geo-political tensions continue to encompass the region as well as the Bank of England’s decision to withdraw support for the bond market at the end of the week. The Euro STOXX 600 index closed -0.63% lower, weighed down by information technology, utilities, and energy which fell by -1.88%, -1.82%, and -1.77% respectively. The FTSE slid -0.87%, the CAC was down -0.13% with the DAX also -0.43% lower. The IMF was critical of the UK government’s mini-budget, commenting it’s “not going to work very well” and the proposed “fiscal package is going to be consistent with what the Bank of England is trying to do.” Meanwhile, Swiss National Bank President Thomas Jordan hinted at increasing the country’s interest rates as price pressures begin to build in the economy.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

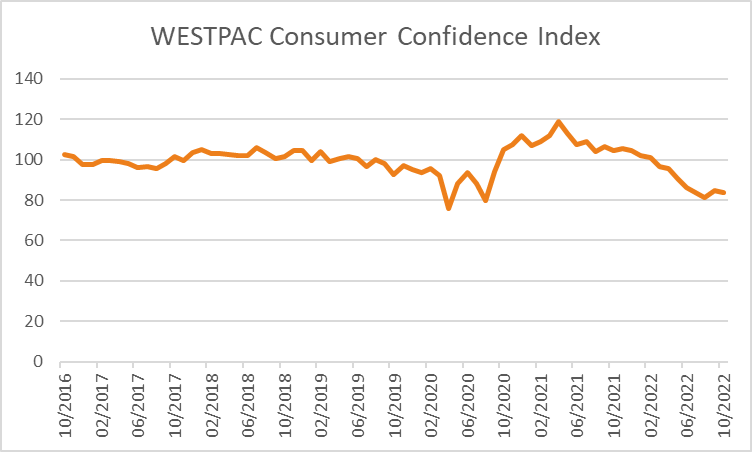

The ASX is set to open lower this morning, with ASX futures down -22 points or -0.33% to 6,621. The ASX 200 closed -0.34% lower on Tuesday, weighed down by energy, information technology, and real estate which fell by -1.59%, -0.96% and -0.94% respectively. GrainCorp rose +4.2% as wheat futures on Monday hit a record high due to the Russian-Ukraine conflict. Johns Lyng Group advanced +5.9% after it emerged that the company’s CEO sold 4 million shares. Whitehaven Coal slipped by -0.8%, Mineral Resources gained +2.8%, BHP Group dropped -0.4%, Woodside Energy fell 2.4%. Deterra Royalties shares gained +1.5% after Goldman Sachs increased the company’s recommendation to “buy”. Telstra’s share price rose 0.3% after shareholders approved a restructuring strategy to separate the company into four separate entities. Baby Bunting lost 20.5% of its stock price, after revealing the company’s gross profit margins had shrunk by -2.3%. The Westpac Consumer Confidence Index edged slightly lower from 84.4 in September to 83.7 in October, while building permits rose by 28.1% in August.

Oil prices were lower, with WTI and Brent Crude falling -2.9% and -2.73% to $88.47 and $93.56 respectively. In precious metals, spot gold rose up by +0.34% to $1,674.29 while spot silver fell -1.5% to $19.31. Industrial metals were mixed with copper rising +0.34% to $344, nickel slipping -0.38% to $22,282, while SGX Iron Ore declined by -1.7% to $97.05 and the price of bitcoin dropped -1.2% to $18,993.

Economic Calendar:

- RBA Ellis Speech 09:00

- Japan Machinery Orders (YoY AUG) 10:50

- UK GDP (YoY AUG) 17:00

- U.S. PPI (MoM Sep) 23:30

- ECB Lagarde Speech 00:30

- FOMC Minutes 05:00

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.