U.S. equities rallied on Thursday supported by positive economic data as the second estimate of Q2 GDP showed the economy contracted less than initially estimated.

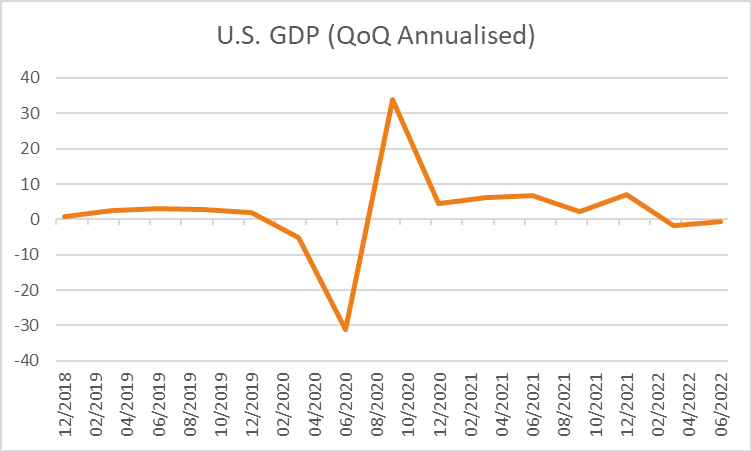

The economy contracted at a -0.6% annualised pace in Q2, less than the initial reading of -0.8% as consumer spending helped to offset a drag from a sharp slowdown in inventory accumulation. Elsewhere, initial jobless claims for the week ending August 20th were also better than expected at 248k compared to forecasts of +253. In focus tonight is Fed Chair Jerome Powell’s speech at the Jackson Hole Symposium with Chief Economic Adviser at Allianz SE Mohamed El-Erian noting on Bloomberg television “The Fed should not blink” as it addresses hot inflation and Powell faces a huge challenge finding ways to cool price growth without damaging the economy. Also released tonight is PCE inflation for July expected to show core prices moderated over the 12 months to +4.7% from +4.8% along with headline prices expected to rise +6.4% from +6.8% previously.

The S&P500 climbed +1.41% in broad-based buying with 93% of stocks higher supported by gains in technology +1.68%, communications +2.06%, and financials +1.52%. The Dow Jones also rose +0.98%, as did the Nasdaq Composite +1.67% and Russell 2000 +1.52% with the VIX retreating -4.56% to 21.78. Treasury yields were lower with the 2-year rate down -2.2 basis points to 3.368% along with both the 10 and 30-year rates by -7.4 and -7.1 basis points respectively. St. Louis Fed President James Bullard on Thursday noted he favours “front-loading” interest rates and likes “the idea that you get the rate increases in earlier rather than later…You show you are serious about inflation fighting and you want to get up to the level that will put downward pressure on inflation”.

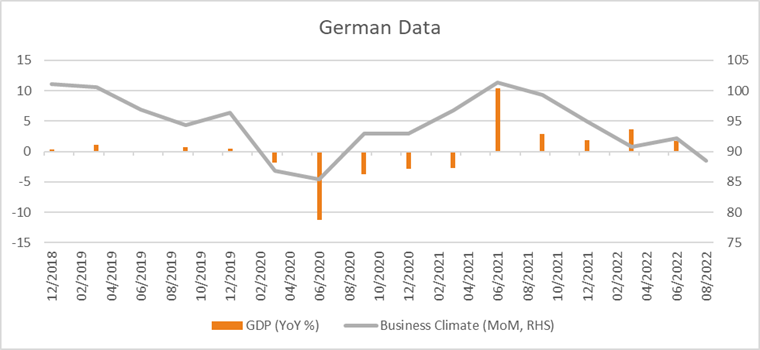

European equities also finished higher following more stimulus from China on Thursday as well as upbeat German economic data with policymakers in China announced a further $146 billion in funding largely focused on infrastructure spending. Meanwhile, the German economy grew +1.7% over the 12 months to Q2, higher than the forecast +1.4% with the Ifo business climate survey also better than expected at 88.5 while analysts called for a lower reading of 86.8. The Euro Stoxx 600 rose +0.30% along with the DAX +0.39% and FTSE100 +0.11% while the CAC edged -0.11% lower.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX is set to open flat this morning with ASX200 futures up just +4 points or +0.06% to 6,979. The index rose +0.71% on Thursday with financials +0.77% and materials +0.72% the largest contributors to gains while consumer services lagged -1.57%. News of Japan restarting nuclear power fuelled a rally in uranium stocks on Thursday with Paladin Energy up +11.6% along with Deep Yellow +18.3% and Bannerman Energy +15.4% with uranium services provider Silex Systems up +11.8%. Elsewhere, shares in Qantas rose +7.1% after better-than-expected results that delivered a $400 million share buyback. Shares in Nine Entertainment also rose +9% after a bumper $315m profit up 35% on an underlying basis and signalled a buyback of as much as 10% of its shares. The Australian dollar is +1.01% higher overnight at 0.6979 and the 10-year government bond yield rose +4.5 basis points on Thursday to 3.674%.

Oil prices retreated on Thursday with both WTI and Brent crude down -2.18% and -1.56% to US$92.82 and US$99.64 following strong gains earlier in the week. Iron ore futures in Singapore declined -0.57% on Thursday but have reversed those losses trading +0.78% higher this morning at US$103.90 with copper +1.45% higher. Gold rose +0.39% to US$1,757 an oz supported by a weaker USD and lower real yields, silver also gained +0.64% while Bitcoin is -0.35% lower at US$21,616.

Economic data:

- German GfK Consumer Confidence (MoM Sep) 16:00

- U.S. PCE Inflation (YoY Jul) 22:30

- Fed Chair Jerome Powell Speech 00:00

- University of Michigan Consumer Sentiment Final (MoM Aug) 00:00

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.