U.S. equities declined on Tuesday weighed by a decline in consumer confidence as well as weaker earnings from Walmart which reported after the close on Monday.

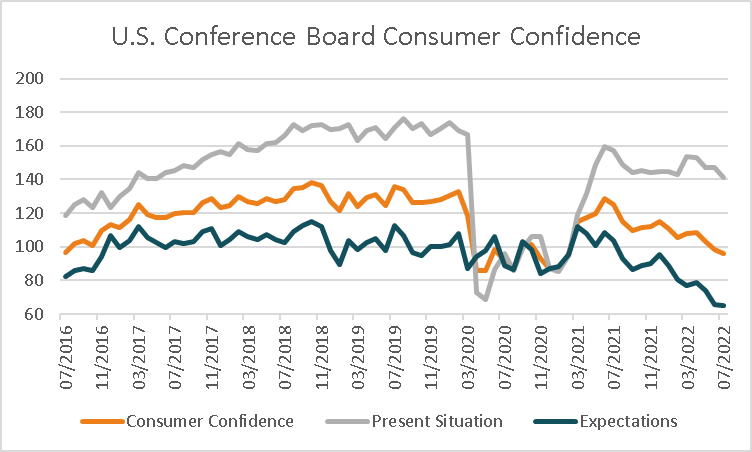

The Conference Board’s measure of consumer confidence declined more than forecast in July to 95.7 from 98.7 previously, missing estimates of 97.2 adding weight to deteriorating economic conditions as the Federal Reserve maintains its aggressive rate increases. The Federal Reserve is also expected to increase rates by an additional +0.75% overnight tonight as it seeks to tame persistently high inflation. Goldman Sachs strategist suggesting the Fed is likely to stay hawkish for longer amid persistently high inflation, echoing views from Morgan Stanley which noted on Monday it is too early to expect the Fed to stop hiking. Meanwhile, JP Morgan strategists noted prices have peaked and will lead to a Fed pivot and improve the picture for equities in the second half of the year.

The S&P500 declined -1.15% weighed by technology -1.58% and consumer discretionary -3.31% while utilities +0.61% and health care +0.55% outperformed. The Dow Jones also retreated -0.71% as did the Nasdaq Composite -1.87% along with the Russell 2000 -0.45% with the VIX rising +5.95% to 35.57. Shares in Google’s parent Alphabet Inc. rose +2.41% in after-hours trading following earnings and revenue which met analyst expectations, reflecting the company’s resilience amid slowing growth in advertising. Meanwhile, shares in Microsoft slipped around -1% in after-hours trading after revenue and profit fell short of analyst expectations amid a stronger USD and weaker corporate demand for cloud services and software as global growth slows.

European equities were lower as investors weighed the strength of corporate earnings amid an ongoing energy crisis. The Euro Stoxx 600 edged -0.03% lower along with the DAX -0.86% and CAC -0.42% while the FTSE100 was unchanged. Adding to news that Gazprom will reduce capacity through the Nord Stream pipeline to 20% of normal capacity from Wednesday, Bloomberg reported the Kremlin is likely to keep vital gas flows to Europe at minimal levels as long as the standoff over Ukraine continues. In response, the European Union has reached an agreement between countries to reduce their gas usage by 15% through next winter as the prospect of a full cut-off from Russian supplies grows increasingly likely. The Euro finished -1% lower at 1.0118 while the Pound edged -0.08% lower to 1.2033 while 10-year government bond yields were lower across the region, ranging from -11.6 basis points in Spain to -2 basis points in the U.K. In focus tonight is the release of German consumer confidence expected to show a modest decline to -28.9 from -27.4 previously.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

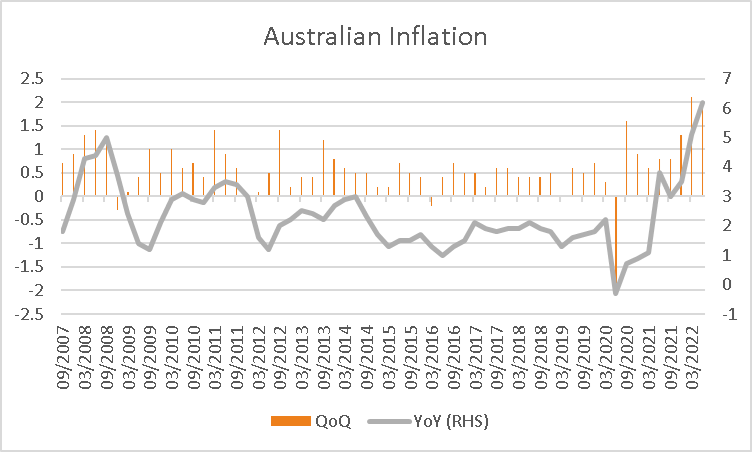

The ASX looks set for a weaker start to trade this morning with ASX200 futures down -39 points or -0.58% to 6,672. The index rose +0.26% on Tuesday boosted by materials +1.61% and energy +2.82% while consumer discretionary stocks lagged -1.71% amid concerns of slowing global growth. Shares in Iress dropped -6.5% after the financial services software company said CEO Andrew Walsh had resigned and will work in a consulting rule until next January. Shares in Zip continued to gain after its recent announcement to exit overseas markets and scrap profits to get back to a profit, rising +19.9% on Tuesday and doubling over the past month. Energy stocks were notable performers amid an ongoing energy crisis in Europe for natural gas which could encourage a switch to coal and crude. WDS gained +2.8% along with STO +2.6% and WHC +6.4%. The Australian dollar is -0.26% weaker overnight at 0.6937 along with the 10-year government bond yield which was -1.4 basis points lower at 3.340% on Tuesday. In focus today is the release of Q2 inflation data expected to show prices moderated to +1.9% from +2.1% in Q1, while rising +6.2% over the 12-month period compared to +5.1% previously.

Oil prices reversed initial gains to finish lower with both WTI and Brent crude down -1.16% and -0.47% respectively at US$95.57 and US$104.67 a barrel. Iron ore futures in Singapore rose +5.61% on Tuesday although are -1.67% lower at US$110.25 this morning while copper futures in the U.S. rose +1.34%. Gold edged -0.15% lower to US$1,717.26 an oz while silver rose +1.05% to US$18.63 and Bitcoin retreated -5.54% to US$20,944.

Economic data:

- Australian Inflation (QoQ Q2) 11:30

- German Consumer Confidence (MoM Aug) 16:00

- U.S. Durable Goods Orders (MoM Jun) 22:30

- Fed Rate Decision 04:00

- Fed Press Conference 04:30

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.