Wall Street finished mixed on Tuesday as U.S. housing data was weaker than expected, and the yield curve flattened on expectations of further rate increases by the Federal Reserve next month.

The Dow Jones finished +0.71% higher boosted by earnings with Walmart rising +5.11% after exceeding profit expectations and improving its full-year forecast, with Home Depot also gaining +4.06% also beating earnings estimates despite a cooling housing market. The S&P500 edged +0.19% higher supported by gains in consumer discretionary +1.09% and consumer staples +1.21% while real estate -0.42% and energy -0.34% lagged. The Nasdaq Composite meanwhile edged -0.19% lower with the Russell 2000 little changed, down -0.04% along with the VIX -1.55% to 19.64.

Data on Tuesday showed the housing market cooled further with housing starts down -9.6% over the month of July compared to forecasts of -2.1% while industrial production was slightly better than expected at +0.6% versus the +0.3% gain estimated. The Federal Reserve is expected to raise interest rates between +0.5% and +0.75% when it meets on September 21st but before then attention turns to the Federal Reserves Jackson Hole Symposium between August 25th and 27th. Historically, the symposium has marked key turning points in monetary policy signalling, and with economic data deteriorating and signs inflation has peaked, markets are certainly leaning towards some type of pivot. The 2-year Treasury yield rose +7.9 basis points to 3.262% on Tuesday along with the 10-year yield by +1.8 basis points while the 30-year rate declined -1.7 basis points to 3.084%.

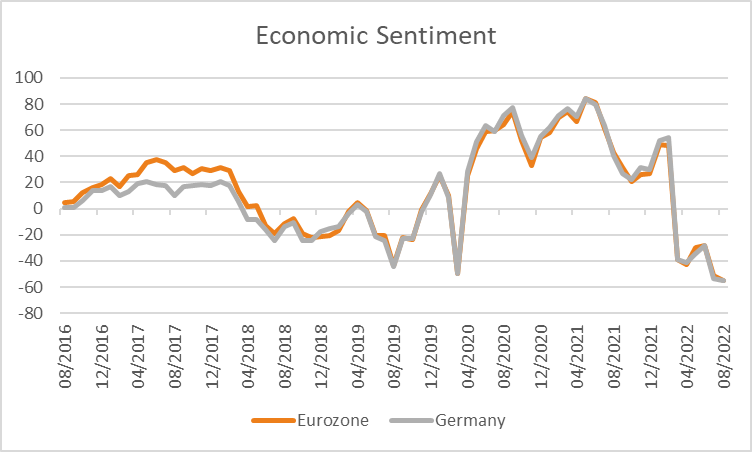

European equities gained for a fifth consecutive session, the longest winning streak since March with the Euro Stoxx 600 up +0.16% along with the DAX +0.68%, CAC +0.34%, and FTSE100 +0.36%. Data on Tuesday showed that Eurozone economic sentiment for August declined less than expected to -54.9 compared to -57 expected although weaker than the reading of -51.1 in July. German economic sentiment also declined to -55.3 against expectations to remain unchanged at -53.8. U.K. employment for the 3 months to June showed +160k jobs were added, lower than the +268k expected with the unemployment rate remaining stable at 3.8%. Economists are growing increasingly pessimistic about the UK, with the risk of a recession now seen as far more likely than not and interest rates expected to go higher than previously thought. Further inflation data for the U.K. will be released tonight expected to show core prices edged higher over the year to +5.9% from +5.8% previously with headline prices expected to rise to +9.8% from +9.4%.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX is expected to edge higher this morning with ASX200 futures up +8 points or +0.11% to 7,016. The index gained +0.58% on Tuesday boosted by materials +1.67% and financials +0.36% with miner BHP climbing +4.1% after posting underlying profit of US$21.3 billion versus US$20.9 billion estimated. BHP also declared an increased dividend of US$1.75 up from US$1.50 in February. Temple & Webster shares were a notable performer, surging +29.8% after saying margins will improve to 3-5% from 2-4% previously. Meanwhile, shares in investment manager Challenger slumped -10.1% after posting a near 60% decline in statutory profit as the manager took a hit from turbulent financial markets. The Australian dollar is little changed at 0.7205 overnight while the 10-year government bond yield declined -14 basis points on Tuesday to 3.224% after the minutes of the latest RBA meeting warned household spending presents “a key source of uncertainty for the outlook” with wage price data for Q2 out at 11:30 AEDT today.

Oil prices declined on expectations Iranian nuclear talks will bring supply back to the market with both WTI and Brent crude -2.9% and -2.81% lower at US$86.84 and US$92.46 a barrel. Iron ore futures in Singapore were -0.33% weaker on Tuesday although are trading +0.82% higher at US$106.50 this morning with copper prices also +0.18% higher. Gold declined -0.24% to US$1,775.43 an oz along with silver -0.71% to US$20.13 and Bitcoin -0.57% to US$23,936.

Economic data:

- Australian Westpac Leading Index (MoM Jul) 10:30

- Australian Wage Price Index (YoY Q2) 11:30

- RBNZ Rate Decision 12:00

- U.K. Inflation (YoY Jul) 16:00

- Eurozone GDP 2nd Estimate (QoQ Q2) 19:00

- U.S. Retail Sales (MoM Jul) 22:30

- Fed Bowman Speech 23:30

- FOMC Minutes 04:00

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.