U.S. equities rose on Wednesday with the latest corporate news lifting stocks offsetting concerns of geopolitical risks in Europe.

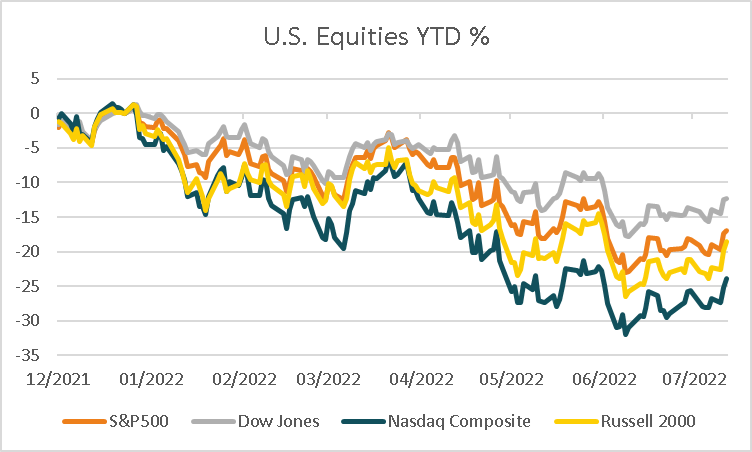

The S&P500 rose +0.59%, lifted by technology +1.56% and consumer discretionary +1.77% with utilities led declines down -1.36%. The Dow Jones also rose +0.15% along with the Nasdaq Composite +1.58% and Russell 2000 +1.59% with the VIX finishing -2.53% lower at 23.88. Shares in Netflix rose +7.7% after it reported better-than-feared earnings as well as losing less than expected customers in the first half of 2022 which declined more than 1m with Chairman Reed Hastings noting “We’re talking about losing 1 million instead of 2 million — our excitement is tempered by the less-bad results”. Meanwhile, Tesla shares surged as much as +4.4% in after-hours trading before paring gains back to +1.8% after second-quarter profit exceeded analyst expectations, reporting production was getting back on track while tackling supply chain disruptions and lockdowns at its factory in China. The electric vehicle maker posted adjusted earnings of $2.27 per share compared to the average forecast of $1.83.

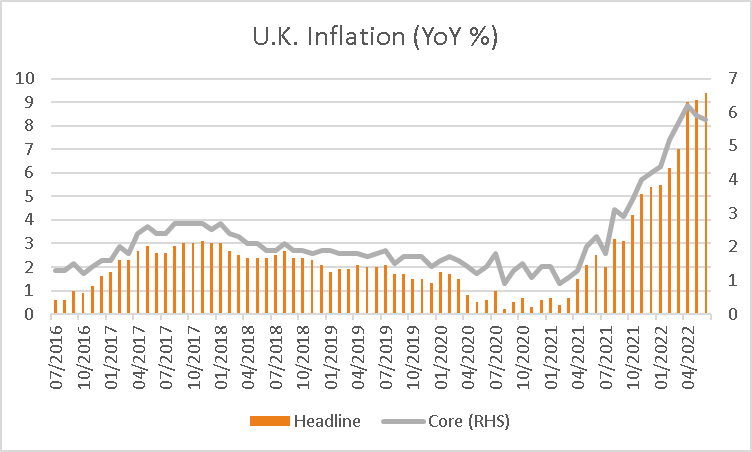

European equities reversed initial gains to finish lower, weighed by the latest political developments in Italy. Italian President Mario Draghi appeared to fall after three key parties failed to support him in a confidence vote. Draghi’s resignation would most likely result in snap elections in the coming months, adding political turmoil as economic warning signs flash. The Euro Stoxx 600 declined -0.21% along with the DAX -0.20%, CAC -0.27% and FTSE100 -0.44% with the Euro weakening -0.47% to 1.0179. U.K. consumer prices hit the highest levels since 1982 in June, rising at an annual rate of +9.4% compared to estimates of +9.3% while core inflation rose +5.8% in line with forecasts. According to Hussain Mehdi of HSBC Asset Management, “The intense cost of living squeeze is putting significant pressure on the UK’s consumer-led economy and means the risk of recession is high”. Also weighing on sentiment are fears that Russia may not restart gas supplies to the continent which are due to be resumed today although Russian President Vladimir Putin earlier signaled gas supplies would resume, although flows would be tightly curbed unless a spat over sanctioned parts is resolved. The ECB will be in focus when it meets to discuss monetary policy tonight with markets expecting a +0.50% increase as well as an unveiling of a new bond-purchase program to ensure rate increases won’t see yield spreads widen in more indebted members. Elsewhere, Eurozone flash consumer confidence for July declined more than expected to -27 vs -24.9 from a slightly revised lower -23.8 in June.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX looks set to open lower this morning with ASX200 futures down -30 points or -0.45% to 6,639. The index rose +1.65% on Wednesday boosted by strong gains in the U.S. with all sectors positive led by technology +3.76% and materials +2.51% with 90% of stocks rising. Shares in Megaport pared gains of over +30% to finish +23% higher after an earnings update with the company saying it swung to an operating cash profit in the June quarter as sales jumped +10% to $30.6 million. Beach Energy posted its best quarterly earnings in more than three years with revenue rising +10% to $504m over the three months from $458m previously while production totaled 5.6m barrels up from 5.2m the prior quarter with shares rising +2.82%. In economic data, the Westpac Leading Index for June declined -0.2 over the month from -0.1 previously while a speech by RBA Governor Philip Lowe added to expectations the central bank will continue to aggressively raise interest rates.

Oil prices edged lower despite U.S. crude inventories declining for the week ending July 15th by -446k barrels compared to estimates of a +1.857m barrel increase as gasoline inventories climbed more than forecast to 3.498m vs 71k expected. Both WTI and Brent crude were -0.99% and -0.66% lower at US$99.74 and US$106.64 a barrel. Iron ore futures in Singapore rose +2.88% on Wednesday although are -0.68% weaker this morning at US$99.50 while copper futures in the U.S. rose +0.56%. Gold declined -0.88% to US$1,696 weighed by a slightly stronger USD +0.34% and higher real yields, with silver also -0.44% lower at US$18.68 and Bitcoin was little changed at US$23,258.

Economic data:

- Bank of Japan Rate Decision 13:00

- ECB Rate Decision 22:15

- U.S. Initial Jobless Claims (July 16th) 22:30

- ECB Press Conference 22:45

- U.S. Conference Board Leading Index 00:00

- ECB President Lagarde Speech 00:15

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.