U.S. equities finished the week mixed on Friday while Treasury yields climbed after a stronger than expected jobs report for July is set to keep the Federal Reserve on a tightening path.

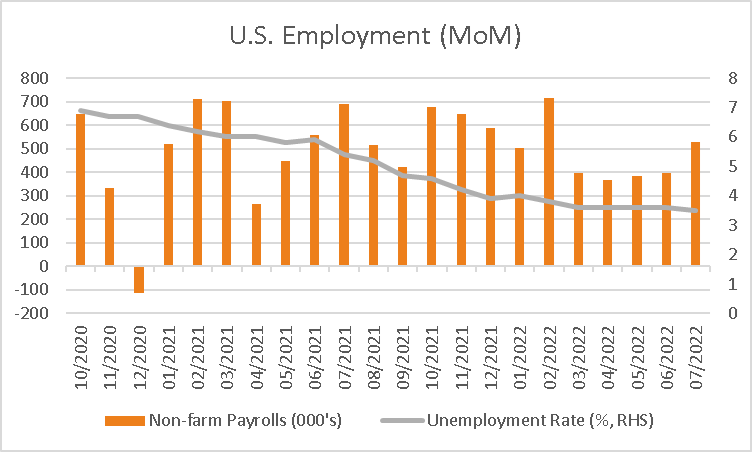

528k jobs were added in July, surpassing the average analyst’s estimate of 250k with the June figure also revised higher by 26k. The unemployment rate also edged lower to 3.5% from 3.6% previously while average hourly earnings rose 5.2% over the 12 months compared to estimates of 4.9%. The data is likely to validate the Federal Reserve’s view that the economy remains resilient and can stand additional rate increases, ruling out the possibility of a dovish pivot for now despite deteriorating economic data. Traders quickly recalibrated their expectations for a 0.5% rate hike at the September meeting to 0.75% based on futures pricing while Treasury yields climbed across the curve with the 2-year rate up +18.2 basis points along with the 10 and 30-year rates by +14 and +10.3 basis points.

The S&P500 finished -0.16% lower weighed by consumer discretionary -1.66% and communications -0.88% while energy outperformed +2.04% on higher oil prices following recent selling. The Nasdaq Composite was also -0.50% lower while the Russell 2000 rose +0.81% along with the Dow Jones +0.23% and the VIX edged -1.35% lower to 21.15. Ahead for the week, investors will be focused on inflation data for July released on Wednesday with core inflation forecast to rise 6.1% from 5.9% previously and headline inflation to moderate to 8.7% from 9.1% over the 12-month period. Thursday will bring producer price data expected to moderate over the month to 0.3% from 1.1 in June and the week will be rounded off with the University of Michigan consumer sentiment survey for August expected to modestly improve to 52.2 from 51.5.

European equities finished lower on Friday, weighed by the prospect of further rate increases as well as ongoing geopolitical tensions between China and Taiwan with China continuing military drills and cutting off defense talks with the U.S. The Euro Stoxx 600 finished -0.76% lower along with the DAX -0.65%, CAC -0.63%, and FTSE100 -0.11%. European equities have rebounded almost 10% over the past month despite hawkish central banks with JP Morgan strategists noting, “Earnings have been surprisingly resilient, with 62% of the Stoxx 600 firms that have reported results so far beating estimates, while revenue growth is at 36%, surprising positively”. Ahead for the week, investors will focus on the final reading of German inflation data for July on Wednesday, followed by U.K. GDP for the 3 months to June forecast to show a -0.2% contraction.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

The ASX is set to open modestly lower this morning with ASX200 futures down -7 points or -0.10% to 6,907. The index was 0.58% higher on Friday lifted by materials +1.88% and health care +1.04% while energy -1.44% and technology -1.25% underperformed. Earnings are in focus for the week ahead with Aurizon and Suncorp due to report results on Monday followed by Charter Hall Long WALE, Computershare, Cornado Mining, Megaport, National Australia Bank, News Corp, and REA Group on Tuesday. Economic data is light this week, with the release of the Westpac consumer confidence index for August on Tuesday and consumer inflation expectations on Thursday the only notable data points. The Australian dollar traded -0.86% lower on Friday to 0.6911 while the 10-year government bond yield declined -5.8 basis points to 3.086% although we should expect higher yields to start the week given the sharp move higher in the U.S.

Oil prices finished higher on Friday with both WTI and Brent crude up 0.53% and 0.85% respectively to US$89.01 and US$94.92 a barrel. Base metals finished the week mixed with aluminum down -2.91% along with copper -0.59%, nickel -5.94%, and Tin -2.36% while Zinc and lead rose 5.44% and 1.74% respectively. Iron ore futures in Singapore were 3.22% higher on Friday and a further 2.65% higher this morning at US$112. Gold retreated -0.88% to US$1,775 weighed by a stronger USD and higher yields, silver was also -1.40% weaker at US$19.90 while Bitcoin rose 2.1% and is a further 1.1% higher over the weekend at US$23,245.

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.