U.S. equities rebounded on Wednesday with Treasury yields falling as investors assessed comments from members of the Federal Reserve.

The S&P500 climbed +1.83% boosted by gains in technology +1.59% and consumer discretionary +3.8% while energy was the only negative sector down -1.15% as oil prices slumped. The Dow Jones also rose +1.40% along with the Nasdaq Composite +2.14% and Russell 2000 +2.21% with the VIX retreating -8.44% to 24.64. Shares in Apple Inc. rose +0.93% after unveiling the latest instalment of its flagship product the iPhone 14 banking on camera upgrades and new emergency satellite messaging which will start at US$799 while the iPhone Plus will start at US$899 with pre-ordering from September 9th.

In a press release on bringing down inflation, Fed Vice Chair Lael Brainard said “At some point in the tightening cycle, the risks will become more two-sided. The rapidity of the tightening cycle and its global nature…create risks associated with overtightening” suggesting that the Fed may soon ease the pace of rate increases if economic data softens. Still, Brainard noted the Fed will need to raise rates to restrictive levels and keep them there for “some time”. Separately Loretta Mester warned against declaring early victory on inflation while Susan Collins of the Boston Fed said it’s too soon to specify what policymakers should do at the September 20-21st meeting. The 2-year yield weakened -7 basis points to 3.433% along with both the 10 and 30-year rates by -8.4 and -8.3 basis points respectively with the U.S. dollar index weakening -0.58%.

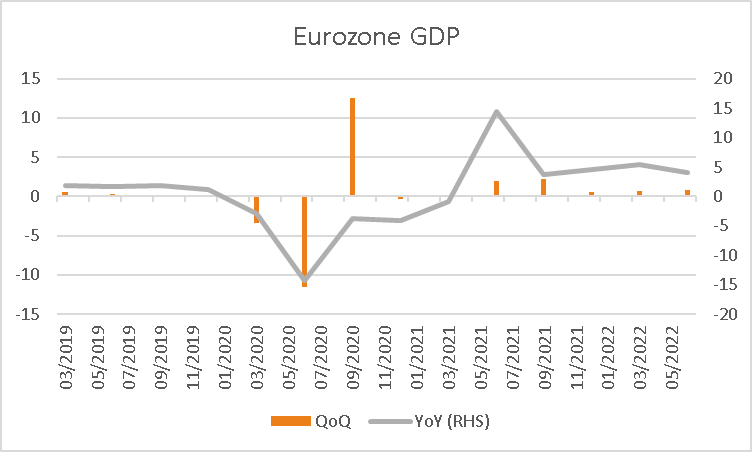

European equities were mixed amid hawkish policy and gas rationing concerns with an emergency meeting scheduled for Friday morning AEDT. The Euro Stoxx 600 finished -0.57% lower along with the FTSE100 while the CAC edged +0.02% higher and the DAX rose +0.35%. In focus is tonight’s ECB policy meeting where traders are forecasting a +0.50% increase as the central bank seeks to tame decades-high inflation. In economic data, the final reading of Q2 GDP for the Eurozone was better-than-expected rising +0.8% vs +0.6% forecast over the quarter and +4.1% vs +3.9% over the 12 months. 10-year government bond yields were lower across the region ranging from -11.4 basis points in the U.K. to -4.9 basis points in Switzerland with the Euro rising +1.06% to 1.0009 and the Pound up +0.14% to 1.1536.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

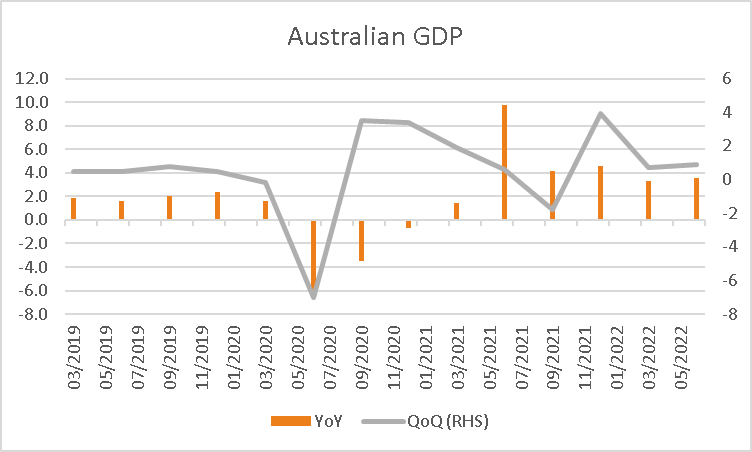

The ASX looks set to open higher this morning with ASX200 futures up +34 points or +0.51% to 6,757. The index slumped -1.42% on Wednesday following a weak lead from Wall Street weighed by declines in financials -2.0% and materials -2.07% while technology +0.33% and health care +0.17% were the only sectors positive. In economic data, GDP for Q2 rose +0.9% over the quarter, modestly below estimates of a +1.0% increase while rising +3.6% over the 12 months, modestly above the +3.5% forecast. However, economists were quick to note the data did not capture the effects of the RBA’s +2.25% worth of rate increases since May, tipping growth to decelerate with VanEck’s Russel Chesler noting “The domestic economy remains vulnerable to global influences such as rising energy and food prices and a slowdown in the world’s largest economy, the US. Chinese growth too is slowing with ongoing shutdowns”.

Oil prices slumped overnight tumbling to the lowest levels in more than six months as demand concerns from China prompted a wave of selling. Both WTI and Brent crude declined -5.90% and -5.62% respectively to US$81.76 and US$87.62 a barrel. Iron ore futures in Singapore were -0.58% lower on Wednesday although are trading +0.30% higher at US$96.75 this morning with copper -0.66% lower. Gold rose +0.97% to US$1,718 boosted by a weaker USD and decline in real yields, silver also rose +2.48% to US$18.46 with Bitcoin also +2.09% higher at US$19,375.

Economic data:

- RBA Governor Lowe Speech 13:05

- ECB Rate Decision 22:15

- Fed Chair Powell Speech 23:10

- ECB Lagarde Speech 00:15

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via info@rivkin.com.au or by phoning +612 8302 3632.